Best Maybank Credit Cards 2024

As the biggest bank in Malaysia and the fourth biggest bank in Singapore, Maybank boasts a robust set of credit cards for Singaporeans. To help you find your ideal card, our experts have handpicked several Maybank credit cards with outstanding features and value propositions.

- Maybank Horizon Visa: Market-leading 3.2 miles per S$1 select local spend

- Maybank Family & Friends: 8% cashback with S$800 min. spend requirement

- Maybank FC Barcelona: Highest unlimited local rebate–1.6% on all spend

- Maybank Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- Maybank World: Free green fees at 100 fairways across 19 countries

- Maybank eVibes: Highest rebate for students–1% on all spend

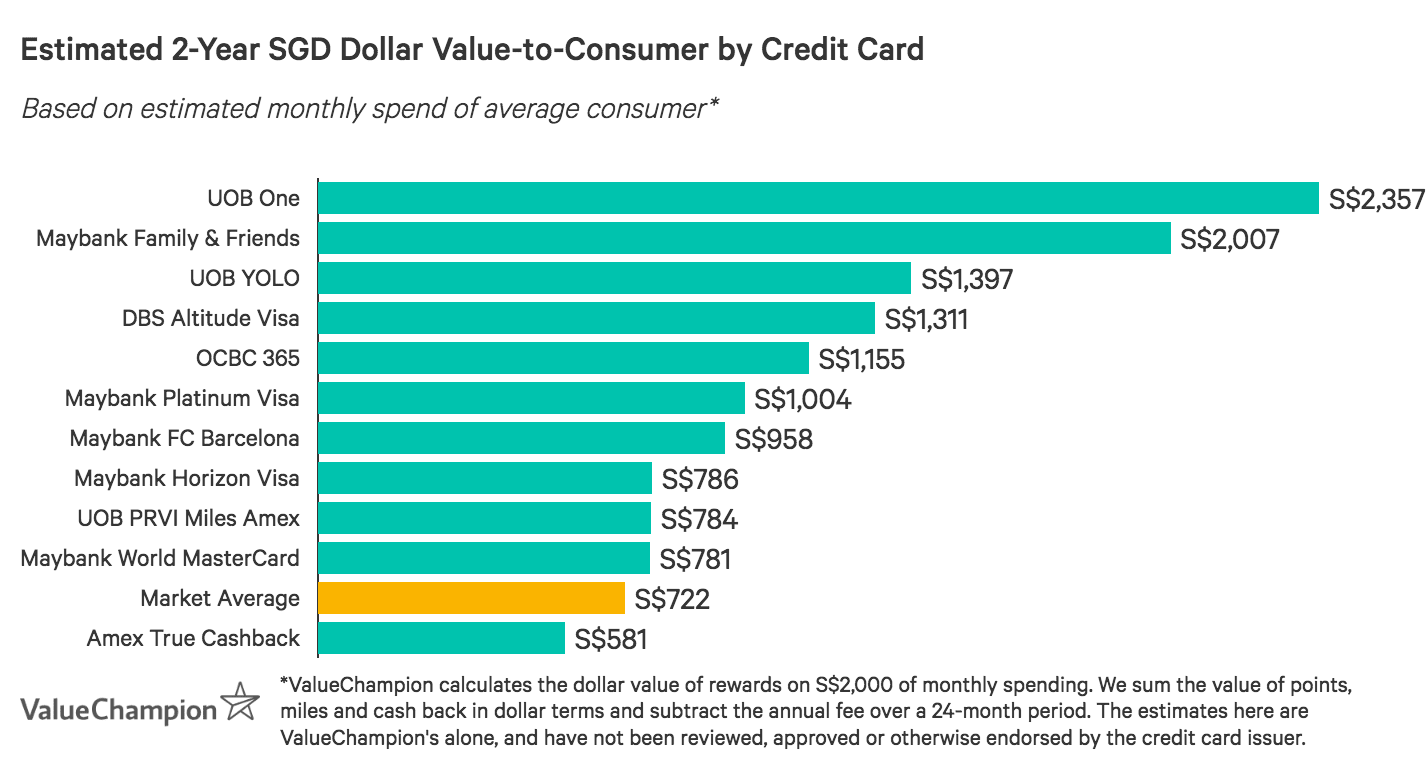

Compare Best Maybank Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best Maybank credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

- Market-leading 3.2 miles per S$1 select local spend

- 8% cashback with S$800 min. spend requirement

- Highest unlimited local rebate–1.6% on all spend

- Up to 3.33% rebate on local and foreign currency spend

- Free green fees at 100 fairways across 19 countries

- Highest rebate for students–1% on all spend

Compare Best Maybank Credit Cards by Dollar Value

Based on an average monthly spend of S$2,000, we analysed the best credit cards on the market to estimate returned value-to-consumer after 2 years, accounting for rebates and netting out annual fees. As a note, dollar value is heavily dependent on spending habits; intangible benefits (like free travel insurance and airport lounge access) are valuable but difficult to quantify.

Maybank Horizon Visa Signature: Top Miles for Local Spend

| |

Maybank Horizon Visa Signature Card offers the highest miles rewards rate for local spend on the market–in addition to impressive overseas rates & travel perks. Cardholders earn 3.2 miles per S$1 spend on local dining, taxis & Grab, petrol, and hotel bookings with Agoda. Most travel cards offer just 1.1–1.4 miles per S$1 local spend.

Maybank Horizon Card also comes with a few perks. Cardholders enjoy free travel insurance and airport lounge access. Even better, cardholders who spend S$18,000/year (about S$1,500/month) are exempt from the S$180.0 fee. Very few traditional travel cards come with fee waivers. Overall, if you spend a great deal of your budget locally but want to earn miles rewards, there’s no better option than Maybank Horizon Card. | |

|

|

Maybank Horizon Visa Signature Card offers the highest miles rewards rate for local spend on the market–in addition to impressive overseas rates & travel perks. Cardholders earn 3.2 miles per S$1 spend on local dining, taxis & Grab, petrol, and hotel bookings with Agoda. Most travel cards offer just 1.1–1.4 miles per S$1 local spend.

Maybank Horizon Card also comes with a few perks. Cardholders enjoy free travel insurance and airport lounge access. Even better, cardholders who spend S$18,000/year (about S$1,500/month) are exempt from the S$180.0 fee. Very few traditional travel cards come with fee waivers. Overall, if you spend a great deal of your budget locally but want to earn miles rewards, there’s no better option than Maybank Horizon Card. |

Maybank Family & Friends Mastercard: Best Rebates for SG & MY

| |

Maybank Family & Friends Card is an excellent choice if you split your time–and budget–between Singapore & Malaysia. Cardholders earn 8% rebate in both countries on 5 key categories (groceries, fast food & food delivery, transport & more) with just S$800 monthly spend which makes it easy for low spenders to earn at high rates. At this spend level, most competitor cards offer just 3.33% cashback or less.

| |

|

|

Maybank Family & Friends Card is an excellent choice if you split your time–and budget–between Singapore & Malaysia. Cardholders earn 8% rebate in both countries on 5 key categories (groceries, fast food & food delivery, transport & more) with just S$800 monthly spend which makes it easy for low spenders to earn at high rates. At this spend level, most competitor cards offer just 3.33% cashback or less.

|

Maybank FC Barcelona Visa Signature: Unlimited Local Rewards

| |

If you’re a high spender with a mostly local budget, you should definitely consider Maybank FC Barcelona Visa Signature Card. Cardholders earn the highest unlimited cashback rate on the market for local spend, at 1.6% (vs. 1–1.5%). This is perfect if you typically feel constrained by earnings caps (for example, if you spend S$7,000+/month). However, this card is less effective for people with high overseas spend, as cardholders earn just 0.8 miles per S$1 on foreign currency transactions.

| |

|

|

If you’re a high spender with a mostly local budget, you should definitely consider Maybank FC Barcelona Visa Signature Card. Cardholders earn the highest unlimited cashback rate on the market for local spend, at 1.6% (vs. 1–1.5%). This is perfect if you typically feel constrained by earnings caps (for example, if you spend S$7,000+/month). However, this card is less effective for people with high overseas spend, as cardholders earn just 0.8 miles per S$1 on foreign currency transactions.

|

Maybank Platinum Visa: Rebates for Low Spenders

| |

Maybank Platinum Visa Card is the best rebate card on the market for low-spenders. In fact, cardholders can earn up to 3.33% flat cashback after just S$300 spend, capped at S$30/quarter. At this rate, most cashback cards just offer a base rewards rate of 0.3%. This means for the same spend, you’ll earn 10x the rewards with Maybank Platinum Visa Card.

| |

|

|

Maybank Platinum Visa Card is the best rebate card on the market for low-spenders. In fact, cardholders can earn up to 3.33% flat cashback after just S$300 spend, capped at S$30/quarter. At this rate, most cashback cards just offer a base rewards rate of 0.3%. This means for the same spend, you’ll earn 10x the rewards with Maybank Platinum Visa Card.

|

Maybank World Mastercard: Best Miles for Golfers

| |

Maybank World Mastercard is the best miles-earning card on the market for avid golfers. Cardholders receive 2 free green fees/month at 100 fairways across 19 countries. This is 3x the number of fairways offered by the closest competitor. In addition, cardholders enjoy travel perks like free travel insurance and airport lounge access.

| |

|

|

Maybank World Mastercard is the best miles-earning card on the market for avid golfers. Cardholders receive 2 free green fees/month at 100 fairways across 19 countries. This is 3x the number of fairways offered by the closest competitor. In addition, cardholders enjoy travel perks like free travel insurance and airport lounge access.

|

Maybank eVibes: Best Rebate Card for Students

| |

Maybank eVibes Card is the best rebate card on the market for students, offering a market-leading 1% cashback on all spend. In fact, this rate is 4x higher than most competitor cards’ and there are no merchant restrictions, unlike the closest alternative. Cardholders do not need to worry about minimum spend requirements and the S$5.0 quarterly service fee is waived simply with card use. This makes Maybank eVibes Card extremely easy to use and maintenance-free–perfect for students just starting out with their first credit card.

| |

|

|

Maybank eVibes Card is the best rebate card on the market for students, offering a market-leading 1% cashback on all spend. In fact, this rate is 4x higher than most competitor cards’ and there are no merchant restrictions, unlike the closest alternative. Cardholders do not need to worry about minimum spend requirements and the S$5.0 quarterly service fee is waived simply with card use. This makes Maybank eVibes Card extremely easy to use and maintenance-free–perfect for students just starting out with their first credit card.

|

Learn More About Maximising Your Rewards with Maybank

If you frequently travel, you may default to looking for a miles-earning credit card when seeking to earn rewards. This definitely makes sense for some. Miles cards typically offer boosted rates for overseas purchases (in other words, transactions made in foreign currency) as well as travel perks like airport lounge access, free travel insurance and more. In most cases, there's no minimum spend requirement and no earnings caps. However, annual fees tend to be higher and waivers are rare. Nonetheless, miles-earning cards typically provide the rewards rates and convenience that support the lifestyle of frequent travellers.

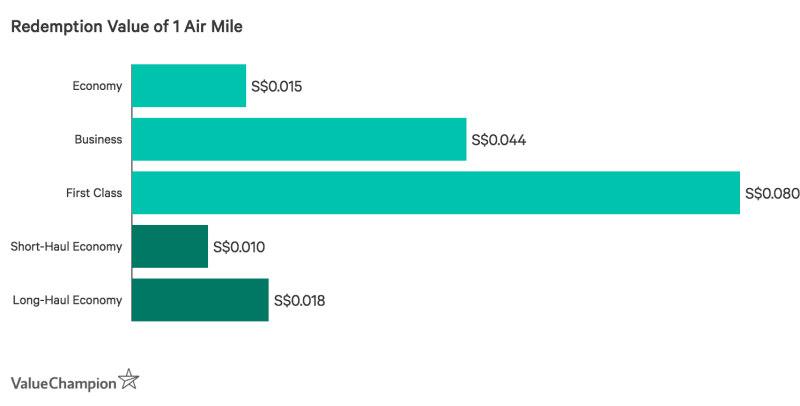

However, it's important to think about the value-to-consumer of miles rewards. If you redeem 1 mile for an economy class air ticket, its value is approximately equal to S$0.01. Given this redemption value, earning 1 mile per S$1 spend is about the same as earning 1% cashback (2 miles per S$1 is about equal to 2% cashback, and so on). Many miles-earning credit cards offer 1.2 miles per S$1 local spend and 2 miles overseas as a standard, which translates to about 1.2% and 2% cashback, respectively. These rates are notably lower than those provided by many cashback cards, which offer up to 10% rebates on select local and overseas purchases.

A miles-earning credit card often makes more sense for people who have larger budgets and are more likely to book longer flights or higher ticket classes. For example, if you redeem 1 mile for a first class ticket, its value is equal to about S$0.08. Higher spending travellers are also more likely to benefit from the lack of rewards caps, and would have an easier time meeting any spend requirements needed to unlock luxury perks. While miles cards' rates may be lower when compared to cashback alternatives, the convenience they offer may provide greater value to affluent travellers.

Overall, average spenders may actually benefit more from cashback cards, even if they tend to travel reasonably often. People who put a higher premium on travel perks and have large, overseas budgets may prefer miles-earning cards, however.

Maybank Horizon Card v. HSBC Revolution Card

| |

| HSBC Revolution Card is a great option if you’re miles-seeking, social spender that often shops online. Cardholders earn 2 miles per S$1 on local dining, entertainment and online spend–including transit and bill payments, which are typically excluded from rewards programs. Overseas and general spend, however, earn just 0.4 miles per S$1. There are no minimum spend requirements, no earnings caps, and the S$160.5 annual fee is waived with just S$12,500 annual spend.

| |

Maybank Family & Friends Card v. OCBC 365 Card

| |

| OCBC 365 Card is the best no-fee rebate card for daily essentials on the market. Cardholders earn up to 6% cashback on dining and 3% on groceries, transport, online travel & recurring bills. There’s an S$800 minimum spend requirement to access these rates, but cardholders can earn up to S$80/month, and avoid paying an annual fee with just S$10,000 annual spend. Cardholders don’t need to worry about merchant restrictions, and rates apply worldwide.

| |

Maybank FC Barcelona Card v. Standard Chartered Unlimited Cashback

| |

| Standard Chartered Unlimited Cashback Card is an excellent choice for high spenders as it offers 1.5% rebate on all spend, locally and overseas, with no cap on earnings. Cardholders also enjoy transport perks–the card is SimplyGo functional and offers up to 21% fuel savings with Caltex. There is a S$192.6 fee, waived 2 years.

| |

Maybank FC Barcelona Card v. CIMB Visa Infinite Card

| |

| CIMB Visa Infinite Card is the best unlimited cashback card for travellers. Cardholders earn 1% flat rebate on general spend and 2% on travel and overseas expenses after a S$2,000 minimum. There are no earning caps, making CIMB Visa Infinite Card perfect for high spenders. In addition, cardholders enjoy perks typically associated with miles-earning cards, like free travel insurance and 3 free lounge visits/year. Finally, CIMB Visa Infinite Card is the only unlimited card that’s free forever–no waivers involved.

| |

Maybank Platinum Visa Card v. UOB One Card

| |

| If you consistently spend S$2,000/month, you’ll earn the highest flat rebate on the market with UOB One Card. At this spend level, cardholders earn 5% cashback on all spend, up to S$300/quarter. Lower spenders earn 3.33% rebates up to S$50 or S$100/quarter, depending on their minimum spend. UOB One Card is so great because rebates apply to all transactions, including bill-pay. Cardholders are able to consolidate all their expenses onto one card, making it easy to reach the S$2,000 minimum required for the highest rebate tier. There is a S$192.6 fee, but it’s waived the 1st year.

| |

Maybank World MasterCard v. CIMB World MasterCard

| |

| CIMB World MasterCard is the best cashback card on the market for golfers. Cardholders enjoy complimentary green fees at 40 fairways across 7 countries in SE Asia. In addition, cardholders earn an unlimited 1.5% rebate, while leisure spend earns 2% (wine & dine, entertainment, recreation, automobile, and spend at duty-free stores). There’s never a fee, so high spending golfers can enjoy top perks and unlimited earning potential without worrying about extra costs.

| |

| Maybank Horizon v. HSBC Revolution |

|---|

| HSBC Revolution Card is a great option if you’re miles-seeking, social spender that often shops online. Cardholders earn 2 miles per S$1 on local dining, entertainment and online spend–including transit and bill payments, which are typically excluded from rewards programs. Overseas and general spend, however, earn just 0.4 miles per S$1. There are no minimum spend requirements, no earnings caps, and the S$160.5 annual fee is waived with just S$12,500 annual spend.

|

| Maybank Family & Friends v. OCBC 365 |

|---|

| OCBC 365 Card is the best no-fee rebate card for daily essentials on the market. Cardholders earn up to 6% cashback on dining and 3% on groceries, transport, online travel & recurring bills. There’s an S$800 minimum spend requirement to access these rates, but cardholders can earn up to S$80/month, and avoid paying an annual fee with just S$10,000 annual spend. Cardholders don’t need to worry about merchant restrictions, and rates apply worldwide.

|

| Maybank FC Barcelona v. SC Unlimited Cashback |

|---|

| Standard Chartered Unlimited Cashback Card is an excellent choice for high spenders as it offers 1.5% rebate on all spend, locally and overseas, with no cap on earnings. Cardholders also enjoy transport perks–the card is SimplyGo functional and offers up to 21% fuel savings with Caltex. There is a S$192.6 fee, waived 2 years.

|

| Maybank FC Barcelona v. CIMB Visa Infinite |

|---|

| CIMB Visa Infinite Card is the best unlimited cashback card for travellers. Cardholders earn 1% flat rebate on general spend and 2% on travel and overseas expenses after a S$2,000 minimum. There are no earning caps, making CIMB Visa Infinite Card perfect for high spenders. In addition, cardholders enjoy perks typically associated with miles-earning cards, like free travel insurance and 3 free lounge visits/year. Finally, CIMB Visa Infinite Card is the only unlimited card that’s free forever–no waivers involved.

|

| Maybank Platinum Visa v. UOB One |

|---|

| If you consistently spend S$2,000/month, you’ll earn the highest flat rebate on the market with UOB One Card. At this spend level, cardholders earn 5% cashback on all spend, up to S$300/quarter. Lower spenders earn 3.33% rebates up to S$50 or S$100/quarter, depending on their minimum spend. UOB One Card is so great because rebates apply to all transactions, including bill-pay. Cardholders are able to consolidate all their expenses onto one card, making it easy to reach the S$2,000 minimum required for the highest rebate tier. There is a S$192.6 fee, but it’s waived the 1st year.

|

| Maybank World v. CIMB World |

|---|

| CIMB World MasterCard is the best cashback card on the market for golfers. Cardholders enjoy complimentary green fees at 40 fairways across 7 countries in SE Asia. In addition, cardholders earn an unlimited 1.5% rebate, while leisure spend earns 2% (wine & dine, entertainment, recreation, automobile, and spend at duty-free stores). There’s never a fee, so high spending golfers can enjoy top perks and unlimited earning potential without worrying about extra costs. Ultimately, CIMB World MasterCard is an exceptional option for affluent golfers seeking cashback. Those who prefer earning miles and who want broader access to fairways worldwide may prefer Maybank World MasterCard. |

If you're also interested in opening a savings account, pairing a Maybank credit card with the Maybank SaveUp Savings Account can help to boost your interest rate to up to 3.00% p.a.–far above the market average in Singapore. Account holders earn a base rate according to the size of their deposit, and can boost this rate by engaging with Maybank products (loans, insurance, investment, credit cards, and more). Salary crediting also counts as a qualifying "product," making it even easier to build towards a higher rate.

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.