Best Credit Cards for Expats in Singapore 2024

Compared to residents, foreigners typically need a higher annual salary in order to qualify for a credit card. Keeping in mind both income requirements and common needs of expats at every socioeconomic status, our research experts reveiwed 100+ of the most competitive credit cards on the market to identify which best fit expatriates' and foreigners' lifestyles.

- UOB PRVI Miles Amex: Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- Citi Prestige: Unlimited lounge access, bonus hotel nights & more

- SC Visa Infinite X: Bonus S$6,000 w/ S$200k fund placement

- Citi Cash Back+: Unlimited 1.6% cashback on all spend

- SC Unlimited Cashback: 1.5% unlimited rebate + transport perks

- Amex True Cash Back: Unlimited 1.5% rebate + Amex benefits

- Maybank FC Barcelona: Highest unlimited local rebate–1.6% on all spend

- HSBC Advance: Up to 3.5% cashback capped at S$300/month

- Citi PremierMiles Visa: 45,000 Welcome Citi Miles with S$9,000 spend in 3 mo

- KrisFlyer UOB: 3mi/S$1 on dining, transport, shopping & travel

- HSBC Revolution: 4 miles per S$1 spent online and on contactless payments

- UOB One: Highest flat rebate on the market, earn up to $300/qtr

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- Citi Cash Back: Up to 8% rebate on groceries & petrol, 6% on dining

- HSBC Visa Platinum: 5% rebate on groceries, dining & petrol, miles for general

- Maybank World: Free green fees at 100 fairways across 19 countries

- Amex Platinum: Elite dining & lifestyle perks in SG

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- POSB Everyday: Rebates up to 10% in Singapore

- Citi Rewards: Up to 4 miles per S$1 for fashion & online spend

- OCBC Titanium: 4 miles per S$1 on fashion & select retail

- SC SingPost Spree: 3% rebate online overseas & vPost transactions

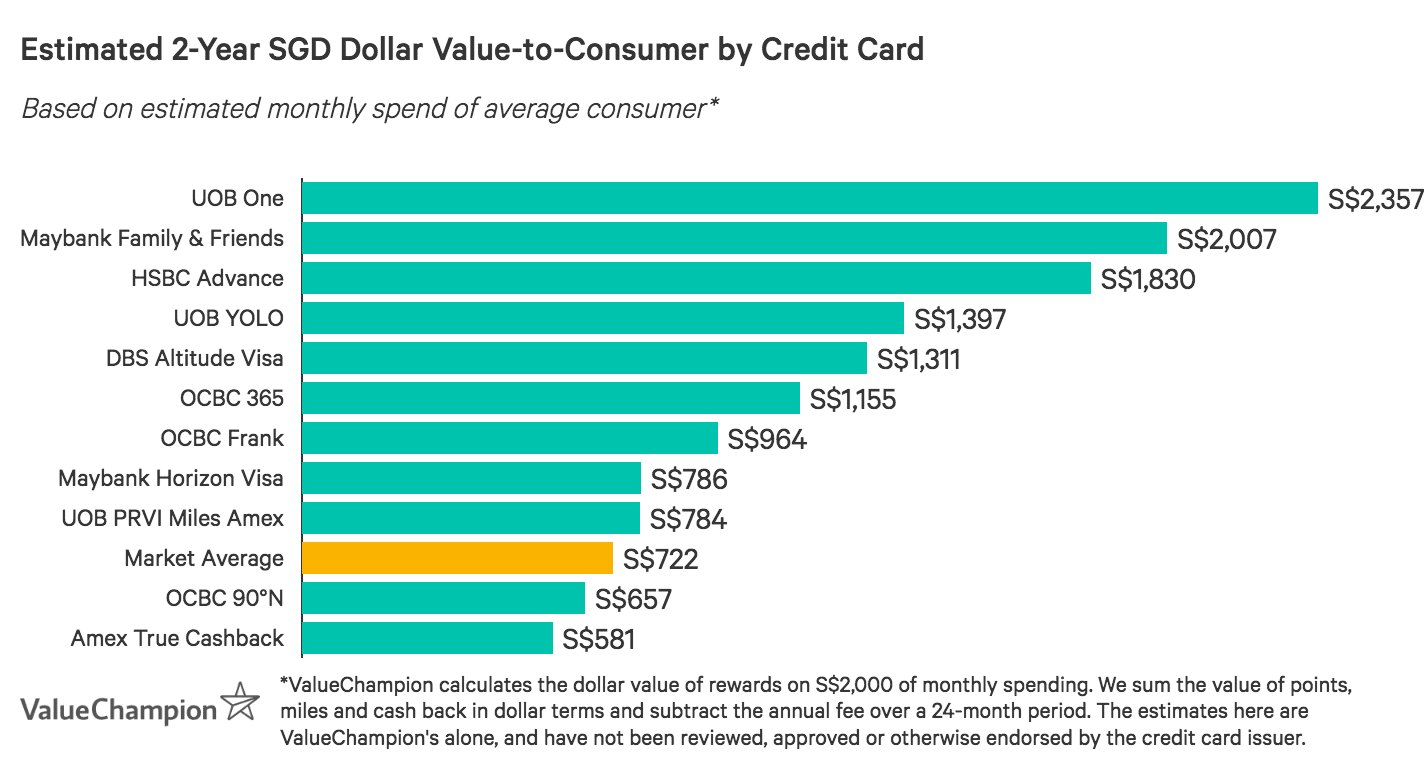

Compare the Best Credit Cards for Expats in Singapore by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Compare Best Expat Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Best Miles Credit Cards for Expats

If you travel often, whether personally or for business, you may want to earn miles rewards for your spend. The following offer both great rates and top-notch perks.

UOB PRVI Miles American Express Card: Rapid Miles Accumulation

| |

UOB PRVI Miles American Express Card is an excellent choice for expats who want to rapidly accumulate miles without paying an annual fee. Cardholders earn at some of the highest rates on the market: 1.4 miles per S$1 locally, 2.4 miles overseas, and 6 miles with major airlines & hotels. Perks include up to 8 free airport transfers a year and free travel insurance. Credit cards with similar perks and rates have annual fees of S$400+.

| |

|

|

UOB PRVI Miles American Express Card is an excellent choice for expats who want to rapidly accumulate miles without paying an annual fee. Cardholders earn at some of the highest rates on the market: 1.4 miles per S$1 locally, 2.4 miles overseas, and 6 miles with major airlines & hotels. Perks include up to 8 free airport transfers a year and free travel insurance. Credit cards with similar perks and rates have annual fees of S$400+.

|

Citi Prestige MasterCard: Best Luxury Travel Perks

|

|

Citi Prestige MasterCard stands out for its incredible luxury travel perks, making it the absolute best option for expats who prioritise comfort and convenience in their travels. Cardholders earn top rewards rates of 1.3 miles per S$1 locally and 2.4 miles overseas, receive 25,000 annual bonus miles (worth S$250), and can earn an annual bonus up to 30% based on the tenure of their relationship with Citibank. These features offset much of the admittedly high S$535.0 fee.

| |

|

|

|---|

|

|

Citi Prestige MasterCard stands out for its incredible luxury travel perks, making it the absolute best option for expats who prioritise comfort and convenience in their travels. Cardholders earn top rewards rates of 1.3 miles per S$1 locally and 2.4 miles overseas, receive 25,000 annual bonus miles (worth S$250), and can earn an annual bonus up to 30% based on the tenure of their relationship with Citibank. These features offset much of the admittedly high S$535.0 fee.

|

Standard Chartered Visa Infinite X: Upfront Miles for Affluent Travellers

| |

Wealthy expats with readily accessible funds should definitely consider Standard Chartered Visa Infinite X Card. Cardholders who place S$300k fresh funds into a SC Priority Banking account within the 1st 3 months receive an incredible 100,000 bonus KrisFlyer miles. Bonuses increase with larger placements. In fact, placing S$800k funds earns 150,000 bonus miles (worth approximately S$15k when redeemed for business class tickets) and Priority Private Banking customers who place S$1.5m receive 300,000 miles (worth S$30k). This bonus is ideal for very affluent expats, especially those who want to quickly accrue miles and don't mind opening an account with Standard Chartered.

| |

|

|

Wealthy expats with readily accessible funds should definitely consider Standard Chartered Visa Infinite X Card. Cardholders who place S$300k fresh funds into a SC Priority Banking account within the 1st 3 months receive an incredible 100,000 bonus KrisFlyer miles. Bonuses increase with larger placements. In fact, placing S$800k funds earns 150,000 bonus miles (worth approximately S$15k when redeemed for business class tickets) and Priority Private Banking customers who place S$1.5m receive 300,000 miles (worth S$30k). This bonus is ideal for very affluent expats, especially those who want to quickly accrue miles and don't mind opening an account with Standard Chartered.

|

OCBC Voyage: Flexible Miles Redemption

|

|

If you’re an expat with a shifting travel schedule, you can benefit from OCBC Voyage Card’s flexibility in rates and miles redemption. Cardholders earn 1.3 miles per S$1 locally and 1.3 miles per S$1 spend overseas. In addition, overseas spend earns a competitive 2.2 miles per S$1 (when charged in foreign currency) so you can earn high rates wherever you are.

| |

|

| |

|---|---|

| |

| |

If you’re an expat with a shifting travel schedule, you can benefit from OCBC Voyage Card’s flexibility in rates and miles redemption. Cardholders earn 1.3 miles per S$1 locally and 1.3 miles per S$1 spend overseas. In addition, overseas spend earns a competitive 2.2 miles per S$1 (when charged in foreign currency) so you can earn high rates wherever you are.

| |

Standard Chartered Visa Infinite: Best Miles for Business Travellers

| |

Standard Chartered Visa Infinite Card is a great card for business travellers and expats with high spend overseas. In fact, SC Visa Infinite Card has the highest overseas rewards rate on the market–an incredible 3 miles per S$1 spend. Cardholders also earn a highly competitive 1.4 miles per S$1 locally, and receive 35,000 welcome miles with card approval (worth S$350).

Finally, this credit card offers excellent travel perks. Cardholders enjoy 6 free lounge visits/year, a free 4hr yacht hire, Hertz Asia rental privileges, golfing privileges throughout SE Asia and much more. While there’s a S$588.5 fee, this is easily reflected in value by its market-leading rewards rate and exemplary perks. Overall, if you’re a high-earning expat that frequently travels for business, SC Visa Infinite Card is a great choice for you. | |

|

|

Standard Chartered Visa Infinite Card is a great card for business travellers and expats with high spend overseas. In fact, SC Visa Infinite Card has the highest overseas rewards rate on the market–an incredible 3 miles per S$1 spend. Cardholders also earn a highly competitive 1.4 miles per S$1 locally, and receive 35,000 welcome miles with card approval (worth S$350).

Finally, this credit card offers excellent travel perks. Cardholders enjoy 6 free lounge visits/year, a free 4hr yacht hire, Hertz Asia rental privileges, golfing privileges throughout SE Asia and much more. While there’s a S$588.5 fee, this is easily reflected in value by its market-leading rewards rate and exemplary perks. Overall, if you’re a high-earning expat that frequently travels for business, SC Visa Infinite Card is a great choice for you. |

Best Cashback Credit Cards for Expats

Singapore’s cost-of-living is quite high. The following cards offer great options for maximising cashback on all of your spend.

American Express True Cashback Card: Limitless Rebates + Amex Perks

|

|

American Express True Cashback Card is the best unlimited credit card on the market if you’re an Amex loyalist–especially if you’re an expat who’s used to using an American Express credit card. Cardholders earn an unlimited 1.5% cashback on all spend, doubled to 3% for the first 6 months (up to S$150). Few competitors offer such a broad and lucrative welcome deal.

| |

|

|

|---|

|

|

American Express True Cashback Card is the best unlimited credit card on the market if you’re an Amex loyalist–especially if you’re an expat who’s used to using an American Express credit card. Cardholders earn an unlimited 1.5% cashback on all spend, doubled to 3% for the first 6 months (up to S$150). Few competitors offer such a broad and lucrative welcome deal.

|

Maybank FC Barcelona Visa Signature: Unlimited Local Cashback

| |

If you have a big budget but mostly spend locally, Maybank FC Barcelona Visa Signature Card is the best credit card to maximise your cashback. Cardholders earn an unlimited 1.6% cashback on all local spend, which is higher than any competitors’ (1%–1.5%). Cardholders also earn 0.8 miles per S$1 spend overseas (equal to about 0.8% rebate), but this is less competitive, so Maybank FC Barcelona is best as a local credit card.

Finally, this is a great credit card if you’re an expat that loves sports–specifically, football (or “soccer”) & the FC Barcelona team. Cardholders receive discounts up to 10% at official FC Barcelona stores and can win a free trip (including full travel package) to see FC Barcelona playing live. Overall, Maybank FC Barcelona Card offers local high spenders a great way to earn unlimited rewards, with the added perk of expat-friendly sports discounts. | |

|

|

If you have a big budget but mostly spend locally, Maybank FC Barcelona Visa Signature Card is the best credit card to maximise your cashback. Cardholders earn an unlimited 1.6% cashback on all local spend, which is higher than any competitors’ (1%–1.5%). Cardholders also earn 0.8 miles per S$1 spend overseas (equal to about 0.8% rebate), but this is less competitive, so Maybank FC Barcelona is best as a local credit card.

Finally, this is a great credit card if you’re an expat that loves sports–specifically, football (or “soccer”) & the FC Barcelona team. Cardholders receive discounts up to 10% at official FC Barcelona stores and can win a free trip (including full travel package) to see FC Barcelona playing live. Overall, Maybank FC Barcelona Card offers local high spenders a great way to earn unlimited rewards, with the added perk of expat-friendly sports discounts. |

Citi Cash Back+ Card: Highest Flat Uncapped Rebate

| |

If you regularly spend more than S$6,000/month, you should definitely consider applying for Citi Cash Back+ Card to maxmise the rebate you can earn. This card provides a flat rate rebate of 1.6% on all of your spending, both local and overseas, without any minimum spend requirement or cap on limit. This feature is custom-made for affluent consumers who can easily feel constrained by cards that limit how much cash back they can earn. While it doesn't provide many extra perks or privileges, Citi Cash Back+ Card's rewards rate is higher than the 1.5% offered by most comparable credit cards. As a result, Citi Cash Back+ is the best option for people with large budgets who are focused primarily on earning to their full potential.

| |

|

|

If you regularly spend more than S$6,000/month, you should definitely consider applying for Citi Cash Back+ Card to maxmise the rebate you can earn. This card provides a flat rate rebate of 1.6% on all of your spending, both local and overseas, without any minimum spend requirement or cap on limit. This feature is custom-made for affluent consumers who can easily feel constrained by cards that limit how much cash back they can earn. While it doesn't provide many extra perks or privileges, Citi Cash Back+ Card's rewards rate is higher than the 1.5% offered by most comparable credit cards. As a result, Citi Cash Back+ is the best option for people with large budgets who are focused primarily on earning to their full potential.

|

Standard Chartered Unlimited Cashback: Unltd. Rebates + Transport Perks

| |

Standard Chartered Unlimited Cashback Card is one of the absolute best options for high-spenders on the market. If you’re spending S$7,000/month or more–which is quite possible, given the comparatively high prices in Singapore–most cashback cards will restrict your earning potential by imposing rewards caps. SC Unlimited Cashback Card, however, offers an unlimited 1.5% cashback on all spend, so you don’t need to worry about restrictions.

Finally, while there’s a S$60,000 annual income requirement for foreigners, this is fairly reasonable for higher spenders, who are most likely to benefit from this credit card. Ultimately, SC Unlimited Cashback Card is an exceptional option if you want to consolidate your spend onto one card, maximise earnings with no restriction, and enjoy perks that make getting around both convenient & affordable. | |

|

|

Standard Chartered Unlimited Cashback Card is one of the absolute best options for high-spenders on the market. If you’re spending S$7,000/month or more–which is quite possible, given the comparatively high prices in Singapore–most cashback cards will restrict your earning potential by imposing rewards caps. SC Unlimited Cashback Card, however, offers an unlimited 1.5% cashback on all spend, so you don’t need to worry about restrictions.

Finally, while there’s a S$60,000 annual income requirement for foreigners, this is fairly reasonable for higher spenders, who are most likely to benefit from this credit card. Ultimately, SC Unlimited Cashback Card is an exceptional option if you want to consolidate your spend onto one card, maximise earnings with no restriction, and enjoy perks that make getting around both convenient & affordable. |

HSBC Advance Card: Rebates for Affluent Advance Customers

| |

HSBC Advance Card is an extraordinary option for high-spenders willing to consider an Advance banking account–which itself has features tailored specifically to expats. Cardholding Advance customers earn 3.5% flat rebate up to S$125/month, after S$2,000 spend (2.5% if below). Rewards can be maxed out with S$3,500/month spend, allowing you to earn up to S$1,500/year–the highest earning potential for a capped card on the market.

Another reason to consider both HSBC Advance Card and an Advance banking account is that customers have access to special expatriate banking privileges. These include the ability to manage up to 11 currencies in a single account, set a target foreign exchange rate for auto-conversion, link and make instant transfers between HSBC accounts worldwide & more. Finally, HSBC Advance Card has one of the lowest income requirements for expats at just S$40,000. If you’re an above-average spender looking to maximise cashback and enjoy expat banking perks, definitely consider HSBC Advance Card with an Advance account. | |

|

|

HSBC Advance Card is an extraordinary option for high-spenders willing to consider an Advance banking account–which itself has features tailored specifically to expats. Cardholding Advance customers earn 3.5% flat rebate up to S$125/month, after S$2,000 spend (2.5% if below). Rewards can be maxed out with S$3,500/month spend, allowing you to earn up to S$1,500/year–the highest earning potential for a capped card on the market.

Another reason to consider both HSBC Advance Card and an Advance banking account is that customers have access to special expatriate banking privileges. These include the ability to manage up to 11 currencies in a single account, set a target foreign exchange rate for auto-conversion, link and make instant transfers between HSBC accounts worldwide & more. Finally, HSBC Advance Card has one of the lowest income requirements for expats at just S$40,000. If you’re an above-average spender looking to maximise cashback and enjoy expat banking perks, definitely consider HSBC Advance Card with an Advance account. |

Best Credit Cards for Expat Low Spenders

If you’re an expat in Singapore with a lower salary or lower income, these cards offer great ways to earn meaningful cashback without high fees or minimums.

Citi PremierMiles Visa: Affordable Perks & Bonus Miles

| |

Citi PremierMiles Visa Card is the best travel credit card for earning high rewards and enjoying great perks without having to pay a massive annual fee. Cardholders earn 1.2 miles per S$1 locally and 2 miles overseas, which aligns with market standards. However, cardholders also receive up to 45,000 welcome miles (worth S$450), plus 10,000 annual bonus miles (worth S$100)–a feature usually associated only with the priciest travel cards.

| |

|

|

Citi PremierMiles Visa Card is the best travel credit card for earning high rewards and enjoying great perks without having to pay a massive annual fee. Cardholders earn 1.2 miles per S$1 locally and 2 miles overseas, which aligns with market standards. However, cardholders also receive up to 45,000 welcome miles (worth S$450), plus 10,000 annual bonus miles (worth S$100)–a feature usually associated only with the priciest travel cards.

|

KrisFlyer UOB Credit Card: Boosted Miles for SIA Loyalists

| |

If you're a budget-minded expat willing to fly primarily with Singapore Airlines, you may be able to maximise your miles rewards with KrisFlyer UOB Card. Cardholders earn 1.2 miles per S$1 local and overseas spend, elevated to 3 miles for transactions with SIA, Scoot, SilkAir and KrisShop. Consumers can unlock a boosted 3 miles per S$1 rate for global dining & online food delivery, transport, online fashion & travel booking with just S$500 min. spend with SIA brands within a year. This minimum is quite reasonable and can typically be achieved with just 2-3 regional trips per year.

| |

|

|

If you're a budget-minded expat willing to fly primarily with Singapore Airlines, you may be able to maximise your miles rewards with KrisFlyer UOB Card. Cardholders earn 1.2 miles per S$1 local and overseas spend, elevated to 3 miles for transactions with SIA, Scoot, SilkAir and KrisShop. Consumers can unlock a boosted 3 miles per S$1 rate for global dining & online food delivery, transport, online fashion & travel booking with just S$500 min. spend with SIA brands within a year. This minimum is quite reasonable and can typically be achieved with just 2-3 regional trips per year.

|

HSBC Revolution: No-Fee Miles for Online & Social Spend

| |

If you find yourself spending a sizeable portion of your budget on local food & entertainment and like to shop online, HSBC Revolution Card is the best miles-earning option on the market. You’ll earn 2 miles per S$1 local spend on dining & entertainment (restaurants, cafes, fast food, clubs, pubs, bars & more), as well as for online transactions–including transit and bill payments. If you’re new to Singaporean credit cards, it’s worth pointing out–most exclude such payments from earning rewards at all.

| |

|

|

If you find yourself spending a sizeable portion of your budget on local food & entertainment and like to shop online, HSBC Revolution Card is the best miles-earning option on the market. You’ll earn 2 miles per S$1 local spend on dining & entertainment (restaurants, cafes, fast food, clubs, pubs, bars & more), as well as for online transactions–including transit and bill payments. If you’re new to Singaporean credit cards, it’s worth pointing out–most exclude such payments from earning rewards at all.

|

UOB One Credit Card: Best Rebates for Consistent Spenders

| |

If you spend at least S$2,000 every month, you can easily maximise your cashback with UOB One Card. At this spend level, cardholders earn 5% flat rebate on all spend, up to S$300/quarter. This rate is boosted to 10% cashback for Grab & select UOB Travel spend and 6% for utilities bills. Lower or inconsistent spend earns at 3.33%, up to S$50 or S$100/quarter (depending on minimum spend level).

If you do feel comfortable spending with select merchants, you can effectively ‘double’ your rebates through UOB SMART$ Programme. Transactions with merchants like BreadTalk, Cold Storage, Cathay Cineplexes & more earn SMART$ (worth S$1 each), which can be used to offset future purchases. This spend also counts towards hitting your minimum, working towards earning the highest rebate rate. Finally, UOB One Card has one of the lowest income requirements for foreigners on the market, at just S$40,000. Overall, if you’re likely to spend S$2,000/month on a consistent basis, UOB One Card offers one of the easiest ways to maximise cashback on every transaction. | |

|

|

If you spend at least S$2,000 every month, you can easily maximise your cashback with UOB One Card. At this spend level, cardholders earn 5% flat rebate on all spend, up to S$300/quarter. This rate is boosted to 10% cashback for Grab & select UOB Travel spend and 6% for utilities bills. Lower or inconsistent spend earns at 3.33%, up to S$50 or S$100/quarter (depending on minimum spend level).

If you do feel comfortable spending with select merchants, you can effectively ‘double’ your rebates through UOB SMART$ Programme. Transactions with merchants like BreadTalk, Cold Storage, Cathay Cineplexes & more earn SMART$ (worth S$1 each), which can be used to offset future purchases. This spend also counts towards hitting your minimum, working towards earning the highest rebate rate. Finally, UOB One Card has one of the lowest income requirements for foreigners on the market, at just S$40,000. Overall, if you’re likely to spend S$2,000/month on a consistent basis, UOB One Card offers one of the easiest ways to maximise cashback on every transaction. |

Maybank Family & Friends MasterCard: Easy Rebates in SG & MY

| |

If you’re currently living in or spend a great deal of time in Malaysia, Maybank Family & Friends Card is a great option to consider. Cardholders earn for spend in key categories in both Singapore & Malaysia, up to 5% after S$500 spend or 8% with S$800 spend. Rebates cover fast food & food delivery, groceries, transport, petrol data communications/online TV streaming & more. These rates are amongst the highest on market, especially amongst those accessible to lower spenders. Cardholders can earn up to S$80/month, which can be maxed out with just S$1,000 spend.

| |

|

|

If you’re currently living in or spend a great deal of time in Malaysia, Maybank Family & Friends Card is a great option to consider. Cardholders earn for spend in key categories in both Singapore & Malaysia, up to 5% after S$500 spend or 8% with S$800 spend. Rebates cover fast food & food delivery, groceries, transport, petrol data communications/online TV streaming & more. These rates are amongst the highest on market, especially amongst those accessible to lower spenders. Cardholders can earn up to S$80/month, which can be maxed out with just S$1,000 spend.

|

Citi Cash Back Card: Rebates on Global Food & Petrol

| |

Citi Cash Back Card is a great credit card for expats because it rewards key spend categories worldwide, with no merchant restrictions. Cardholders earn 8% cashback on dining, groceries, and petrol both locally and overseas. While there’s a S$800 minimum spend, it’s fairly reasonable that the average consumer will reach this amount as food & petrol comprise nearly half of the average budget.

| |

|

|

Citi Cash Back Card is a great credit card for expats because it rewards key spend categories worldwide, with no merchant restrictions. Cardholders earn 8% cashback on dining, groceries, and petrol both locally and overseas. While there’s a S$800 minimum spend, it’s fairly reasonable that the average consumer will reach this amount as food & petrol comprise nearly half of the average budget.

|

HSBC Visa Platinum: Cashback + Miles for Food & Petrol

| |

HSBC Visa Platinum Card is one of the few credit cards on the market that allows cardholders to earn both cashback and miles. Cardholders earn 5% rebate on local dining, groceries and petrol after S$600 minimum spend, up to S$250/quarter. All other transactions earn 0.4 miles per S$1, with no minimum spend requirement. This rewards structure is great for practical consumers seeking cashback in key spend categories.

| |

|

|

HSBC Visa Platinum Card is one of the few credit cards on the market that allows cardholders to earn both cashback and miles. Cardholders earn 5% rebate on local dining, groceries and petrol after S$600 minimum spend, up to S$250/quarter. All other transactions earn 0.4 miles per S$1, with no minimum spend requirement. This rewards structure is great for practical consumers seeking cashback in key spend categories.

|

Best Credit Cards for Expat Golfers

If you're a frequent golfer looking for privileges at fairways worldwide, this may be the card for you.

Maybank World MasterCard: Best Miles Card for Golfers

| |

Maybank World MasterCard is the best miles-earning card for golfers, including expats. Cardholders receive 2 free green fees/month at 120 fairways across 25 countries. That’s 3x the number of fairways available with the closest competitor, making Maybank World a far more comprehensive option for the avid overseas golfer.

Even if you’re an expat that enjoys the finer things of life, you may be happy to know that Maybank World Card comes with an easy fee-waiver. Cardholders are exempt from the S$240.0 fee with just S$24,000/year spend. Even better, spend on a supplementary credit card (perhaps by a spouse) also counts towards this minimum, making it even easier to avoid the fee. Still, there’s a S$80,000 foreign income requirement. Overall, if you’re an expat seeking no-fee golfing privileges and miles for luxury spend, there’s no better option than Maybank World MasterCard. | |

|

|

Maybank World MasterCard is the best miles-earning credit card for golfers, including expats. Cardholders receive 2 free green fees/month at 120 fairways across 25 countries. That’s 3x the number of fairways available with the closest competitor, making Maybank World a far more comprehensive option for the avid overseas golfer.

Even if you’re an expat that enjoys the finer things of life, you may be happy to know that Maybank World Card comes with an easy fee-waiver. Cardholders are exempt from the S$240.0 fee with just S$24,000/year spend. Even better, spend on a supplementary credit card (perhaps by a spouse) also counts towards this minimum, making it even easier to avoid the fee. Still, there’s a S$80,000 foreign income requirement. Overall, if you’re an expat seeking no-fee golfing privileges and miles for luxury spend, there’s no better option than Maybank World MasterCard. |

American Express Platinum Card: Local Luxuries for Affluent Expats

|

|

Wealthy expats seeking local luxuries may want to consider American Express Platinum Card. Cardholders enjoy a myriad of perks, including 40% off a la carte services at high end spas, dining discounts through Love Dining & Amex Selects, and free drinks at trendy bars through the Chillax programme. Consumers also enjoy waived green fees at fairways across Asia Pacific (with 1 paying guest on weekdays, 2 on weekends).

| |

|

|

|---|

|

|

Wealthy expats seeking local luxuries may want to consider American Express Platinum Card. Cardholders enjoy a myriad of perks, including 40% off a la carte services at high end spas, dining discounts through Love Dining & Amex Selects, and free drinks at trendy bars through the Chillax programme. Consumers also enjoy waived green fees at fairways across Asia Pacific (with 1 paying guest on weekdays, 2 on weekends).

|

Best Shopping & Online Delivery Credit Cards for Expats

Whether you’re looking to save money or prioritise convenience, the following cards will help you earn rewards for shopping and delivery.

OCBC 365 Card: No-Fee Rebates on Daily Essentials

| |

OCBC 365 Card is not only the best no-fee everyday credit card on the market, it also comes with perks uniquely suited to expats without their own car. Cardholders earn rebates on nearly all spend–6% on dining and 3% on groceries, land transport, travel bookings & recurring bills, after S$800 minimum spend.

OCBC 365 Card also stands out by offering a relatively low income requirement for foreigners–just S$45,000–as well as an easy fee-waiver. Cardholders who spend just S$10,000/year (S$833/month) are exempt from the S$192.6 fee, which is already waived for 2 years. This makes OCBC 365 Card accessible, affordable, and incredibly convenient for expats. | |

|

|

OCBC 365 Card is not only the best no-fee everyday credit card on the market, it also comes with perks uniquely suited to expats without their own car. Cardholders earn rebates on nearly all spend–6% on dining and 3% on groceries, land transport, travel bookings & recurring bills, after S$800 minimum spend.

OCBC 365 Card also stands out by offering a relatively low income requirement for foreigners–just S$45,000–as well as an easy fee-waiver. Cardholders who spend just S$10,000/year (S$833/month) are exempt from the S$192.6 fee, which is already waived for 2 years. This makes OCBC 365 Card accessible, affordable, and incredibly convenient for expats. |

POSB Everyday Card: Top Promotional Rates on Essentials

| |

POSB Everyday Card is a great all-in-one card for expats looking to earn rewards while also consolidating their wallets. While promotional rates change with time, cardholders can typically earn as high as 8% rebates on categories such as online food delivery, dining, groceries, transport, personal care and recurring bills. Some categories are merchant-restricted, and most require consumers to meet a minimum spend (Personalised Spend Goal, assigned by DBS). However, as the minimum requirement is based on the individual's average spending levels, it may be easier to consistently reach the minimum than with other more rigid cards.

| |

|

|

POSB Everyday Card is a great all-in-one card for expats looking to earn rewards while also consolidating their wallets. While promotional rates change with time, cardholders can typically earn as high as 8% rebates on categories such as online food delivery, dining, groceries, transport, personal care and recurring bills. Some categories are merchant-restricted, and most require consumers to meet a minimum spend (Personalised Spend Goal, assigned by DBS). However, as the minimum requirement is based on the individual's average spending levels, it may be easier to consistently reach the minimum than with other more rigid cards.

|

Citi Rewards: Best for Online Shopping & Fashion

| |

Do you enjoy shopping online & keeping up with the latest fashion trends? Citi Rewards Card is a great option if you want to earn miles for online & fashion spend. Cardholders earn 10 points (4 miles) per S$1 on online spend (including food & grocery delivery and ride-hailing services), as well as on clothing, bags, shoes & more. You’ll earn rewards for purchases made both locally and overseas. This kind of flexibility is great if you often purchase overseas brands or like to try new styles in different places. Even better, if you want to shop and travel, you can enjoy the card’s free travel insurance. Foreigners must earn S$42,000 annually to qualify, and there’s a S$192.6 annual fee, but it’s waived 1 year. Overall, Citi Rewards Card is a great choice for expats who seeking the convenience of online shopping and flexibility in retail spending.

| |

|

|

Do you enjoy shopping online & keeping up with the latest fashion trends? Citi Rewards Card is a great option if you want to earn miles for online & fashion spend. Cardholders earn 10 points (4 miles) per S$1 on online spend (including food & grocery delivery and ride-hailing services), as well as on clothing, bags, shoes & more. You’ll earn rewards for purchases made both locally and overseas. This kind of flexibility is great if you often purchase overseas brands or like to try new styles in different places. Even better, if you want to shop and travel, you can enjoy the card’s free travel insurance. Foreigners must earn S$42,000 annually to qualify, and there’s a S$192.6 annual fee, but it’s waived 1 year. Overall, Citi Rewards Card is a great choice for expats who seeking the convenience of online shopping and flexibility in retail

|

OCBC Titanium Card: No-Fee Miles for Fashion Retail

| |

OCBC Titanium Rewards Card is the best shopping credit card on the market, for expats and native Singaporeans alike–in fact, no shopping credit card is more comprehensive and versatile. Cardholders earn 10 points (4 miles) per S$1 spend on fashion, electronics, and retail with select merchants like Amazon, Lazada, Qoo10 and many more. Essentially, you can earn rebates for buying everything from shoes to appliances to pharmaceuticals & more.

| |

|

|

OCBC Titanium Rewards Card is the best shopping credit card on the market, for expats and native Singaporeans alike–in fact, no shopping credit card is more comprehensive and versatile. Cardholders earn 10 points (4 miles) per S$1 spend on fashion, electronics, and retail with select merchants like Amazon, Lazada, Qoo10 and many more. Essentially, you can earn rebates for buying everything from shoes to appliances to pharmaceuticals & more.

|

Standard Chartered SingPost Spree: Rebates for Online Overseas Spend

|

|

If you often shop online for overseas brands–perhaps from your home country–Standard Chartered SingPost Spree Card is definitely the best option to maximise rewards. Cardholders earn 3% cashback on foreign online & vPost transactions with no minimum spend requirement–which is perfect if you have a smaller shopping budget and buy from merchants like Amazon. Even better, the card comes with Online Price Guarantee and additional discounts on shipping & packaging.

| |

|

|

|---|

|

|

If you often shop online for overseas brands–perhaps from your home country–Standard Chartered SingPost Spree Card is definitely the best option to maximise rewards. Cardholders earn 3% cashback on foreign online & vPost transactions with no minimum spend requirement–which is perfect if you have a smaller shopping budget and buy from merchants like Amazon. Even better, the card comes with Online Price Guarantee and additional discounts on shipping & packaging.

|

Learn More About How to Find the Best Credit Card for You

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.