The Basics of Refinancing Your Mortgage Loan

Singapore has some of the highest real estate prices in the world. As a result, most consumers use home loans to help make the purchase of a home possible. When it comes to a home loan, the real “cost” of the loan is the interest rate. What we also know is that interest rates are at historic lows, regardless of your credit score. If you took out a loan five, ten or fifteen years ago, it is likely that the interest rate on this loan is higher than what the market is currently offering. How can you capture these low rates if you are currently paying 1.50%, 2.00% or even 3.00%? The answer is quite simple: consider refinancing your home loan.

Refinancing – The Basics

At its core, refinancing is a financial strategy where consumers pay off existing high-interest debt using a new, lower interest debt. To see how this works, consider the following example.

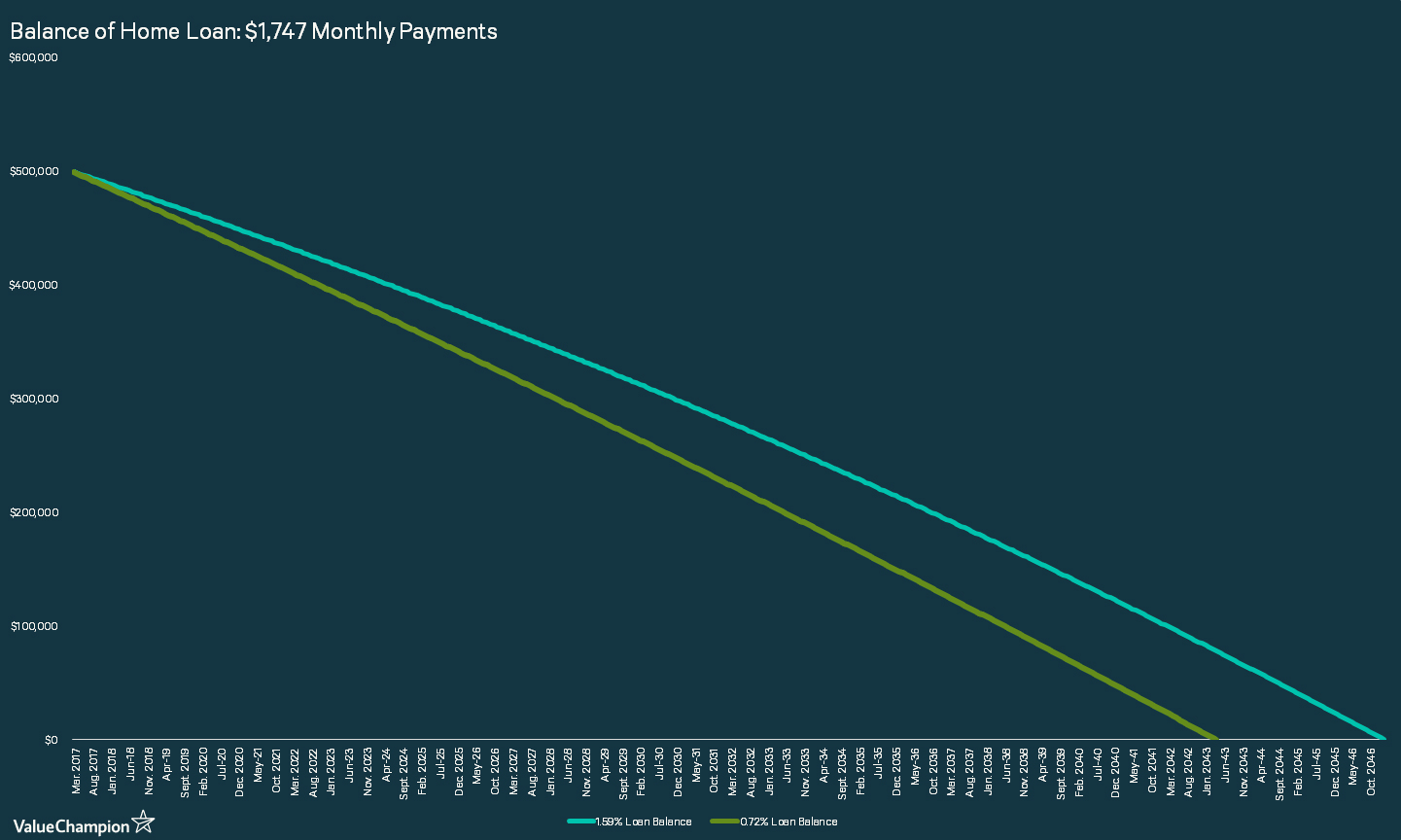

Let’s take the case of a homeowner who currently has a S$500,000 loan at 1.59% interest for the next 30 years. Each month he makes a S$1,747 payment to the bank. After a diligent search, the homeowner finds a bank which will allow them to refinance this loan at just 0.72% interest. Below graph illustrates just how much benefit you could receive by refinancing your loan. Even if you make the same amount of monthly payment, at this much lower interest rate, you will be able to pay off their loan four years faster!

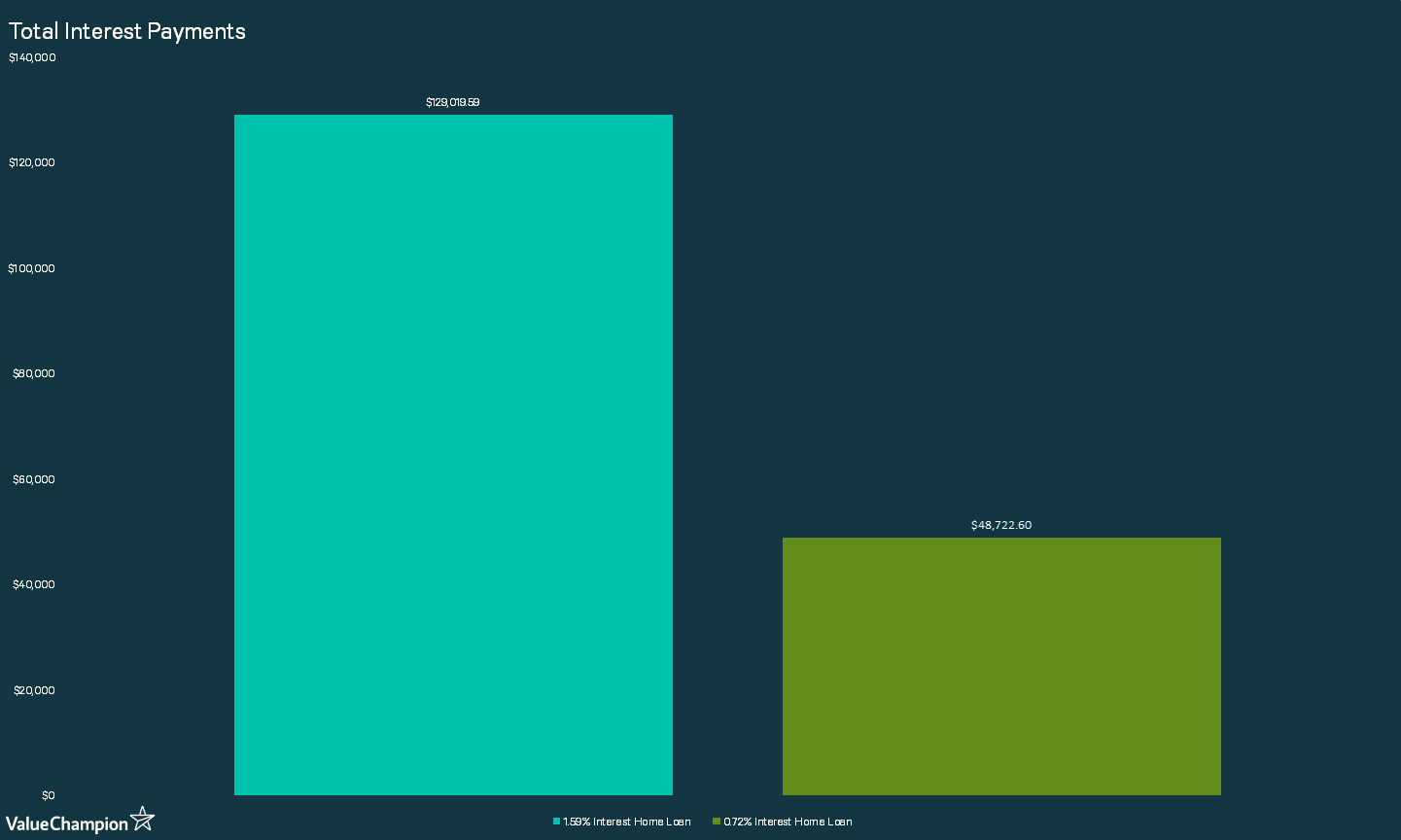

While the time saved is a good reason to look at refinancing, the real value comes from the reduced interest paid over the life of the loan. In our previous example, we assumed that the homeowner continued to pay S$1,747 monthly – even though their new loan agreement only required monthly payments of S$1,545. Many homeowners will opt to make these lower minimum monthly payments and hold the loan for 30 years rather than paying off the loan early (as we showed in the previous example). The chart below shows total interest payments made under each scenario. A 1.59%, 30-year loan, will cost S$129,020 in total interest payments. This compares to just S$48,723 on a 0.72% home loan over 30 years.

By refinancing, you can pay down debt obligations faster and spend significantly less on interest over the life of the loan.

We’ve done a lot of research on home loans in Singapore, and have found that the average interest rate on a home loan (fixed rate, 30-year) is approximately around 1.38%. For home buyers with excellent credit scores, interest rates on these 30-year loans can be as lower. This is remarkably similar to the hypothetical scenario we described above, and there's a lot of savings you can gain before interest rates pick up even more than they have.

What to Consider Before Refinancing

So refinancing looks like a great option if you can find a lender who will provide you a lower interest rate. There are a couple of things you should consider before diving in head first.

Fees From Refinancing

The majority of lenders will require you to pay a fee for refinancing your loan, like legal fees & valuation fees. These fees can easily total up to a sum greater than S$3,000. Make certain that you understand ALL of the fees involved in a refinance, as lenders have been known to hide costs within the fine print. Read the new loan agreement carefully, and ask questions, before signing on the dotted line. Some banks will even provide waivers for certain fees so that you can maximise savings from refinancing your home loan.

The Break-even Point

Once you know the fees associated with refinancing, you can develop an understanding of your break-even point. Just as we explored with cell phone insurance, this break-even point is an important concept in consumer finance. The break-even point on any financial transaction is the point where the benefits of a transaction equal the costs. In the case of a home loan refinance, this is the point where you have saved more money from refinancing than you paid in upfront fees in the process.

Let’s assume that the bank issuing the new loan at 0.72% charged the homeowner S$2,000 in refinancing fees. As the homeowner is saving S$202 per month on payments, it would take ten months to break-even on this transaction.

The math looks like this:

Break-even Point = Upfront Costs / Monthly Savings

9.9 months = S$2,000 / S$202

Once the homeowner hits the break-even point, they are saving $202 each month towards their home loan costs. In this case, refinancing is a very good idea – as the break-even point is less than a year out. In some cases, even if your break-even point is five or ten years away it can be a wise decision.

Final Thoughts

With all of this information in mind, you are now ready to begin searching for a lower interest rate on your home loan. Keep checking ValueChampion for updates on home loan rates in Singapore, the overall lending environment, and tips for making your dollars go farther.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.