4 Money-Losing Myths About Home Loans in Singapore

Vast majority of people in Singapore end up owning a home one way or another, with the country's homeownership hovering around 90%. However, there are also a proportional number of myths surrounding the issue of home ownership, and therefore home loans, that still confuse and cause real economic losses for people. To debunk some of these myths that actually cost you real dollars, we reveal some truths about some of the most popular mortgage myths.

Myth 1: Fixed-rate mortgages are always the best.

When thinking of a traditional home loan, most people bring up a 25-30 year fixed-rate mortgage. While these home loans are a common and popular option, they aren’t always the best choice for everyone. In fact, whether you should get a fixed or floating rate home loan matter chiefly on how rates are expected to change over the next 3 years.

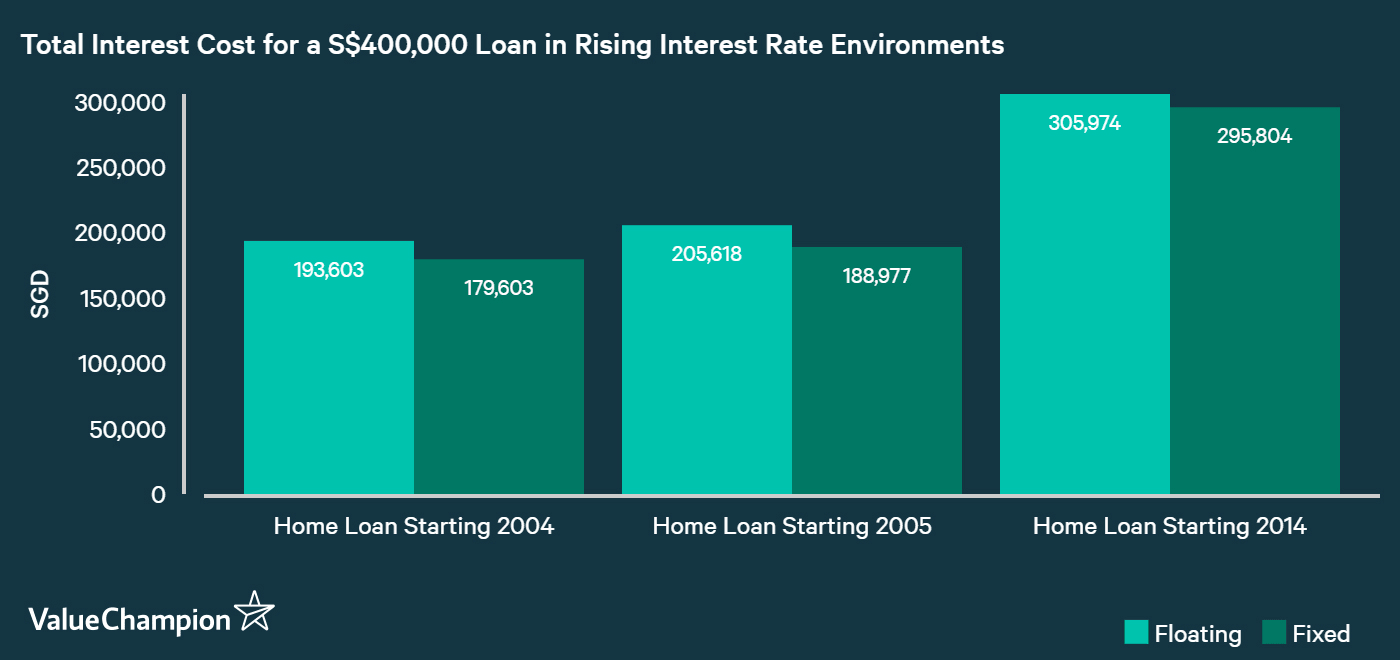

Fixed-rate home loans in Singapore hold their interest rates constant for up to 3 years only. This means that the interest cost between a fixed rate and a floating rate is largely dependent on how rates change over the 3 years during which your interest is fixed. Therefore, fixed rates are only good when rates are set to rise meaningfully. Otherwise, floating rates can be a much more economic option. For instance, consider our example below where we calculate the interest cost of S$400,000 worth of home loans that begin in 2004, 2005 and 2014, all when rates rose for the next 3 years. Fixed rate loans ended up costing about S$10,000 less than floating rate loans.

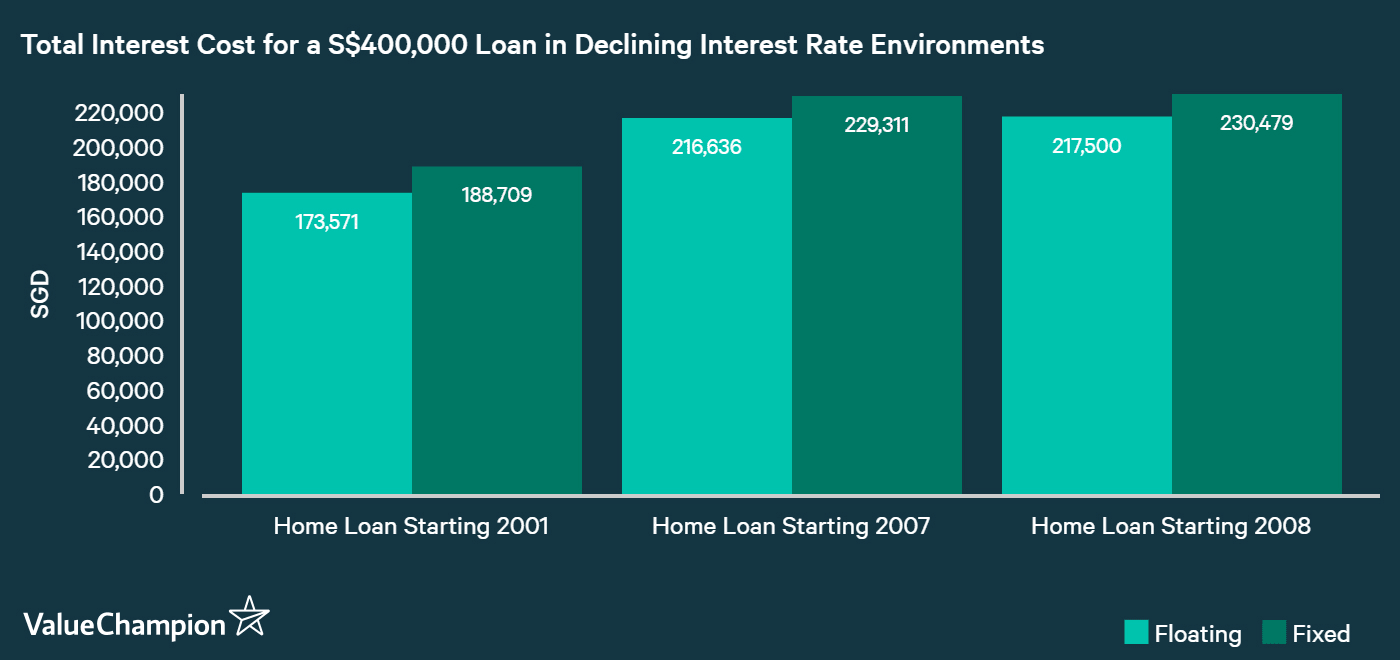

People perceive floating rate mortgages with some stigma and concerns because their interest rates can fluctuate. However, most people also fail to consider that these loans also tend to charge lower rates than fixed rate loans because of this volatility. Therefore, they tend to be the more economic choice in a stable-rate environment. Not only that, they also help you save money when rates end up declining, as they did in 2008 and 2009. At the end of the day, you can always refinance your loan after 3 years if your expectations on rate movements change and fixed rates become more economical. If you are trying to decide which one is a better option right now, you can compare the best home loan rates for yourself using our tool at the link.

Myth 2: It's cheaper to rent than to own a home.

Another myth about homeownership is that it's more expensive than renting an apartment. This myth cannot be farther from the truth. In fact, as long as you have saved enough for a downpayment, owning will cost you far less in terms of monthly payments than renting. According to our analysis of HDB's 2013-2017 data on median rent and resale prices, owning can be 15-50% cheaper than renting a comparable property in terms of monthly payments. In addition to HDB flats, private properties showed similar results: you pay less on a home mortgage every month than you would for rent. This doesn't even account for the fact that owning a home helps you build equity and wealth over time, while renting is simply an expenditure that adds up to nothing.

There are a couple reasons why this is the case. When you rent, your landlord adds a margin in order to make a profit from you. This especially the case because the real estate market in Singapore has not been all that hot: besides rental income, there aren't other sources of profit on real estate. They also provide you with the convenience of avoiding a big down payment and taking care of the maintenance issues.

Myth 3: You should always pay off your mortgage as quickly as possible.

Most people don't like to be in debt. Therefore, there's a natural inclination to pay off one's loan as quickly as possible. When it comes to home loans, however, repaying early does not equal savings. Because banks rely on the predictability of a home loan's payment schedule, they encourage the borrowers to stick to their payment plan for as long as possible; after all, it's a great way to lock-in a profit stream for a long period of time. To do this, they introduce features like "early redemption penalty" that imposes fines on people who pay either a portion or the entirety of their home loans before their maturity.

Rather than repaying your mortgage early, it's more advisable to invest the extra cash you have on hand. While home loans can only cost you about 2%, investing properly can help you generate much higher returns of 5-10% annually if you do it well, more than offsetting the opportunity cost of using that cash to reduce your interest cost. Not only that, the interest you pay on your home loan are tax-deductible, so they aren't as expensive as you perceive them to be.

Myth 4: Once you obtain approval-in-principle, you’re guaranteed the loan amount.

Before starting your home shopping process, it's essential to get pre-approved from a lender so that you have a good idea of your budget and that you can readily snatch up a property you want. However, many people aren't aware that getting pre-approved and obtaining approval-in-principle does not guarantee that you get the amount that you want.

In contrast, a bank bases its approval-in-principle (AIP) on the credit report and financial health of the borrower. It is in no ways "binding" and therefore subject to the property valuation and other checks in the application process. Though it is typically valid for 1 to 3 months, your bank can change its "commitment" if it finds out any new material information about you or the home you are buying. Just because you were pre-approved, it doesn't mean you can stop worrying about your credit score or start getting other loans for a big purchase.

Therefore, we recommend you to do your best to maintain your credit score by keeping up with your bill payments and not getting any other loans during your home purchase process. Banks can still change its mind any time before your mortgage closes, and any additional credit obtained or damages on your credit score can work against you in your home loan application process. If this happens, you can lose a significant amount of money in booking fees that you may have already paid.

Parting Thoughts

Because most people purchase a home only once in their life time, it's easy to believe myths about home loans because they lack the expertise and experience to make the smartest decisions. However, given the sheer size and significance it carries, we should be more careful about which advice we adhere to when it comes to securing our home. Now that you know the truth about these mortgage myths, we hope that you are better equipped to start your home-buying process.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.