Fixed vs. Floating Rate: Which is Better for Your Home Loan?

One of the most challenging tasks when shopping for a home loan is to choose between a fixed rate loan or a floating rate loan. Is fixed rate always better than floating rate, or vice versa? To answer this question, you have to form your opinion about how rates will behave in the next 2 to 3 years while your loan is locked up, and how that impacts your overall cost. Below, we discuss a few possible scenarios that you should consider and how to take advantage of each type of loans in these situations.

Your Strategy Depends on the Interest Rate Environment

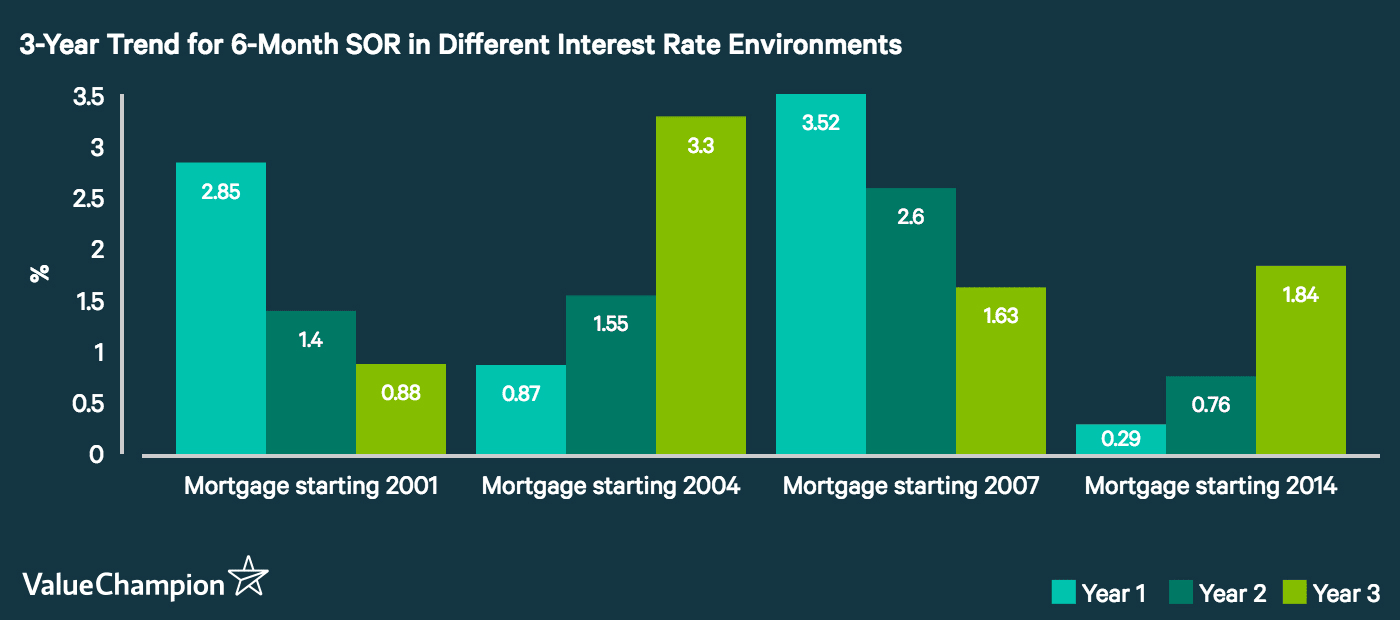

How much your bank charges you for interest depends on how the interest rates are moving in the Singaporean economy. In general, you should try to lock into favorable rates when the interest rate is low by getting a fixed-rate loan, and let your mortgage rate float when you believe interest rates are likely to decline in the next 3-4 years. To assess the impact of choosing the right interest rate in a given interest rate environment, we've collected the historical rates for 6-month SIBOR and SOR between 2000 and 2017, and analysed the total interest cost on the home loans starting each year.

Fixed Rate Is Better in a Rising Interest Rate Environment

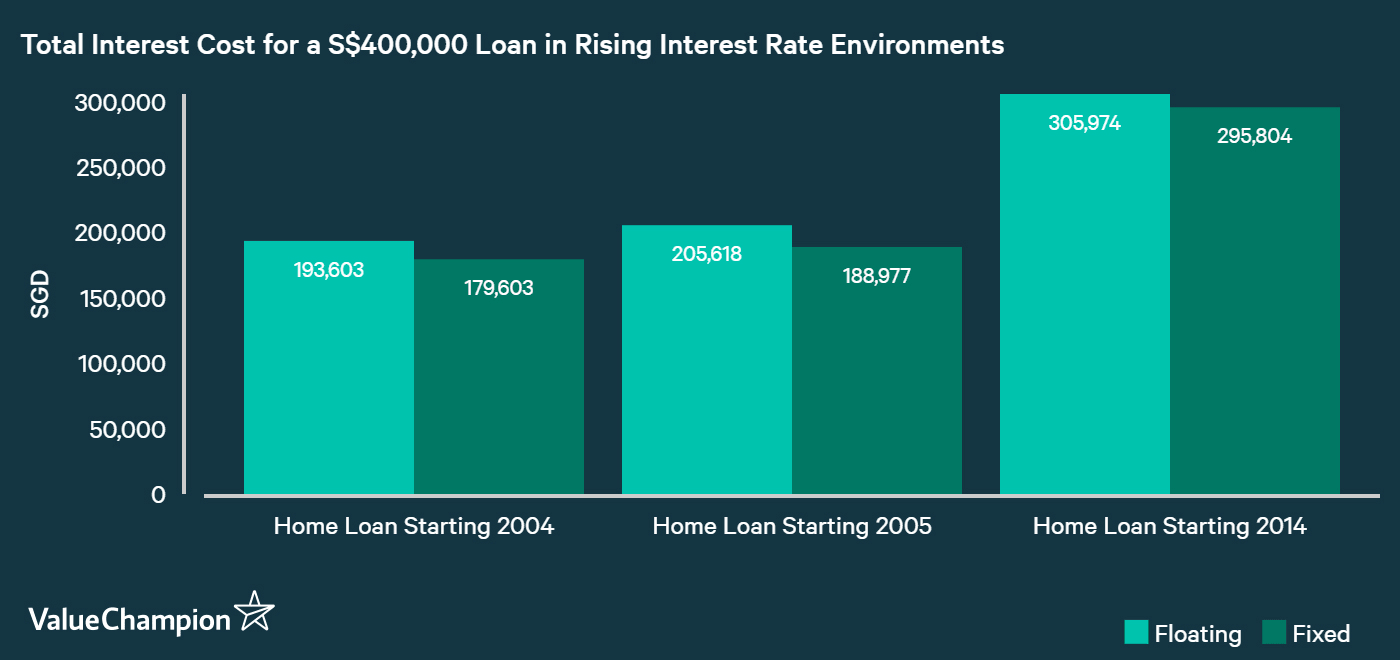

When the interest rate is rising, fixed-rate loans can give you up to 10% of cost savings by locking in the current (low) interest rate. According to our analysis of 2000-2017 historical interest rates, you could save as much as S$16,641 by choosing fixed rate if you took out a loan of S$400,000 in 2005, when the market rates began to rise steeply. These estimates are based on interest rate of 0.50% plus the benchmark 6-month SOR, a 3-year fixed-rate period. We also assumed that the rate continues to rise to 5.00% until 2022, after which the rate stays constant.

The result consistently held true for all three time periods, as long as they represented a rising interest rate environment. For instance, you would've save about S$10,169 in interest cost compared to floating rate if you took a fixed-rate mortgage starting 2014, because interest rates have been steadily rising during 2014-2017.

Floating Rate is Better in a Flat-to-Declining Interest Rate Environment

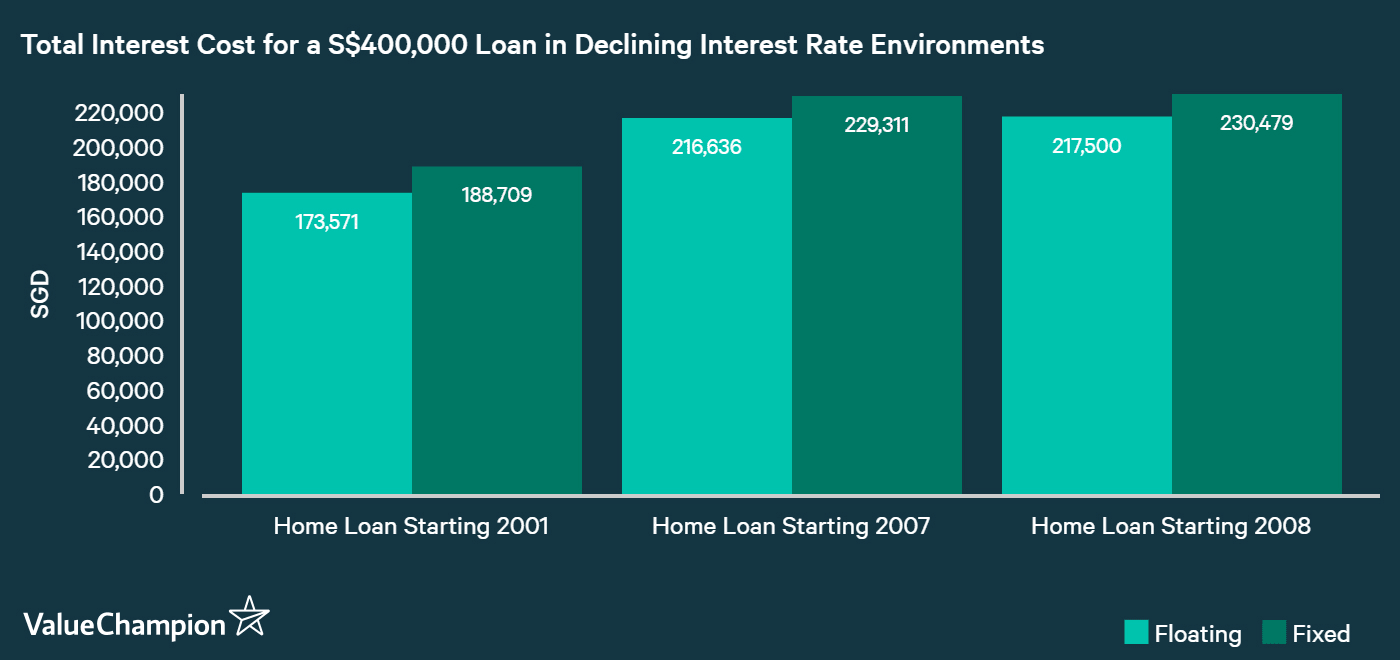

In a flat-to-declining interest rate environment, you can save up to 8% of interest cost by choosing a floating interest rate, according to the same analysis as above. We can find a prominent example in year 2007, when the 6-month SOR peaked out at 3.52%. As the interest rate kept declining, the floating rate adjusted each year to the lower market rate, but fixed-rate loans were locked in at these sky-high rates. As a result, you could've saved about S$12,675 or 6% of total interest cost if you took out a floating rate loan of S$400,000 in 2007, compared to its fixed-rate counterpart.

It is also generally more advisable to get a floating rate loan in a flat interest rate environment. This is because banks typically charge you higher interest on fixed-rate loans in order to reflect the premium you are getting from knowing exactly how much to pay each month.

The First Three Years Matter the Most

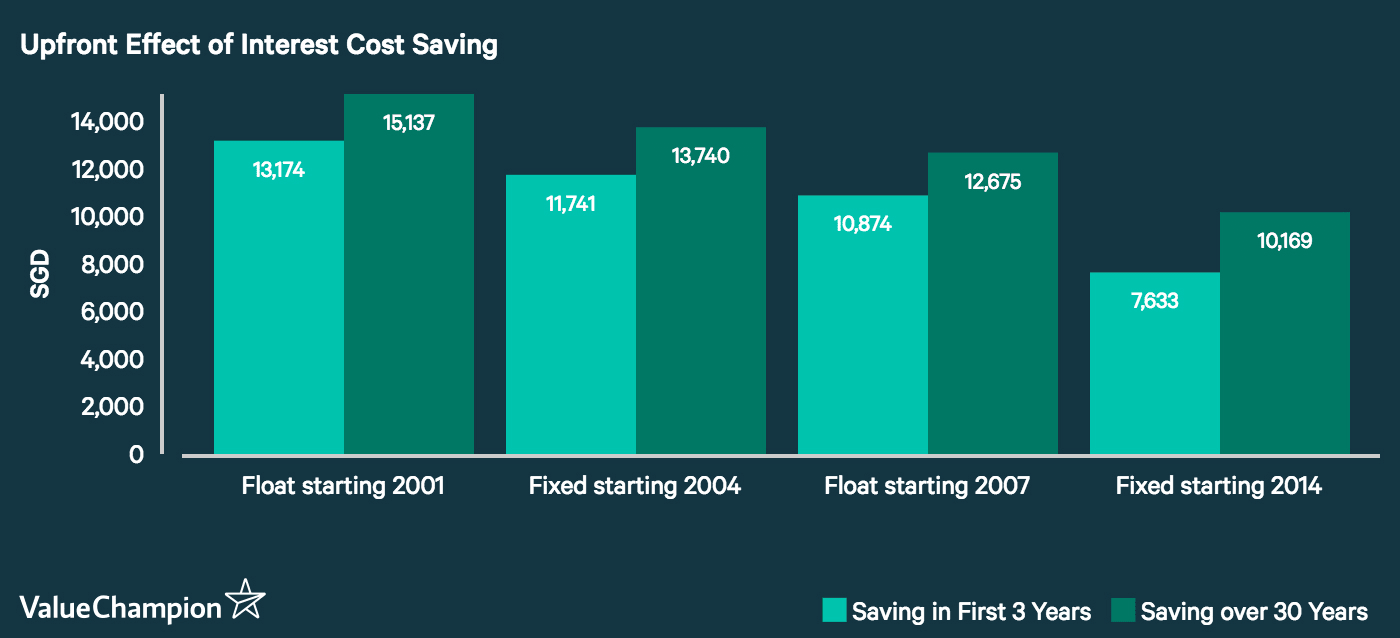

Because the fixed-rate period typically lasts for 3 years, almost all of your interest cost savings happen during that time. This means that if you took out a fixed-rate loan of S$400,000 in 2005, over 86% (S$14,382 out of S$16,641) of the savings would come in during the first three years, while the remaining 14% happens over the remaining 27 years. This also represents about 38% of interest cost reduction in the first three years. The ratios stay relatively constant regardless of which year the mortgage starts, meaning that the majority of your net position is determined in the first three years, unless you choose to refinance your mortgage.

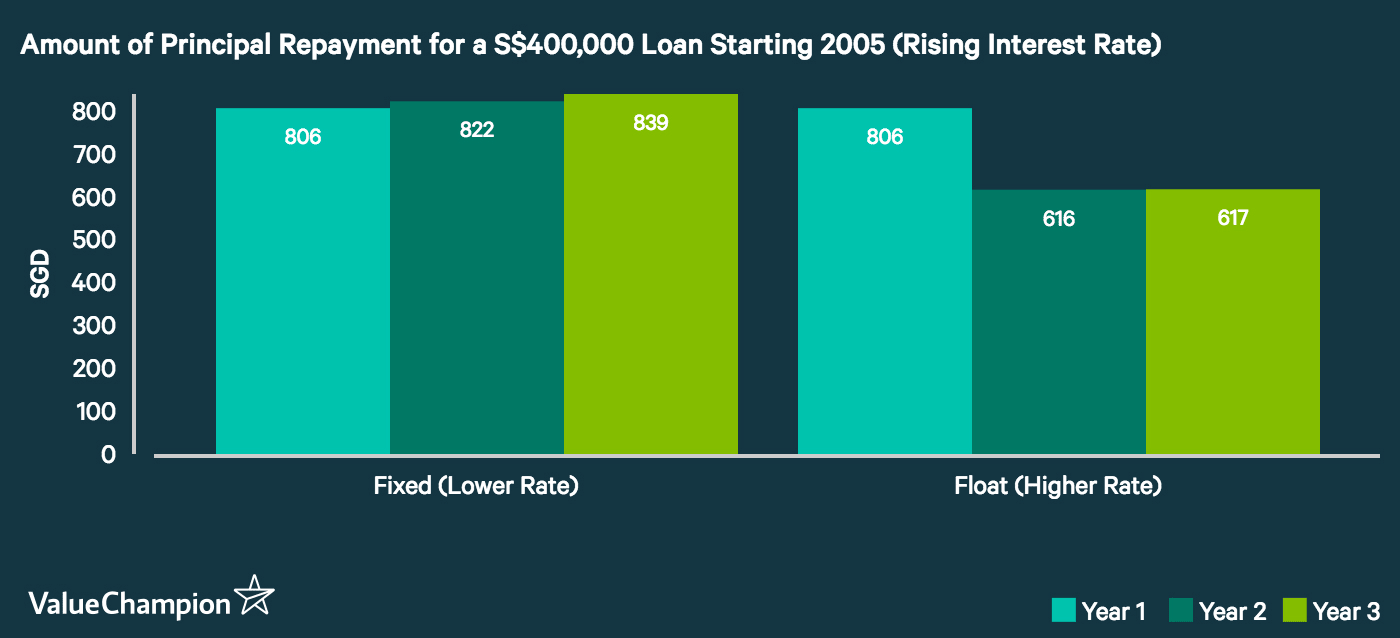

Low Interest Rate Also Helps You Pay Down More Debt

Not only does low interest rate reduce your cost in the first three years. In fact, it can also help you pay down relatively more principal each month, which in turn helps you pay less interest down the road. Let's take a look at an example of how this would have worked in your favor in 2005, when the interest rate was rising. If you took out a S$400,000 mortgage loan with fixed rate, over 50% of your payment in the first 3 years would've been "principal repayment." This is beneficial for you because principal repayment decreases your outstanding debt balance, which ultimately results in less interest costs. However, if you took the same loan with floating rate, only about 30% of your payment in the second and third years (2006 and 2007, respectively) would go to pay down your debt.

Which Interest Rate Environment Are We In Now?

Now you're armed with the appropriate strategy for both the rising and declining interest rate environments, you might wonder which one exactly we belong to now. While it's impossible to predict the immediate future, we can look at a few factors to understand where rates are headed in the long-run. For example, SIBOR and SOR are highly correlated with the U.S. interest rates, as discussed in one of our previous articles. We also know that the U.S. Federal Reserve plans to roll out its plans to tigthen its monetary policy and raise the U.S. interest rate. It is impossible to make interest rate predictions, but you should take into account these things when thinking about your strategic move.

Refinancing is a Double-Edged Sword

Refinancing wisely over the life of a loan can help you double down on savings by locking in low interest rates for multiple rounds of 3-year periods. According to our analysis, if you took out a floating-rate home loan of S$400,000 benchmarking 6-month SOR in 2005, there would've been at least one chance to refinance to a fixed rate loan in 2015, which would've given you S$14,481 or 7% of cost savings compared to if you never refinanced your floating-rate loan.

Despite these amazing savings, refinancing comes with two caveats: upfront refinancing costs and unpredictability of interest rate. First, banks usually require refinancing charges including legal & valuation fees, which can easily add up to S$3,000 (although some lenders have special terms that waive these obligations). In light of this, we advise our readers to compare the costs & benefits of refinancing and calculate their breakeven points for refinancing in order to make the most informed decision.

In addition to the upfront costs, refinancing also involves the risk that your prediction about interest movement might be wrong. For example, let's say you are in 2012 and have never refinanced your loan. Because the 6-month SOR has been going up between 2011 and 2012, you decide to lock into the 2012 rate of 0.58% by refinancing your loan. However, we can only know from hindsight that this was a bad move: 6-month SOR declined through 2013 and 2014 to as low as 0.29%, which means you should've not refinanced your loan and instead should've continued with the floating interest rate.

Parting Thoughts

Taking out a home loan to purchase a property is a daunting exercise, and choosing the right type of interest rate for such a big commitment can be a headache. In general, you should get a fixed rate in a rising interest rate environment, and get a floating rate loan when rates are declining. You should also consider refinancing during the life of your loan, when you believe the rate has hit a low point or if you find another lender that gives you a much better term. No matter what you do, you should do some research on interest rates like SIBOR and SOR as Singaporean loans are largely tied to these benchmarks, in order to make a rewarding personal finance decision.