Everything You Need to Know To Optimise Credit Card Rewards Points Redemption

Get the Best Credit Cards in Singapore

If you're not earning cashback, chances are you're earning points for your credit card spend–even if rewards are advertised as miles. In most cases, cardholders earn a designated amount of points for every S$1 spend. These points are then credited to an online account (rather than automatically offsetting the card statement, as with a rebate card), and can be redeemed on an online rewards platform for merchant vouchers, cash credits, air miles and more.

Each redemption value is different, however–both the voucher amount and the number of miles required for redemption can vary dramatically across merchants and rewards types. This makes it exceedingly difficult to discern the value-per-point for each option–so how do you know whether or not you're making the most of your hard-earned rewards? We've analysed 331 rewards options from 5 of Singapore's leading banks to provide greater insight into how to optimise your points conversions when you're ready to redeem rewards.

Table of Contents:

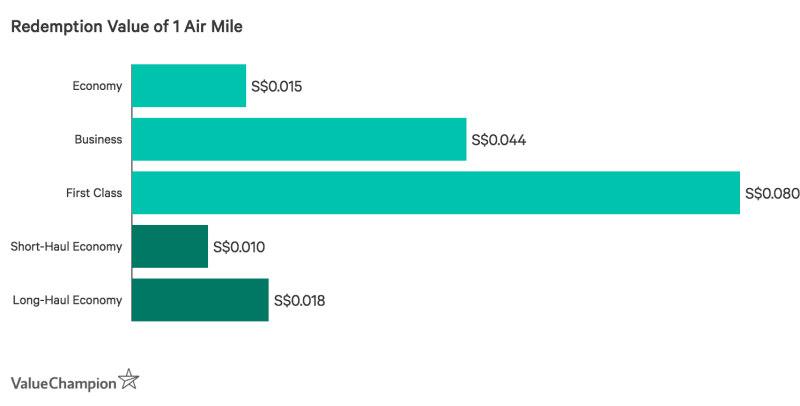

Miles Have the Highest Redemption Value

You'll often find that credit cards that technically earn points advertise their rewards as air miles. There's a reason for this–the redemption value of 1 point for 1 air mile is almost always higher than what you'd get with any other type of rewards option. Essentially, if you're looking to maximise the value of the rewards you've earned, you should always opt to convert your points to air miles. This is generally true no matter what type of traveller you are, though ultimate redemption value does vary based on your ticket booking. The average value of 1 mile redeemed for a shorter flight is lower than its value if redeemed for a longer flight. Additionally, redeeming miles for business and first class tickets provides even greater value-to-consumer.

Redeeming points for miles does have a few drawbacks, however. To begin with, cardholders typically need to first redeem points for air miles, which are then credited to their corresponding frequent flyer account. Consumers must then redeem these miles on the airline platform when they actually book a flight–so two steps are involved, rather than just one. Additionally, many issuers charge consumers S$26+ for every points-to-miles conversion, or S$42+ to cover automatic conversions across a full year. These costs can quickly cut into ultimate value-to-consumer, unfortunately. Finally, there's little use to converting points to miles if you rarely (if ever) travel. Once points have been converted to miles, they may expire within a few years (3 years with KrisFlyer). As a result, while the redemption value of 1 mile is higher than that of most other options, it's important to consider your own lifestyle and needs.

Department Store Vouchers Have the Lowest Redemption Value

If you aren't interested in redeeming your rewards points for miles, you should at the very least avoid department store vouchers. Most banks offer vouchers valued at anywhere from S$10–S$100+ at outlets such as TANGS, Al-Futtain Retail Asia, Takashimaya, Isetan and more. While these may seem like a "safe bet" for redemption–given the huge selection at these stores, it's almost guaranteed you'll find enough to spend your full voucher on–the ultimate value-to-consumer for these vouchers is actually amongst the lowest of all possibilities on just about any bank's rewards platform.

Average Redemption Value of 1 Point, By Category

| Rewards Category | Average Redemption Value |

|---|---|

| Air Miles | S$0.0127 |

| Cash / Waiver | S$0.0041 |

| Petrol | S$0.0035 |

| Entertainment | S$0.0033 |

| Retail (Store-Specific) | S$0.0031 |

| Dining | S$0.0030 |

| Department Store | S$0.0027 |

In some cases, the value of 1 point redeemed for a department store voucher can be as low as 13% of its value when redeemed for 1 air mile. The redemption value for department store vouchers is also typically lower than the value for merchant-specific vouchers. As a result, you may want to consider redeeming your points for a voucher from your favourite brand instead. You might also want to consider applying for a shopping credit card. The elevated rewards you'll earn from spending at these shopping outlets are, in a way, a form of discount in themselves.

Difference in Redemption Value By Category Varies By Bank

As seen above, the value of a point often differs by rewards type–miles tend to have higher value, while department store vouchers have amongst the lowest. However, banks also offer rewards in categories such as cash credits or fee waivers, dining, entertainment, merchant-specific retail and petrol. While the redemption value of miles is meaningfully higher than any other options in almost any bank, the remaining categories may have their own degree of variation, or lack thereof.

For example, Standard Chartered and OCBC both offer a comprehensive array of rewards, but beyond miles, the redemption value per option is quite flat. This means that the value of 1 point, whether redeemed for a dining voucher or for a movie ticket, is about the same. This is great for cardholders who prefer to redeem rewards in a variety of categories or who may want to switch up their selection without having to worry about optimising their redemption.

Average Redemption Value per 1 Point By Category, By Bank

| Category | SC | OCBC | UOB | HSBC | DBS |

|---|---|---|---|---|---|

| Air Miles | S$0.0097 | S$0.0134 | S$0.0137 | S$0.0134 | S$0.0134 |

| Cash / Waiver | S$0.0036 | S$0.0028 | S$0.0022 | S$0.0048 | S$0.0071 |

| Petrol | S$0.0037 | S$0.0029 | S$0.0033 | S$0.0045 | S$0.0031 |

| Entertainment | S$0.0040 | S$0.0026 | S$0.0020 | S$0.0040 | S$0.0039 |

| Retail (Store-Specific) | S$0.0038 | S$0.0027 | S$0.0024 | S$0.0033 | S$0.0032 |

| Dining | S$0.0039 | S$0.0026 | S$0.0020 | S$0.0035 | S$0.0031 |

| Department Store | S$0.0037 | S$0.0026 | S$0.0018 | S$0.0028 | S$0.0028 |

Other banks, however, have more value-variegated options. Both HSBC and DBS's rewards programmes offer varying redemption values, on average, per category. In both cases, cash credits and/or fee waivers have particularly competitive redemption values (though still lower than for miles). While the differences between other categories may seem small, the percent change from one to the next can range up to 45%–even when considering small values, this difference adds up when 1,000s of points are redeemed at once. In these cases, consumers may want to redeem their points for rewards only in higher-value categories.

Points Earned from Equal Spend Are Weaker with Some Banks Than Others

On a final note, the potential return-value of S$1 spend can actually vary from bank to bank. To clarify, it's easy to calculate the redemption-value of 1 point within a given bank. This is helpful if you're looking to redeem points from a credit card that you already own. However, this analysis cannot be compared cross-bank because it may be easier to earn 1 point with a credit card from one bank than with another. For example, you might earn 1 point per S$1 general spend with an HSBC credit card, but earn 1 point per S$5 spend with a DBS credit card. When calculating redemption values on its website, it may seem like the value of 1 point earned from DBS is remarkably high–but that's because it's harder to earn. To facilitate an even analysis, we've standardised point earnings across the 5 banks reviewed, defaulting to the base rate for every S$1 spend. The table below shows the ultimate return value-to-consumer per S$1 general spend across multiple categories and banks.

Total Average Return-Value Per S$1 Base Rate Spend, By Bank

| Category | UOB | OCBC | SC | HSBC | DBS |

|---|---|---|---|---|---|

| Avg Redemption Value (inc. Miles) | S$0.0039 | S$0.0042 | S$0.0046 | S$0.0052 | S$0.0052 |

| Avg Redemption Value (exc. Miles) | S$0.0023 | S$0.0027 | S$0.0038 | S$0.0038 | S$0.0039 |

In general, the return value of spend with a points-earning DBS credit card or HSBC credit card is higher than that with an OCBC or UOB credit card, for equal spend at a base rate.

However–this offers just one point of perspective. It's essential to remember that cardholders ideally should opt for a credit card that offers boosted rates (above the base rate) for transactions in the categories they spend the most on. If you're earning just at the base rate, you may want to consider a different credit card. Also, some credit cards–especially travel cards–offer a completely different type of point for purchases; these points may have a separate value system (for example, OCBC 90°N Card earns Travel$, not OCBC$). Finally, some points-earning travel cards lack typical base rates; cardholders earn a certain rate for local and overseas transactions that varies from card to card, so there isn't a "bottom catch-all" rate for non-category spend. DBS Altitude Card is one such card where this applies.

Conclusion

Ultimately, if you have a points-earning credit card, remember to check on the redemption value for the options you're interested in. While you can use the data above as a benchmark if you have a card with one of these banks, you can quickly check the value for yourself for a specific option by dividing the voucher value by the number of points. You can then compare the resulting values to determine which is highest, and therefore, the optimal choice. If you are a traveller, however, you can take a shortcut and opt for miles as these conversions almost always offer the highest return value.