Secured vs Unsecured Loans: What's Right For You?

In general, loans can be divided into two major categories: secured and unsecured. A secured loan is "secured" by an asset called collateral that the lender can seize if you don't repay the loan. In contrast, an unsecured loan does not require any collateral and is lent solely based on your creditworthiness and ability to repay. Because there's no underlying asset securing the loan for the lender, these loans tend to carry meaningfully higher interest rates than do secured loans. In this guide, we explore the difference between secured and unsecured loans in detail, and discuss some innovative ways of utilising these loan types.

Table of Contents

Secured Loans Vs Unsecured Loans

There a few major differences between a secured loan and an unsecured that are worth highlighting. First and foremost, the biggest difference between the two is what happens when you stop making payments, or default, on the loan. For secured loans, the lender has the right to seize the pledged asset (also called collateral) from the borrower to recuperate his loss without going to court. For example, home loans and car loans are the most common types of secured loans, where your home or car serve as the collateral, and you could lose your home or your car when you default on your home loan or car loan. However, this is a rather dramatic result, and usually defaulting borrowers get a chance to make good on their debt (with some additional fees) without losing their assets. Nevertheless, being late on your payments will hurt your credit scores.

In contrast, you don't have to pledge any assets to secure an unsecured loan, so you don't actually stand to lose your assets when you don't make good on your debt. However, there are severe consequences for defaulting on your unsecured loans, as it can seriously ruin your credit score and prevent you from ever getting other loans or even credit cards in the future. The most well known examples of an unsecured loan are personal loans and credit cards.

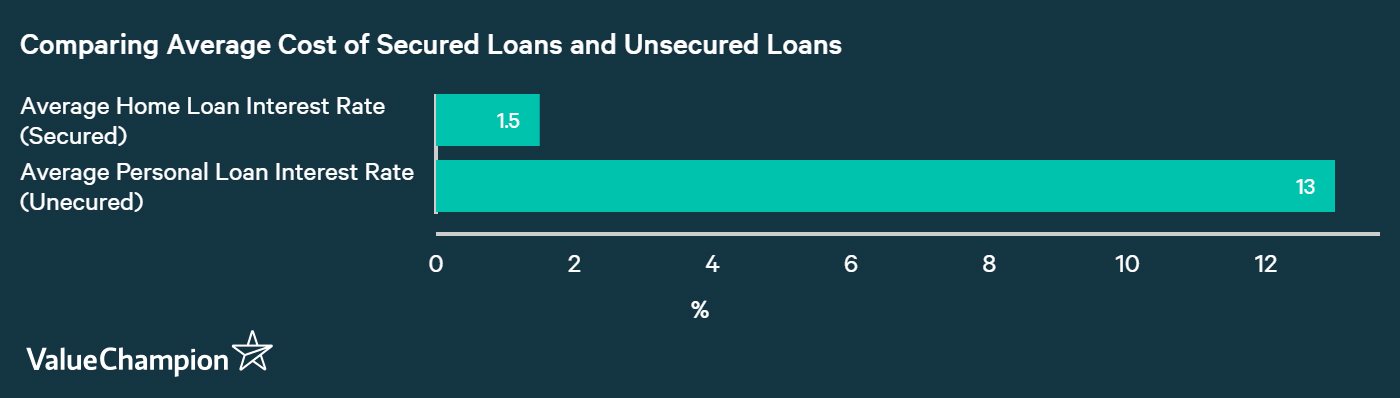

The second major difference is there interest rates. Since the lender has an asset to back a secured loan, they are willing to provide the fund at a lower rate than they are for unsecured loans. Therefore, the average interest rates for personal loans tend to be couple times higher than the average interest rates of home loans.

Innovative Applications of Secured & Unsecured Loans

There are couple ways that you can use these different loan types in innovative ways when you are in need of extra capital.

First up is a home equity loan. It is a type of secured loan that allows borrowers to get a loan against the value of their home that has been paid off already. By pledging your home's equity value as collateral, you can get a secured loan that is as much as 10% cheaper than your conventional personal loan. In fact, these loans tend to cost only a few basis points higher than normal home loans.

Secondly, a refinancing cash-out loan is great for people who have paid a chunk of their home or car loan back but still owe money on the original loan. In some cases, the borrower can take out a new loan for an amount that’s higher than the original one. Therefore, if you need some extra cash, you can use the new loan to pay off the original and use the leftover cash.

Lastly, you can sometimes secure your personal loan (which would otherwise be unsecured) with your savings account or certificate of deposit with the lender. This could help reduce the high interest rate that usually comes with an unsecured personal loan. If your account is close to maturity, however, you may want to wait a bit longer to use the money you've saved up instead of getting the loan and ultimately incurring extra cost in interest payment.

Parting Thoughts

Whether you are getting a secure loan or an unsecured loan, your ultimate goal should be to always minimise the interest cost while borrowing the minimum amount that you absolutely need. Loans can be costly and failing to repay them on time can have long-term consequences that can negatively impact your life.

Also, if you’re rejected for both unsecured and secured loans, you should still avoid going to money lenders or resort to getting a payday loan, as they come with an astronomically high price tag. There are better alternatives if you really need the money. For instance, even a credit card debt is cheaper than a loan from a money lender. Not only that, pawn shops offer surprisingly low rates as long as you are able to pledge an asset that's valuable enough to secure the amount of money you need.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.