Rent or Own, Which Is Better For You?

Renting, rather than owning, is becoming increasingly popular in one of the world's most expensive property markets. But is it the best option for you? In order to answer this question, you should compare the pros and cons of owning versus renting based on your needs and circumstances. To help you sort through this process, below we discuss the benefits and costs of each option and some advice for prospective property buyers.

| Pro | Con | |

|---|---|---|

| Owning |

|

|

| Renting |

|

|

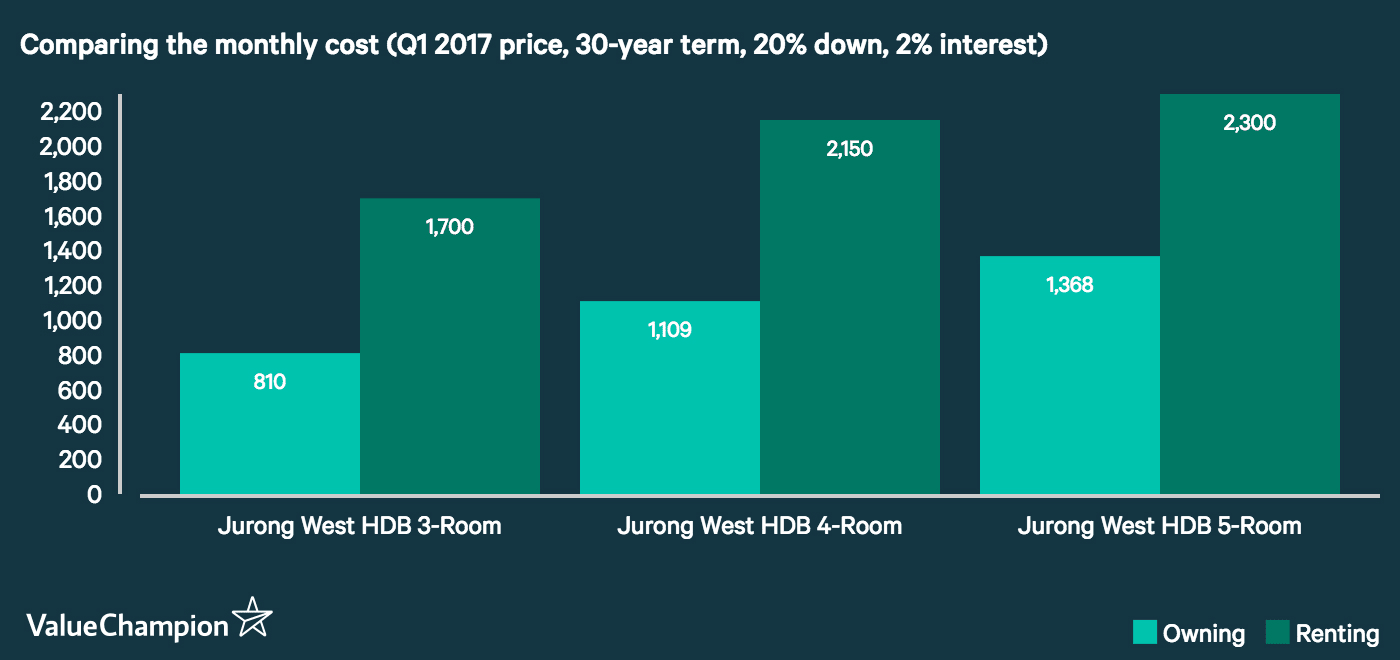

Owning is cheaper in most cases, with some caveat

Contrary to the increasingly popular belief that renting is better, owning still represents a more economic choice for most Singaporean properties. According to our analysis of HDB's 2013-2017 data on median rent and resale prices, the monthly cost of owning can be 15-50% cheaper than the rent for a comparable property. This is assuming that each month, you are paying back your 30-year home loan that requires 20% down payment and charges 2% interest rate. In addition to HDB flats, private properties showed similar results: you pay less on a home mortgage every month than you would for rent.

Not only is owning cheaper, it also entitles you to many other benefits such as the potential profit of reselling if you decide to do so. As you pay off your loan, your equity in the property gradually increases until you command full ownership of your home. In contrast, if you rent a property, the monthly rent you pay represents an expenditure, meaning it's just spent rather than being used to build an asset that belongs to you, and can appreciate in value.

Although investing rather than spending sounds like a savvy thing to do, you should be aware of the potential risk of borrowing money to buy an asset. Buying a property requires a down payment, which represents upfront cost. Typically, a Singaporean mortgage loan requires 20% of down payment, which means you need to submit at least S$100,000 if you are to finance the purchase of a S$500,000 property. Depending on your financial situation, surrendering this amount of money can simply be impossible. Not only that, it will reduce your spending capability, which represents an opportunity cost if you have limited savings. Last but not least, if your property price goes down, your home might lose value and you might suffer a significant financial loss.

It should be noted that there are many forms of financial assistance to help you reduce the cash component of your down payment. This means that even if your 20% mortgage loan requires you to put together S$100,000, you can use non-cash sources to subsidise this payment. These include government grants, as well as the money in your CPF Ordinary Account. Such financial assistance programs are typically available for HDB properties and private executive condominiums.

Owning comes with other hidden costs

Besides the large down payment, owning a home also comes with many hidden costs. For example, most Singaporean properties have 99-year leaseholds, which means you do not actually own the property forever, even if you pay down all of your mortgage. If you intend to pass your property down multiple generations, therefore, HDB flats are not a suitable investment because when the leases run out, flats will be returned to HDB, who will in turn have to surrender the land to the government. Your better bet is private properties with 999-year leasehold or permanent ownership, but these are harder to find and more expensive.

Finally, reselling your property for profit comes with some barriers. These include transaction costs that you need to pay to your broker and the bank, potential damages to the property during one's residence, and the penalties for breaking up the loan. For example, if you resell your property before fully paying down the loan, you have to spit out the government grant that subsidised your purchase, plus interest. Not only that, if you also used your CPF account to finance your purchase, there are interest incomes you could've earned on that CPF money which represents opportunity cost.

Renting is better for short-term tenants, especially in high-end properties

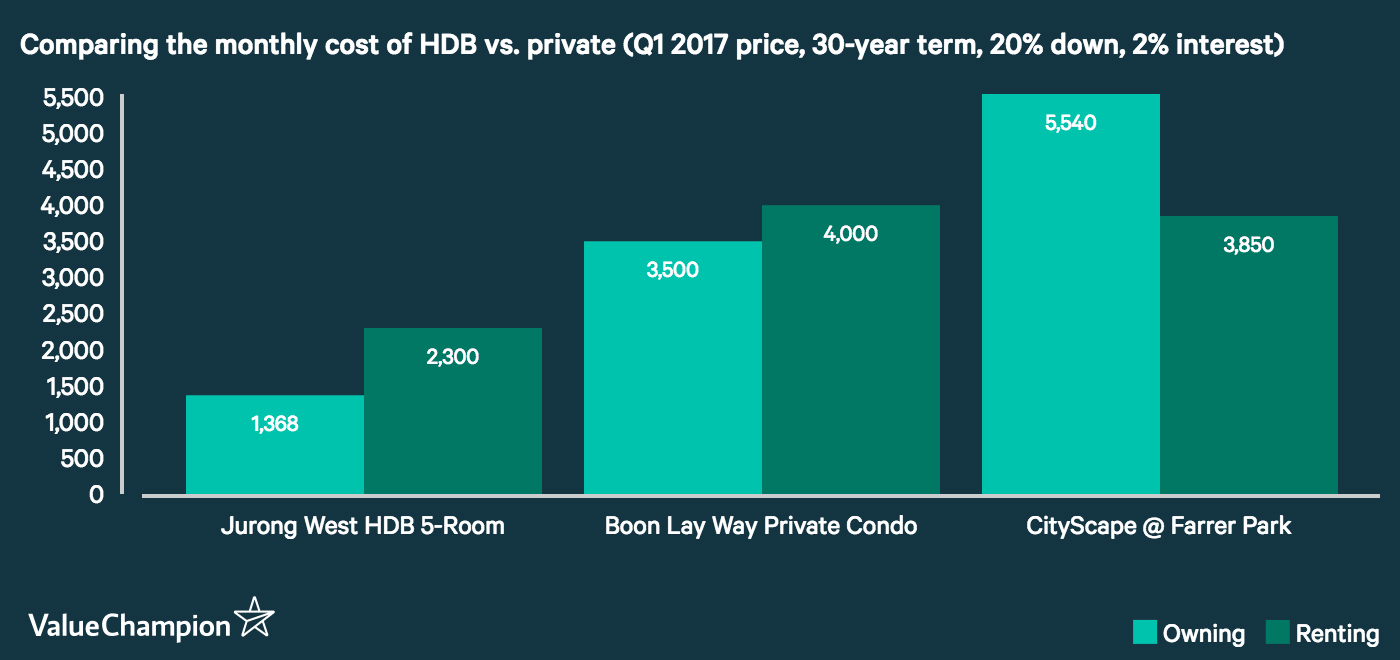

You should consider renting if you intend to be a short-term resident in high-end properties like private condos or executive flats. While this may not always be cheaper on a monthly basis, you can save a lot on down payment which is a big upfront cost as discussed above. Not only that, the difference between monthly mortgage payment and monthly rent narrows for higher-end properties, so the extra cost you have to pay might be worth it if you don't intend to eventually own the property.

For instance, you can rent a private condo on Boon Lay Way in Jurong West for about S$4,000 per month, which costs only 10-20% more than the monthly mortgage for this S$1,000,000-property. In a more extreme example, buying a property in Cityscape at Farrer Park, a high-riser located near the city center, can result in a higher monthly expenditure than just renting. Our analysis shows that renting this property can be cheaper by about 15% than repaying a mortgage based on your monthly payment.

Other considerations for property investors

Although we used monthly payment above as a way to compare the cost of renting and owning, there are many other factors that can potentially influence an investor's decision to buy a property. From the market's perspective, this includes all of the strategic considerations: the property's location, brand name, as well as regulation on the real estate market. These represent external factors that are important determinants of your property's market value at resale.

Interest rate movement is also a major consideration whose importance cannot be exaggerated. In a rising interest rate environment, property prices tend to peak out and start declining. This indicates a favorable condition for renting, because your rent will adjust more favorably than your mortgage: rent declines with lower property prices, while mortgage payment increases with higher rates. Not only that, owning a property during a market downturn can result in significant financial losses. Conversely, in a declining interest rate environment, the opposite is true: property prices are likely to be at a low point, and you might be able to find good investments that are undervalued. In contrast, your rent can rise along with the rising property market. Your decision to invest in the property market, in all cases, should be based on your beliefs about where the market interest rates and the property market is headed.

Aside from these market considerations, you should also optimise the leverage you use. Because leverage gives you greater exposure to volatility in the roller coaster-like property market, you should be careful of its mixed blessings. Let's take a look at an example of how this works. For a S$500,000 property, you can take out a home loan with down payments of 25% or 10% (leverage of 75% or 90%, respectively) hoping to make profit by turning the property around. In three years, if your property price declines by 10%, your loss over the three-year period is 17.4% if you started with a 75% leverage. However, this loss can increase significantly to 32.3% if you had started with a higher leverage of 90%.

| 75% Leverage | 90% Leverage | |

|---|---|---|

| Initial Price | S$500,000 | S$500,000 |

| Less: Initial Loan | S$375,000 | S$450,000 |

| Initial Equity | S$125,000 | S$50,000 |

| In three years, your property's market value goes down by 10% | ||

| Property Value | S$450,000 | S$450,000 |

| Less: Remaining Debt | S$346,787 | S$416,144 |

| Remaining Equity | S$103,213 | S$33,856 |

| Loss | 17.4% | 32.3% |

As you can see from this example, you are exposed to greater downside risk if your leverage increases. Therefore, we advise our readers to arrange their investment structure and use leverage carefully, in a way that is suitable for their risk tolerance.

Parting Thoughts

Owning a home can help you invest in an asset that you own, while keeping monthly payments low. In contrast, renting is an expense, not an investment, but requires less commitment and responsibility attached to home ownership. Although some macroeconomic factors indicate favorable conditions for renting, we still think you should evaluate all of the pros and cons in order to make the most informed decision. Finally, bear also in mind that your investment return in the property market will depend on where you think market is going, and how you finance your investment.