Best Renovation Loans in Singapore 2024

To help you find the best renovation loan your home improvement project, our analysts reviewed and analysed the best loans from all of Singapore's top lenders. Below, we highlight the most affordable loans based on your preference of loan amount and tenure.

- Best Renovation Loan Promotion: Maybank Renovation Loan

- Best Large & Long-Term Renovation Loans: DBS Renovation Loan

- Best Personal Loans for Home Renovations

- Renovation Loan From Your Mortgage Lender

- Summary of the Best Renovation Loans in 2024

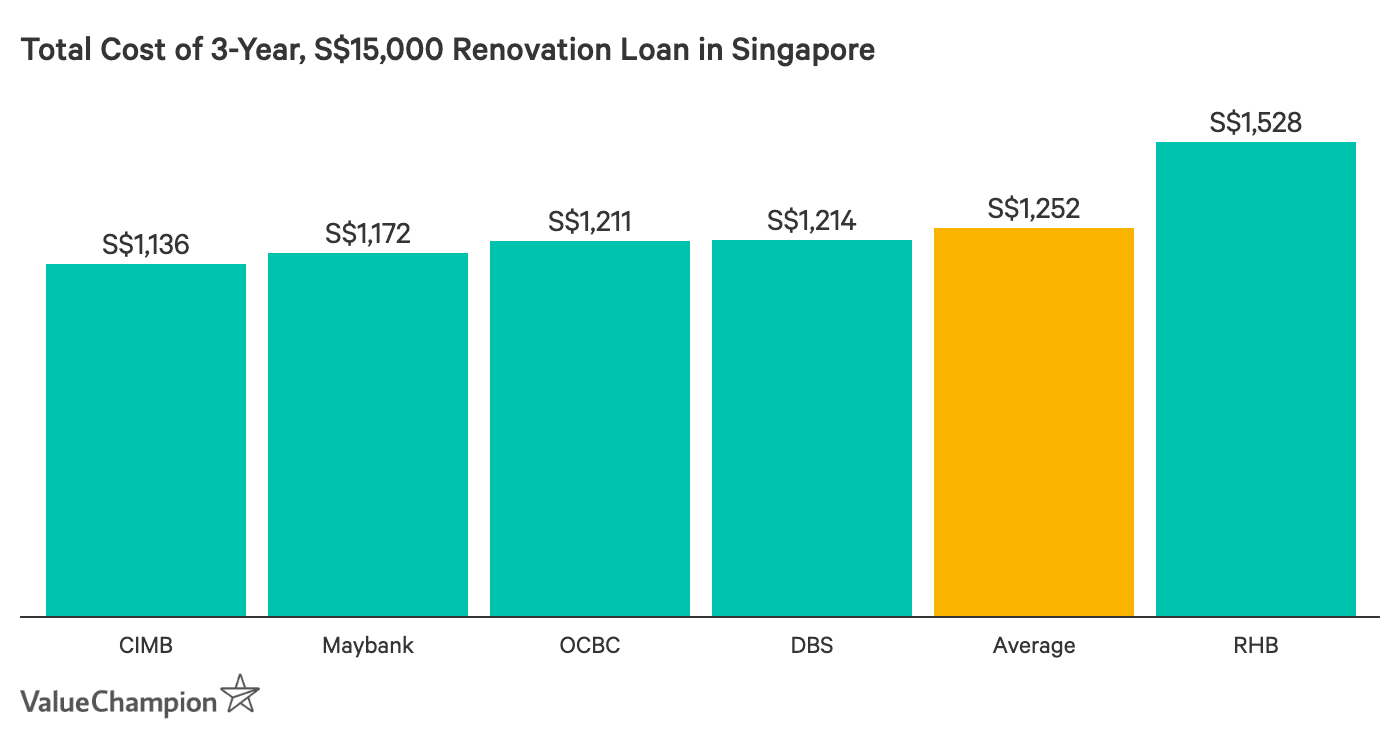

Cost Comparison of Renovation Loans by Bank

There are many renovation loans available in Singapore. Below, we compare the cost of these loans. We assume that a borrower takes out a renovation loan of S$15,000 over 5 years, and that they do not qualify for preferential rates for returning customers (i.e. they do not already have home loans from a certain bank).

- Best Renovation Loan Promotion: Maybank Renovation Loan

- Best Large & Long-Term Renovation Loans: DBS Renovation Loan

- Best Personal Loans for Home Renovations

- Renovation Loan From Your Mortgage Lender

- Summary of the Best Renovation Loans in 2024

Cost Comparison of Renovation Loans by Bank

There are many renovation loans available in Singapore. Below, we compare the cost of these loans. We assume that a borrower takes out a renovation loan of S$15,000 over 5 years, and that they do not qualify for preferential rates for returning customers (i.e. they do not already have home loans from a certain bank).

Best Renovation Loan Promotion: Maybank Renovation Loan

Maybank's competitive interest rates make it a good option for those that seek a larger renovation loan. First, Maybank's interest rate of 6.53% (Reno Loan Board rate less 4.32% p.a.) for new customers (Min 3 years tenure) is among the lowest available for loans of 4-5 years, making it a good fit for larger loans. The bank also offers dramatically lower rates if you already have a home loan with Maybank. For existing home loan customers, Maybank will reduce the interest rates between to 3.88%, which is the lowest in the market.

| Maturity | Processing Fee | Interest Rate (Rest Rate) | Monthly Instalment | Interest Cost |

|---|---|---|---|---|

| 1 Year | 1.25% | 6.93% | S$1,294.65 | S$535.84 |

| 2 Years | 1.25% | 6.93% | S$668.40 | S$1,041.53 |

| 3 Years | 1.25% | 6.53% | S$458.94 | S$1,557.84 |

| 4 Years | 1.25% | 6.53% | S$355.93 | S$2,084.73 |

| 5 Years | 1.25% | 6.53% | S$293.70 | S$2,622.18 |

| *Assuming loan of S$15,000 | ||||

Best Large, Long-Term Renovation Loans: DBS Renovation Loan

DBS offers some of the most affordable renovation loans for longer-tenures, due to its low interest rate of 4.88% p.a. This makes it worth considering for those that will require a larger renovation loan or would prefer to spread out the total cost of their loan over a longer period of time. With that said, DBS charges higher than average fees (1% handling fee + 1% insurance premium) and does not offer the best short-term rates. Therefore, those who need a smaller renovation loan would be better off choosing a different lender.

| Maturity | Processing Fee | Interest Rate (Rest Rate) | Monthly Instalment | Total Cost |

|---|---|---|---|---|

| 1 Year | 2% | 4.88% | S$1,283.29 | S$399.45 |

| 2 Years | 2% | 4.88% | S$657.27 | S$774.36 |

| 3 Years | 2% | 4.88% | S$448.76 | S$1,155.20 |

| 4 Years | 2% | 4.88% | S$344.62 | S$1,541.98 |

| 5 Years | 2% | 4.88% | S$282.24 | S$1,934.67 |

| *Assuming loan of S$15,000 | ||||

Best Renovation Loans With Low Fees: CIMB Renovation-i Financing Loan

CIMB Renovation-i Financing renovation loan offers some of the best rates for long-term renovation loans or projects more than S$25,000. Also, Renovation-i Financing offers some of the lowest effective interest rates and boasts a quick 1-day turnaround for homeowners looking for immediate funds. The bank also has lower introductory fees as it charges a processing fee of 1.2% and no administrative fee. Borrowers are also able to choose flexible tenures for up to 5 years that cover all types of residential properties, completed or still under construction.

| Maturity | Processing Fee | Interest Rate (Rest Rate) | Monthly Instalment | |

|---|---|---|---|---|

| 1 Year | 1.2% | 4.48% (CPR-1.02%) | S$2,135 | |

| 2 Years | 1.2% | 4.48% (CPR-1.02%) | S$1,091 | |

| 3 Years | 1.2% | 4.48% (CPR-1.02%) | S$744 | |

| 4 Years | 1.2% | 4.35% (CPR-1.02%) | S$569 | |

| 5 Years | 1.2% | 4.35% (CPR-1.02%) | S$465 | |

| *Assuming loan of S$25,000 | ||||

Best Personal Loans for Renovation Projects

For those seeking to completely remodel their home, a renovation loan of S$30,000 may not be enough to cover the full cost of a renovation. For these individuals, it would be prudent to consider a personal loan. However, individuals seeking a loan of S$30,000 or less will save money with renovation loans, which typically charge lower interest rates compared to personal loans.

Best Personal Loan for Home Renovations: HSBC Personal Loan

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 4x monthly salary for income S$30,000 to S$120,000; 8x monthly salary for income > S$120,000; S$200,000 Maximum Loan Size (2x monthly salary for foreigners)

- Min. Loan Amount

- S$10,000

- Processing Fee

- S$0

- Approval Time

- 1 minute approval, receive cash in one business day

| Loan Duration | Flat Rate | Processing Fee | Effective Interest Rate | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 4% | 0% | 7.5% | S$866.67 | S$400 |

| 2 years | 4% | 0% | 7.5% | S$450.00 | S$800 |

| 3 years | 4% | 0% | 7.5% | S$311.11 | S$1,200 |

| 4 years | 4% | 0% | 7.5% | S$241.67 | S$1,600 |

| 5 years | 4% | 0% | 7.5% | S$200.00 | S$2,000 |

| 6 years | 4% | 0% | 7.5% | S$172.22 | S$2,400 |

| 7 years | 4% | 0% | 7.5% | S$152.38 | S$2,800 |

| *Assuming S$10,000 loan and income of S$30,000 | |||||

HSBC's offers the most affordable personal loans for most consumers. For instance, the bank's effective interest rate of 7.5% p.a. is the best available. Additionally, the bank tends to offer competitive promotions. The bank is also ideal for those that need a large loan for their renovation project because it is the only bank to offer 7-year loans. This assists homeowners that prefer to spread out the total cost of their loan over several years. Finally, HSBC is a great option for expats and other foreigners residing in Singapore, as its income requirement for these consumers is lower than those of other banks (S$40,000).

- Current Promotions:

- New BAU Promo: S$100 Cashback

- Read Our Full Review

Instant Cash Disbursement: POSB/DBS Personal Loans

- Eligibility

- S$20,000 of annual income

- Max. Loan Amount

- 4x monthly salary; 10x monthly salary for income > S$120,000

- Min. Loan Amount

- S$500

- Processing Fee

- 1% of loan principal

- Approval Time

- Immediate approval & disbursement for DBS & POSB credit card or line of credit customers

| Loan Duration | Flat Rate | Fee | Effective Interest Rate | Monthly Payment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 3.88% | 1% | 7.56% | S$865.67 | S$388 |

| 2 years | 3.88% | 1% | 7.56% | S$449.00 | S$776 |

| 3 years | 3.88% | 1% | 7.56% | S$310.11 | S$1,164 |

| 4 years | 3.88% | 1% | 7.56% | S$240.67 | S$1,552 |

| 5 years | 3.88% | 1% | 7.56% | S$199.00 | S$1,940 |

| *Assuming loan of S$10,000 | |||||

POSB and DBS offer instant cash disbursement to approved online applicants for their personal loans. Additionally, the banks' offer rates from 3.88% (EIR 7.56%), which are very competitive. Therefore, if you require quick financing to get your renovation started, it is worth considering POSB or DBS.

Note: The interest rate and processing fee offered to you is based on your personal credit and income profile. It may differ from the published rate and the rate offered to other borrowers.

- Current Promotions:

- New loan customers receive up to 2% cashback for approved loans of S$10,000 and above. Promotion ends 31 March 2023

- Read Our Full Review

Best Moneylender Renovation Loan for Bad Credit: Friday Finance

- Eligibility

- No min. salary; Must be SG citizen or PR who is either a Salaried Employee, Variable/Commission-based Employee or Self Employed

- Max. Loan Amount

- 6x monthly salary

- Processing Fee

- Starting from 2%; 50% refund if loan is paid off on time

- Approval Time

- 1 day

| Tenure | Interest Rate | Admin Fee | Monthly Repayment Amount | Total Cost |

|---|---|---|---|---|

| 3 Months | 2% | S$600 | S$5,201.32 | S$603.96 |

| 6 Months | 2% | S$600 | S$2,677.89 | S$1,067.34 |

| 9 Months | 2% | S$600 | S$1,837.73 | S$1,539.57 |

| 12 Months | 2% | S$600 | S$1,418.39 | S$2,020.68 |

| 18 Months | 2% | S$600 | S$1,000.53 | S$3,009.54 |

| *Assuming loan of S$15,000 | ||||

Friday Finance is a moneylender that provides personal loans that you can use for renovations, even if you have bad credit or low income. These loans are a good option for people who want to take out a short-term loan, as the max tenure is 18 months. Customers will pay between 1-3% in interest per month, depending on their specific circumstances. However, banks typically charge 3-6% annually, so they would be a better option for long-term renovation loans.

Customers who earn more than S$20,000 a year can take a loan out of up to 6x their monthly income, otherwise you have a loan cap of S$3,000. These renovation loans can be either secured or unsecured, with the latter being covered by their insurance policy at no cost to you. This means that your loan obligation will be reduced if you cannot pay back the loan due to an accident that resulted in your permanent/temporary disability or death. Furthermore, if you repay your loan on time, Friday Finance will refund you 50% of the administration fee.

Renovation Loan From Your Mortgage Lender

If you already have taken out a home loan from a bank, we recommend getting your renovation loan from the same bank. This is because banks provide lower interest rates to those who get both a home loan and a renovation loan from the same bank. Doing so can also benefit you by reducing the complexity of managing multiple bills from different parties every month. Banks typically offer 25-50% cheaper rates to these customers. For instance, Maybank's interest rate declines from 6.53% to 3.88% for their home loan customers. For most loans, this translates to savings of hundreds of dollars. Please see the below table for a detailed analysis.

| Total Cost by Maturity for Maybank Renovation (S$15,000) | New Customers | Home Loan Customers | Difference In Cost |

|---|---|---|---|

| 1 Year | S$535.84 | S$317.12 | S$218.72 |

| 2 Years | S$1,041.53 | S$613.75 | S$427.78 |

| 3 Years | S$1,557.84 | S$914.14 | S$643,70 |

| 4 Years | S$2,084.73 | S$1,218.29 | S$866.44 |

| 5 Years | S$2,622.18 | S$1,526.18 | S$1,096 |

Summary of Best Renovation Loans in 2024

When shopping for a renovation loan, the primary factor you should consider is the overall cost of the loan. This includes both the processing fee and the interest expense. Above, we have compiled all the renovation loan offerings from major lenders in Singapore by cost. To calculate the total cost, we assume a loan of S$15,000 over 5 years for a borrower that makes at least S$30,000 of annual income. Given that home renovations cost S$55,000 on average, this loan would cover about 25% of the total cost of your home remodeling.

| Renovation Loan | Fee | Interest (Rest Rate) | Monthly Payment | Total Cost |

|---|---|---|---|---|

| Maybank Renovation Loan | 1.25% | 6.53% | S$293.70 | S$2,622.18 |

| DBS/POSB Renovation Loan | 2.0% | 4.88% | S$282.24 | S$1,934,67 |

| OCBC Renovation Loan | 1.5% | 4.18% | S$277.46 | S$1,648.08 |

| CIMB Renovation Loan | 1.2% | 4.35% | S$278.62 | S$1,717.00 |

Home Renovation Loan Frequently Asked Questions

Do you have questions about home renovation loans? We have the answers.

On average, home renovation loans in Singapore charge about 5.33% in interest. This does not include the one-time upfront processing fee of .75%-2%, for a total cost of about 6-7%.

Read this article to find out what exactly goes into the average cost of a home renovation.

A few factors to look for when choosing the best home renovation loan is:

- Best interest rates

- Low processing fees

- Industry standard additional fees (e.g. early repayment, late repayment or cancellation fees)

- Loan tenor

- Ongoing promotions

Ideally, you would have enough savings to front the cost of your home renovation. The average cost of a home renovation can range from 6-7%. That being said, there are many scenarios where renovation loans are a necessary option. One example is for those moving into a new house on short notice, but don't have the savings to cover the renovation costs.

One of the biggest differences between home renovation loans and personal loans is the flexibility of use. A personal loan can be used on any purchase[s], whereas a home renovation loan can only be used for a home renovation. Additionally, the amount one can borrow in Singapore can be quiet different. The loan amount for most renovation loans are up to S$30,000, where a personal loan can be upwards of S$250,000.

Read More:

Stephen Lee is a Senior Research Analyst at ValueChampion, specializing in insurance. He holds a Bachelor of Arts degree in International Studies from the University of Washington, and his prior work experience include risk management and underwriting for professional liability and specialty insurance at Victor Insurance. Additionally, Stephen is a former US Peace Corps Volunteer in Myanmar (serving between 2018-2020), where he continues to provide business development consulting services to HR companies in Asia Pacific.