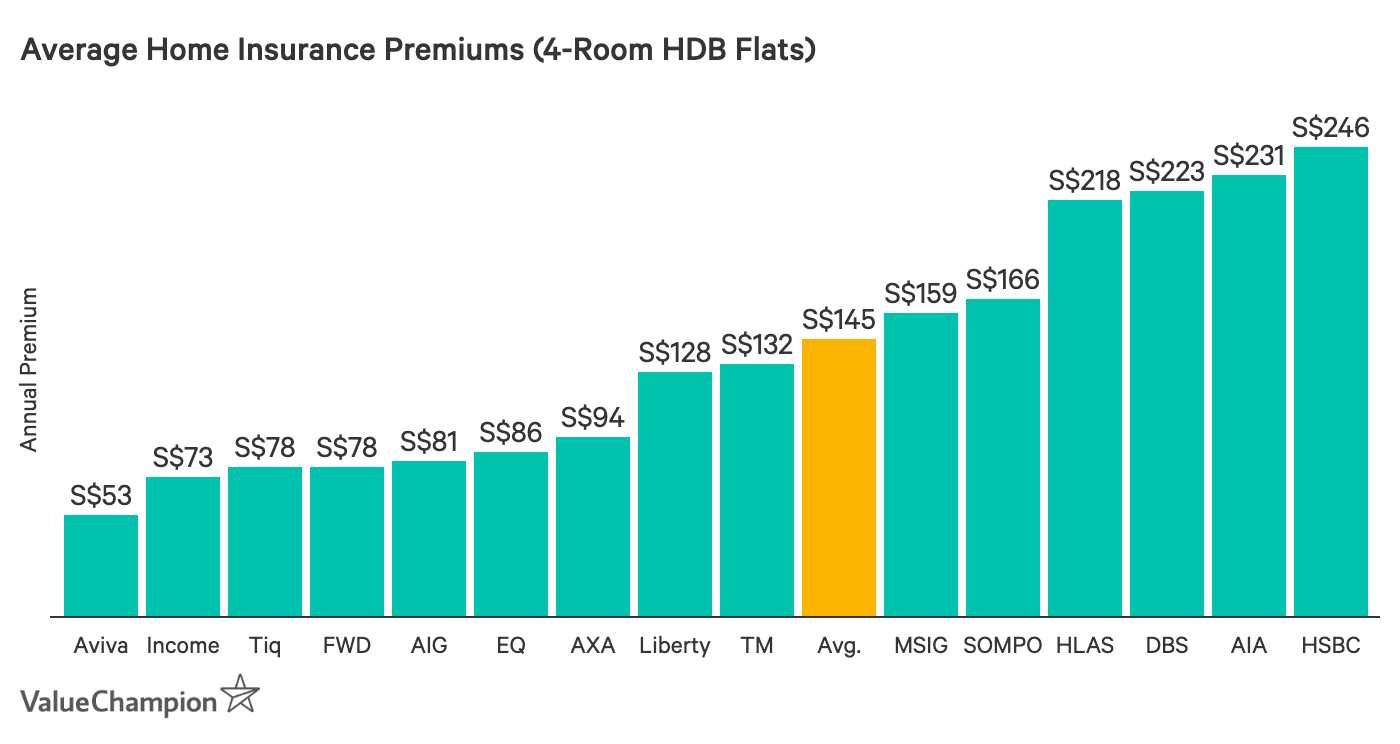

Is Emergency Home Assistance Service Actually Useful?

An increasing number of insurance companies in Singapore is beginning to offer a service called "24-Hour Emergency Home Assistance." Essentially, this service ensures that the insurance company secures and pays for certain emergency home repairs like plumbing, electricity, locksmith and pest control issues. But are they really useful service that you should get? Whether this service is valuable depends largely on three factors: how often these emergencies occur, how expensive they are to resolve and how expensive the emergency service itself is to purchase. Here, we examine some facts and opine on the value of this service based on facts.

How often do these events occur?

There aren't great statistics on how often pests or plumbing problems occur for a regular household in Singapore. Not only that, the likelihood of someone's experiencing a pest, pipe leakage or locked doors also depends heavily on the person's personal habits and living conditions. Organised and neat people living in new residences are very unlikely to find bed bugs or roaches in their apartments; in contrast, people who keep dirty dishes piled up in their sinks could find pests to be a problem occasionally, especially if they live in old buildings. All things considered, however, it's quite unlikely that you will encounter these problems often in any given year. But, it would not be surprising for anyone to experience one of these at least once or twice in their lifetime. After all, pipes get old and clogged over time, while rats and roaches will find a way to enter your buildings eventually.

How expensive are these emergency repairs?

Fortunately, most of these problems aren't that expensive to resolve. For instance, we found few websites listing prices for different plumbing services, which ranged from S$60 to S$500. Pest controls are supposed to cost around S$30-S$40 per month, while unlocking your doors can costs little as S$40 to S$50. While these are all relatively affordable, there is another cost to experiencing any of these home emergencies. Mainly, we're talking about psychological, temporal and health risks. For example, finding bed-bugs or rats in your apartment can really ruin your day unless it's fixed immediately. Not being able to use your bathroom or air conditioner because of some plumbing or electricity problem can also degrade your life quickly.

Is emergency home assistance a necessary service to have in your home insurance?

If pest, plumbing, locksmith and electricity issues at home are both infrequent and inexpensive to fix, is a 24-hour emergency home assistance service a necessity? If such a service were an expensive add-on to your home insurance policy, one should certainly think twice before paying up for it. We wouldn't recommend doing that ourselves. However, what if this were a free service for purchasing a policy that's already cheaper than others?

| Insurance Companies Offering 24-hr Emergency Home Assistance | Coverage Details |

|---|---|

| Etiqa | S$200 per service x 4 times a year |

| AXA | S$300 per service x 1 time a year |

| SOMPO | S$100 per event |

| Liberty | $100 per occurence x 2 times a year |

This is why Etiqa's announcement of its new Emergency Home Assistance service is interesting. Our study of major home insurance plans in Singapore found that Etiqa's 5-year home insurance plan stands out as being one of the cheapest options as well as offering the most competitive emergency home service in the country. This means that you can get this 24-hour emergency home assistance pretty much as a free add-on service, while ensuring that you can get a convenient assistance night and day in case your pipe leaks, a/c breaks or you are locked out of your home, and get your insurer to pay for a large chunk (if not the whole) of your bill.

Of course, there's always a catch. First, Etiqa only provides this level of price and service for customers who buy their 5-year long home insurance policies. Buying their 1-year policies will cost you more and lose access to their home emergency coverage. Secondly, you have no way of avoiding the contractor's overcharging you, since the insurer will be sending one on their own. However, this second factor is almost always a concern for any contract workers unless you take your time to research and negotiate, a luxury most people can't afford in case of an emergency. Also, you can take solace in knowing a meaningful portion of your bill will be paid or reimbursed by your insurance company. In fact, this dynamic could incentivise the insurance company keep the contractors honest, since any service below S$200 will be paid entirely by the insurer; just like you, they also want to minimise their cost.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.