Best Personal Loans in Singapore 2024

Taking out a personal loan may be necessary if you need extra cash for a major expense. Our loan experts analysed and compared all of the personal loans available on the market to help you find the best personal loan for your specific needs.

| Bank | Best For: | Flat Rate | Tenor |

|---|---|---|---|

| Lendela Personal Loan | Low-Income Borrowers | from 0.8% p.m. | 1-7 years |

| HSBC Personal Loan | Best Overall | from 3.2% p.a. | 1-7 years |

| Standard Chartered CashOne | Promotions | from 3.48% p.a. | 1-5 years |

| POSB/DBS Personal Loan | Instant Cash Disbursement | from 2.88% p.a. | 1-5 years |

| Citibank Quick Cash Personal Loan | Short-Term | from 3.45% p.a. | 1-5 years |

| OCBC Cash-On-Instalment | Cash-on-Instalment | 3.5% p.a. | 1-5 years |

| Standard Chartered CashOne | Low-Income Borrowers | from 9.8% | 1-5 years |

| HSBC Personal Loan | Foreigners & Expats | from 3.7% p.a. | 1-7 years |

| Friday Finance Personal Loan | Low Credit | from 1% p.m. | 3 months - 18 months |

| TCC Personal Loan | Low-Income Borrowers | 6.99% p.a. | 1 month - 5 years |

| Bank | Best For: | Flat Rate | Tenor |

|---|---|---|---|

| Lendela Personal Loan | Low-Income Borrowers | from 0.8% p.m. | 1-7 years |

| HSBC Personal Loan | Best Overall | from 3.4% p.a. | 1-7 years |

| Standard Chartered CashOne | Promotions | from 3.48% p.a. | 1-5 years |

| POSB/DBS Personal Loan | Instant Cash Disbursement | from 2.88% p.a. | 1-5 years |

| Citibank Quick Cash Personal Loan | Short-Term | from 3.45% p.a. | 1-5 years |

| OCBC Cash-On-Instalment | Cash-on-Instalment | 3.5% p.a. | 1-5 years |

| Standard Chartered CashOne | Low-Income Borrowers | from 9.8% | 1-5 years |

| HSBC Personal Loan | Foreigners & Expats | from 3.2% p.a. | 1-7 years |

| Friday Finance Personal Loan | Low Credit | from 1% p.m. | 3 months - 18 months |

| TCC Personal Loan | Low-Income Borrowers | 6.99% p.a. | 1 month - 5 years |

Compare the Best Personal Loans in Singapore

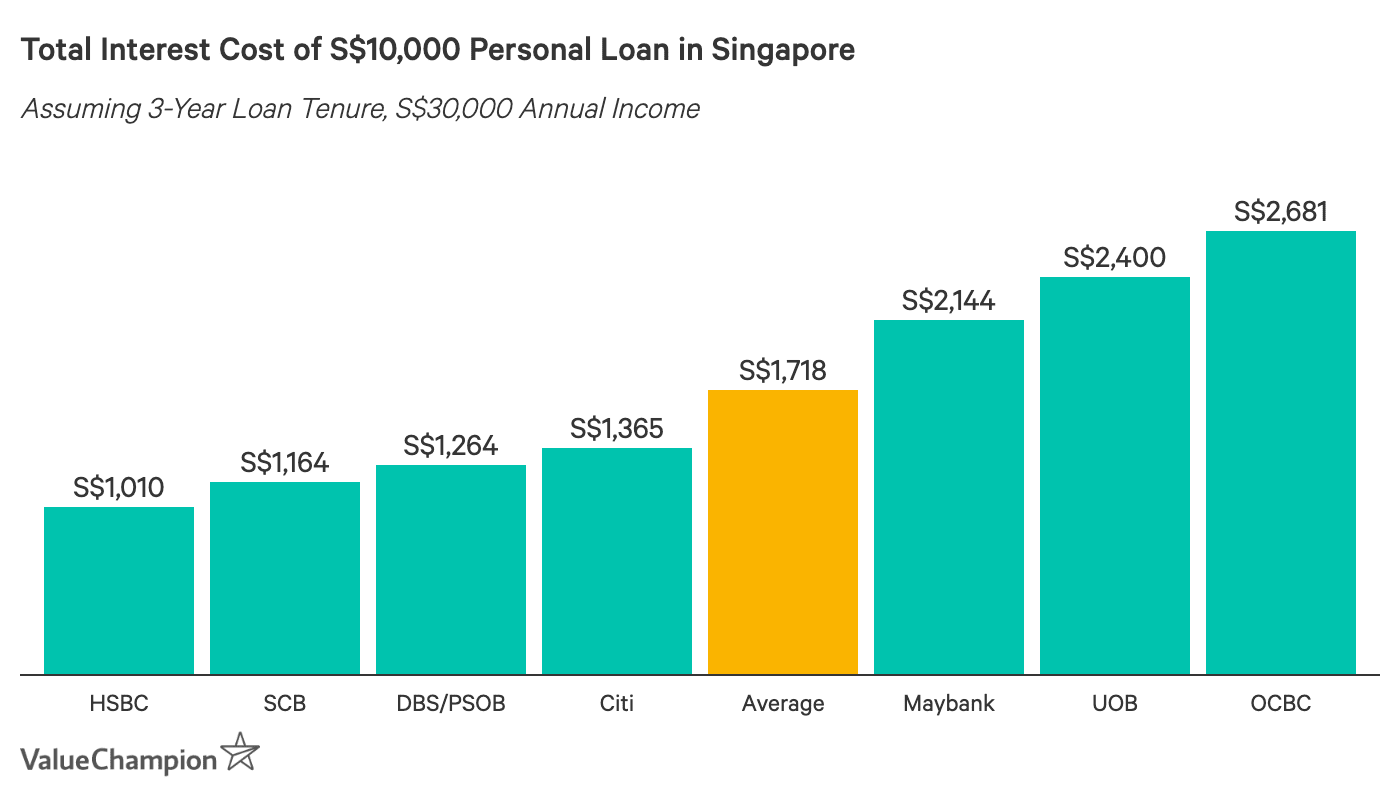

Below, we show the total cost for each personal loan in Singapore. Our chart assumes a 3-year S$10,000 loan for a borrower that makes at least S$30,000 annually. For a loan of this size, you should expect to pay somewhere between S$1,000 and S$2,500 in fees and interest. This cost does not include fees for late or early payments, which we typically advise against.

Best Moneylender Loans for Low-Income Borrowers: Lendela

- Eligibility

- S$1,200 per month

- Max. Loan Amount

- 6x monthly salary

- Min. Loan Amount

- S$1,000

- Processing Fee

- Varies

- Approval Time

- 1 day

Promotion:

|

|---|

Lendela is an online loan provider that helps borrowers find the best personal loans for their needs.

The platform tailors personal loan recommendations from various MAS regulated banks and financial institutions in Singapore, which often come with lower eligibility requirements compared to traditional bank loans. This makes Lendela a suitable alternative for those who do not qualify for a personal loan from a bank.

Note that the loans are provided by the banks and financial institutions, and not Lendela itself.

- Eligibility

- S$1,200 per month

- Max. Loan Amount

- 6x monthly salary

- Min. Loan Amount

- S$1,000

- Processing Fee

- Varies

- Approval Time

- 1 day

Promotion:

|

|---|

Lendela is a great option for individuals that do not qualify for personal loans from banks. For example, Lendela provides prospective borrowers with a comparison of the best personal loans from moneylenders based on the borrower's credit score. Additionally, Lendela has a low minimum income requirement (S$1,200 monthly) and most applicants receive more than 1 same-day loan offer. In these ways, the platform is a great alternative for those that cannot obtain bank loans.

Best Personal Loan: HSBC Personal Loan

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 4x monthly salary for income S$30,000 to S$120,000; 8x monthly salary for income > S$120,000; S$200,000 Maximum Loan Size (2x monthly salary for foreigners)

- Min. Loan Amount

- S$10,000

- Processing Fee

- S$0

- Approval Time

- 1 minute approval, receive cash in one business day

| Promotion:

|

|---|

HSBC's personal loans typically charge the lowest effective interest rates in the market (from 7.5% EIR). Additionally, HSBC is the only lender that provides 7-year personal loans in Singapore, which can reduce the burden of your monthly repayments by spreading them out over a longer period of time. HSBC also boasts a quick 1 minute in-principle approval time and you can receive cash by the next day for successful loan applications of less than S$100,000. Finally, the bank is a great option for foreigners living in Singapore, as its income requirement for foreigners (S$40,000) is the lowest of any bank in our review.

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 4% | 0% | 7.5% | S$866.67 | S$400 |

| 2 years | 4% | 0% | 7.5% | S$450.00 | S$800 |

| 3 years | 4% | 0% | 7.5% | S$311.11 | S$1,200 |

| 4 years | 4% | 0% | 7.5% | S$241.67 | S$1,600 |

| 5 years | 4% | 0% | 7.5% | S$200.00 | S$2,000 |

| 6 years | 4% | 0% | 7.5% | S$172.22 | S$2,400 |

| 7 years | 4% | 0% | 7.5% | S$152.38 | S$2,800 |

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 4x monthly salary for income S$30,000 to S$120,000; 8x monthly salary for income > S$120,000; S$200,000 Maximum Loan Size (2x monthly salary for foreigners)

- Min. Loan Amount

- S$10,000

- Processing Fee

- S$0

- Approval Time

- 1 minute approval, receive cash in one business day

| Promotion:

|

|---|

HSBC's personal loans typically charge the lowest effective interest rates in the market (from 7.5% EIR). Additionally, HSBC is the only lender that provides 7-year personal loans in Singapore, which can reduce the burden of your monthly repayments by spreading them out over a longer period of time. HSBC also boasts a quick 1 minute in-principle approval time and you can receive cash the next day for successful loan applications of less than S$100,000. Finally, the bank is a great option for foreigners living in Singapore, as its income requirement for foreigners (S$40,000) is the lowest of any bank in our review.

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 4% | 0% | 7.5% | S$866.67 | S$400 |

| 2 years | 4% | 0% | 7.5% | S$450.00 | S$800 |

| 3 years | 4% | 0% | 7.5% | S$311.11 | S$1,200 |

| 4 years | 4% | 0% | 7.5% | S$241.67 | S$1,600 |

| 5 years | 4% | 0% | 7.5% | S$200.00 | S$2,000 |

| 6 years | 4% | 0% | 7.5% | S$172.22 | S$2,400 |

| 7 years | 4% | 0% | 7.5% | S$152.38 | S$2,800 |

Best Personal Loan Promotions: Standard Chartered CashOne Personal Loan

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 2x monthly salary for annual income below S$30,000; 4x monthly salary for annual income > S$30,000; 8x monthly income for annual income above S$120,000 (up to S$250,000)

- Min. Loan Amount

- S$1,000

- Processing Fee

- S$199 for 1st year, S$50 for subsequent years (waived for borrowers who make repayments on time)

- Approval Time

- 15 minutes

| Promotion:

|

|---|

Standard Chartered is currently offering some of the best cashback promotions for personal loans in Singapore. For instance, the bank is offering up to S$2,400 cashback. On top of their competitive rates (starting at 3.48% p.a.), these promos make the CashOne personal loan a great fit for those seeking loans of at least S$15,000 with tenures of 4 to 5 years. Finally, approval takes 15 minutes, after which funds are disbursed instantly. However, it is important to keep in mind that other loans may be cheaper if you do not qualify for Standard Chartered's lowest rates and current promotions.

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year loan | 3.48% | S$199 | 6.95% | S$862.33 | S$348 |

| 2 year loan | 3.48% | S$199 | 8.45% | S$445.67 | S$696 |

| 3 year loan | 3.48% | S$199 | 7.63% | S$306.78 | S$1,044 |

| 4 year loan | 3.48% | S$199 | 7.30% | S$237.33 | $1,392 |

| 5 year loan | 3.48% | S$199 | 7.10% | S$195.67 | S$1,740 |

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 2x monthly salary for annual income below S$30,000; 4x monthly salary for annual income > S$30,000; 8x monthly income for annual income above S$120,000 (up to S$250,000)

- Min. Loan Amount

- S$1,000

- Processing Fee

- S$199 for 1st year, S$50 for subsequent years (waived for borrowers who make repayments on time)

- Approval Time

- 15 minutes

| Promotion:

|

|---|

Standard Chartered is currently offering some of the best cashback promotions for personal loans in Singapore. For instance, the bank is offering up to S$2,400 cashback. On top of their competitive rates (starting at 3.48% p.a.), these promos make the CashOne personal loan a great fit for those seeking loans of at least S$15,000 with tenures of 4 to 5 years. Finally, approval takes 15 minutes, after which funds are disbursed instantly. However, it is important to keep in mind that other loans may be cheaper if you do not qualify for Standard Chartered's lowest rates and current promotions.

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year loan | 3.48% | S$199 | 6.95% | S$862.33 | S$348 |

| 2 year loan | 3.48% | S$199 | 8.45% | S$445.67 | S$696 |

| 3 year loan | 3.48% | S$199 | 7.63% | S$306.78 | S$1,044 |

| 4 year loan | 3.48% | S$199 | 7.30% | S$237.33 | $1,392 |

| 5 year loan | 3.48% | S$199 | 7.10% | S$195.67 | S$1,740 |

Best Personal Loan for New Customers: CIMB CashLite Personal Loan

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- Unknown

- Min. Loan Amount

- S$1,000

- Processing Fee

- 0

- Approval Time

- 1 day

| Promotion:

|

|---|

CIMB personal loans offer one of the lowest promotional rates for new customers, making it an attractive option for those who want to borrow cash inexpensively. CIMB offers 1 - 5 years loans. Their current promotional rate of 3.38% interest p.a. for new customers is the lowest in the market for a loan of 3 - 5 years tenure. For its existing customers, CIMB charges a flat annual interest rate of 4.50%, which is middle-range compared to the market average.

The CIMB personal loan also has no processing fees at the time of application, but does have a late payment fee and an early termination fee should you end your contract early.

| Loan Duration | Flat Rate | Annual Fee | EIR | Monthly Installment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 4.00% | 0% | 7.30% | S$866.67 | S$400 |

| 2 years | 4.00% | 0% | 7.50% | S$450.00 | S$800 |

| 3 years | 3.38% | 0% | 6.38% | S$305.95 | S$1,014 |

| 4 years | 3.38% | 0% | 6.36% | S$236.50 | S$1,352 |

| 5 years | 3.38% | 0% | 6.32% | S$194.84 | S$1,690 |

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- Unknown

- Min. Loan Amount

- S$1,000

- Processing Fee

- 0

- Approval Time

- 1 day

| Promotion:

|

|---|

CIMB personal loans offer one of the lowest promotional rates for new customers, making it an attractive option for those who want to borrow cash inexpensively. CIMB offers 1 - 5 years loans. Their current promotional rate of 3.48% interest p.a. for new customers is the lowest in the market for a loan of 3 - 5 years tenure. For its existing customers, CIMB charges a flat annual interest rate of 4.50%, which is middle-range compared to the market average.

The CIMB personal loan also has no processing fees at the time of application, but does have a late payment fee and an early termination fee should you end your contract early.

| Loan Duration | Flat Rate | Annual Fee | EIR | Monthly Installment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 4.00% | 0% | 7.30% | S$866.67 | S$400 |

| 2 years | 4.00% | 0% | 7.50% | S$450.00 | S$800 |

| 3 years | 3.38% | 0% | 6.38% | S$305.95 | S$1,014 |

| 4 years | 3.38% | 0% | 6.36% | S$236.50 | S$1,352 |

| 5 years | 3.38% | 0% | 6.32% | S$194.84 | S$1,690 |

Fastest Personal Loan Disbursement: POSB/DBS Personal Loan

- Eligibility

- S$20,000 of annual income

- Max. Loan Amount

- 4x monthly salary; 10x monthly salary for income > S$120,000

- Min. Loan Amount

- S$500

- Processing Fee

- 1% of loan principal

- Approval Time

- Immediate approval & disbursement for DBS & POSB credit card or line of credit customers

|

Promotion:

|

|---|

POSB and DBS charge some of the most competitive interest rates (from 3.88% p.a., 7.56% EIR) for personal loans in Singapore. Not only that, the banks' loans are particularly useful for individuals that need cash immediately. While most banks take at least a day to disburse personal loans, POSB & DBS instantly provide funds to their credit card and credit line customers, as well as new customers that credit their salary into a POSB or DBS deposit account.

Note: The interest rate and processing fee offered to you is based on your personal credit and income profile. It may differ from the published rate and the rate offered to other borrowers.

| Loan Duration | Flat Rate | Fee | EIR | Monthly Payment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 3.88% | 1% | 7.56% | S$865.67 | S$388 |

| 2 years | 3.88% | 1% | 7.56% | S$449.00 | S$776 |

| 3 years | 3.88% | 1% | 7.56% | S$310.11 | S$1,164 |

| 4 years | 3.88% | 1% | 7.56% | S$240.67 | S$1,552 |

| 5 years | 3.88% | 1% | 7.56% | S$199.00 | S$1,940 |

- Eligibility

- S$20,000 of annual income

- Max. Loan Amount

- 4x monthly salary; 10x monthly salary for income > S$120,000

- Min. Loan Amount

- S$500

- Processing Fee

- 1% of loan principal

- Approval Time

- Immediate approval & disbursement for DBS & POSB credit card or line of credit customers

Promotion:

|

|---|

POSB and DBS charge some of the most competitive interest rates (from 3.88% p.a., 7.56% EIR) for personal loans in Singapore. Not only that, the banks' loans are particularly useful for individuals that need cash immediately. While most banks take at least a day to disburse personal loans, POSB & DBS instantly provide funds to their credit card and credit line customers, as well as new customers that credit their salary into a POSB or DBS deposit account.

Note: The interest rate and processing fee offered to you is based on your personal credit and income profile. It may differ from the published rate and the rate offered to other borrowers.

| Loan Duration | Flat Rate | Fee | EIR | Monthly Payment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 3.88% | 1% | 7.56% | S$865.67 | S$388 |

| 2 years | 3.88% | 1% | 7.56% | S$449.00 | S$776 |

| 3 years | 3.88% | 1% | 7.56% | S$310.11 | S$1,164 |

| 4 years | 3.88% | 1% | 7.56% | S$240.67 | S$1,552 |

| 5 years | 3.88% | 1% | 7.56% | S$199.00 | S$1,940 |

Best Small, Short-Term Personal Loan: Citibank Quick Cash Personal Loan

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 4x Monthly Income (or S$150,000)

- Min. Loan Amount

- S$1,000

- Processing Fee

- 0%

- Approval Time

- 1 hour (before 5pm)

| Promotion:

|

|---|

For people who need a small personal loan and expect to be able to pay it off within 3 years, Citibank's Quick Cash Personal Loan (formerly Ready Credit PayLite) is one of the best options in the market. Citibank's effective interest rates of 6.50% for new customers are among the lowest in Singapore for 1-3 years. Additionally, Citibank's Personal Loan does not charge a processing fee. Finally, Citibank’s minimum loan amount is only S$1,000, making it very accessible for anyone who may need to borrow just a few thousand dollars.

Additionally, Citibank's Personal Loans now offer competitive interest rates for loans with longer tenures, making even more of an attractive option for borrowers. However, while Citi's application decision is made within one hour, cash is disbursed more slowly, for new Citibank customers, (1-5 days) than other banks.

| Loan Duration | Flat Rate | Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year loan | 3.56% | 0% | 6.50% | S$863.00 | S$356.00 |

| 2 years loan | 3.46% | 0% | 6.50% | S$445.50 | S$692.00 |

| 3 years loan | 3.45% | 0% | 6.50% | S$306.53 | S$1,035.00 |

| 4 years loan | 3.46% | 0% | 6.50% | S$237.17 | S$1,384.00 |

| 5 years loan | 3.48% | 0% | 6.50% | S$195.67 | S$1,740.00 |

- Eligibility

- S$20,000 of annual income

- Max. Loan Amount

- 4x monthly salary

- Min. Loan Amount

- S$1,000

- Processing Fee

- None

- Approval Time

- 1 hour (before 5pm)

Promotion:

|

|---|

For people who need a small personal loan and expect to be able to pay it off within 3 years, Citibank's Quick Cash Personal Loan (formerly Ready Credit PayLite) is one of the best options in the market. Citibank's effective interest rates of 6.50% for new customers are among the lowest in Singapore for 1-3 years. Additionally, Citibank's Personal Loan does not charge a processing fee. Finally, Citibank’s minimum loan amount is only S$1,000, making it very accessible for anyone who may need to borrow just a few thousand dollars.

Additionally, Citibank's Personal Loans now offer some of the lowest interest rates for loans with longer tenures, making even more of an attractive option for borrowers. However, while Citi's application decision is made within one hour, cash is disbursed more slowly, for new Citibank customers, (1-5 days) than other banks.

| Loan Duration | Flat Rate | Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year loan | 3.56% | 0% | 6.50% | S$863.00 | S$356.00 |

| 2 years loan | 3.46% | 0% | 6.50% | S$445.50 | S$692.00 |

| 3 years loan | 3.45% | 0% | 6.50% | S$306.53 | S$1,035.00 |

| 4 years loan | 3.46% | 0% | 6.50% | S$237.17 | S$1,384.00 |

| 5 years loan | 3.48% | 0% | 6.50% | S$195.67 | S$1,740.00 |

Best Cash-On-Instalment: OCBC Cash-On-Instalment

- Eligibility

- S$20,000 of annual income

- Max. Loan Amount

- Maximum available credit limit

- Processing Fee

- 1%

- Approval Time

- Unknown

Promotion:

|

|---|

Due to its exclusive rate offered through ValueChampion, OCBC's Cash-On-Instalments are a great option for individuals seeking an alternative to other personal loans. The bank is currently offering an exclusive interest rate of 3.50% p.a. (EIR 6.96%-8.27%) and cashback promotion when you apply for Cash-on-Instalments online.

These loans are unique in that they allow consumers to convert their available credit limit into a fixed monthly installment loan. This feature can be quite useful for those who need a relatively small sum of cash. Their 1-year loan is also relatively cheap, with a one-time processing fee of 1% of the principle amount. However, OCBC's Cash-On Instalments can be quite expensive for loans of longer durations.

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year loan | 3.50% | 1% | 8.27% | S$862.50 | S$350.00 |

| 2 year loan | 3.50% | 1% | 7.57% | S$445.83 | S$700.00 |

| 3 year loan | 3.50% | 1% | 7.27% | S$306.94 | S$1,050.00 |

| 4 year loan | 3.50% | 1% | 7.09% | S$237.50 | S$1,400.00 |

| 5 year loan | 3.50% | 1% | 6.96% | S$195.83.84 | S$1,750.00 |

- Eligibility

- S$20,000 of annual income

- Max. Loan Amount

- Maximum available credit limit

- Processing Fee

- 1%

- Approval Time

- Unknown

Promotions:

|

|---|

Due to its exclusive rate offered through ValueChampion, OCBC's Cash-On-Instalments are a great option for individuals seeking an alternative to other personal loans. The bank is currently offering an exclusive interest rate of 3.50% p.a. (EIR 6.96-8.27%) and cashback promotion when you apply for Cash-on-Instalments online..

These loans are unique in that they allow consumers to convert their available credit limit into a fixed monthly instalment loan. This feature can be quite useful for those who need a relatively small sum of cash. Their 1-year loan is also relatively cheap, with a one-time processing fee of 1% of the principal amount. However, OCBC's Cash-On Instalments can be quite expensive for longer durations.

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year loan | 3.50% | 1% | 8.27% | S$862.50 | S$350.00 |

| 2 year loan | 3.50% | 1% | 7.57% | S$445.83 | S$700.00 |

| 3 year loan | 3.50% | 1% | 7.27% | S$306.94 | S$1,050.00 |

| 4 year loan | 3.50% | 1% | 7.09% | S$237.50 | S$1,400.00 |

| 5 year loan | 3.50% | 1% | 6.96% | S$195.83.84 | S$1,750.00 |

Best Personal Loans for Low Income Borrowers

As a prospective borrower with a limited income, it can be difficult to find an affordable loan from a reputable lender. The four options below represent the best options for these individuals in Singapore.

Best Bank Loan for Low-Income Borrowers: Standard Chartered CashOne

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 2x monthly salary for annual income below S$30,000

- Min. Loan Amount

- S$1,000

- Processing Fee

- S$199 for 1st year (waived for online application), S$50 for subsequent years (waived for borrowers who make repayments on time)

- Approval Time

- 15 minutes

Promotion:

|

|---|

For individuals who make less than S$30,000 per year, Standard Chartered CashOne is the best personal loan available. For people who make between S$20,000 and S$30,000 per year, Standard Chartered offers loans with flat rates of 9.8%-10.8% and an administrative fee only for the first year. This translates to an effective interest rate (EIR) of 20%-27%, depending on the loan tenor. In comparison, other personal loans offered to lower income borrowers charge flat rates of 11%-13% in addition to processing fees (up to 4%) with EIR of around 30%. As mentioned before, approval is within 15 minutes with funds disbursed once approved.

A downside of the Standard Chartered CashOne is that it has a maximum loan cap of S$5,000 or 2x your monthly salary, whichever is lower. However, if you make less than S$30,000, we strongly advise you against borrowing more than this amount in the first place.

| Loan Duration | Flat Rate | Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year loan | 9.8% | S$199 | 27.56% | S$275 | S$493 |

| 2 year loan | 9.8% | S$0 | 23.14% | S$150 | S$588 |

| 3 year loan | 10.8% | S$0 | 22.99% | S$110 | S$972 |

| 4 year loan | 10.8% | S$0 | 21.80% | S$90 | S$1,296 |

| 5 year loan | 10.8% | S$0 | 20.92% | S$70 | S$1,620 |

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 2x monthly salary for annual income below S$30,000

- Min. Loan Amount

- S$1,000

- Processing Fee

- S$199 for 1st year (waived for online application), S$50 for subsequent years (waived for borrowers who make repayments on time)

- Approval Time

- 15 minutes

Promotion:

|

|---|

- Best Interest Rates for Low Income Borrowers

- Loan Tenor: 1 - 5 years

- Loan Amount: S$1,000 - S$5,000 or 2x your monthly salary (whichever lower)

- Approval Time: 15 minutes

- Min. Annual Income: S$20,000 (SG Citizens & PR)

For individuals who make less than S$30,000 per year, Standard Chartered CashOne is the best personal loan available. For people who make between S$20,000 and S$30,000 per year, Standard Chartered offers loans with flat rates of 9.8%-10.8% and an administrative fee only for the first year. This translates to an effective interest rate (EIR) of 20%-27%, depending on the loan tenor. In comparison, other personal loans offered to lower income borrowers charge flat rates of 11%-13% in addition to processing fees (up to 4%) with EIR of around 30%. As mentioned before, approval is within 15 minutes with funds disbursed once approved.

A downside of the Standard Chartered CashOne is that it has a maximum loan cap of S$5,000 or 2x your monthly salary, whichever is lower. However, if you make less than S$30,000, we strongly advise you against borrowing more than this amount in the first place.

| Loan Duration | Flat Rate | Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year loan | 9.8% | S$199 | 27.56% | S$275 | S$493 |

| 2 year loan | 9.8% | S$0 | 23.14% | S$150 | S$588 |

| 3 year loan | 10.8% | S$0 | 22.99% | S$110 | S$972 |

| 4 year loan | 10.8% | S$0 | 21.80% | S$90 | S$1,296 |

| 5 year loan | 10.8% | S$0 | 20.92% | S$70 | S$1,620 |

Honourable Mention: TCC Personal Loan

Promotion:

|

|---|

TCC Credit Cooperative Limited is a non-profit lending institution whose loans can be beneficial for low-income borrowers. This is largely because their minimum monthly salary requirement is S$1,200, which is much less than other banks, who typically have minimum income requirements of S$20,000 per annum. Moreover, since the firm is not a bank, there are less restrictions regarding the loan details. For example, loan repayments can be negotiated depending on unforeseen circumstances. Thus, those with low income or those looking for a more flexible loan could benefit from TCC's services.

To apply for a loan, you must be a TCC member and membership is free. Obtaining a membership will qualify you for a variety of loans they offer, from education to marriage loans, and give you access to other perks such as academic funds and discounts on healthcare providers. While TCC may be a good option for those who want low rates and flexible conditions, it's important to mention that it might not be the best option for people who are looking for a loan larger than S$50,000.

Promotion:

|

|---|

TCC Credit Cooperative Limited is a non-profit lending institution whose loans can be beneficial for low-income borrowers. This is largely because their minimum monthly salary requirement is S$1,200, which is much less than other banks, who typically have minimum income requirements of S$20,000 per annum. Moreover, since the firm is not a bank, there are less restrictions regarding the loan details. For example, loan repayments can be negotiated depending on unforeseen circumstances. Thus, those with low income or those looking for a more flexible loan could benefit from TCC's services.

To apply for a loan, you must be a TCC member and membership is free. Obtaining a membership will qualify you for a variety of loans they offer, from education to marriage loans, and give you access to other perks such as academic funds and discounts on healthcare providers. While TCC may be a good option for those who want low rates and flexible conditions, it's important to mention that it might not be the best option for people who are looking for a loan larger than S$50,000.

Best Moneylender Loans for Near-Prime Credit Borrowers: Friday Finance

- Eligibility

- No min. salary; Must be SG citizen or PR who is either a Salaried Employee, Variable/Commission-based Employee or Self Employed

- Max. Loan Amount

- 6x monthly salary

- Processing Fee

- Starting from 2%; 50% refund if loan is paid off on time

- Approval Time

- 1 day

Promotion:

|

|---|

For Singaporeans with less than perfect credit looking for a personal loan from a credible lender, Friday Finance is a good option. Friday Finance offers low monthly interest rates (between 1%-3% per month) and they will work with you to create a custom weekly or monthly repayment plan. Loan approval is short, within 1-2 hours, with disbursement within a day. They even incentivize on-time payments by refunding 50% of the administration fees when you fully pay off the loan, either by GIRO, PayNow or bank transfers. In the event you can't pay back the loan due to an accident, Friday Finance also offers personal loan protection and insurance.

Since Friday Finance takes into consideration the current and future earning capacity of each applicant, we recommend it for people who have trouble getting a loan due to a lower credit score, particularly those who make good income now but had an incident that affected their credit scores in the past. Due to this type of credit checking, it's also a great option if you don't have a fixed income stream (i.e. you are a freelancer, or entrepreneur).

- Eligibility

- No min. salary; Must be SG citizen or PR who is either a Salaried Employee, Variable/Commission-based Employee or Self Employed

- Max. Loan Amount

- 6x monthly salary

- Processing Fee

- Starting from 2%; 50% refund if loan is paid off on time

- Approval Time

- 1 day

Promotion:

|

|---|

For Singaporeans with less than perfect credit looking for a personal loan from a credible lender, Friday Finance is a good option. Friday Finance offers low monthly interest rates (between 1%-3% per month) and they will work with you to create a custom weekly or monthly repayment plan. Loan approval is short, within 1-2 hours, with disbursement within a day. They even incentivize on-time payments by refunding 50% of the administration fees when you fully pay off the loan, either by GIRO, PayNow or bank transfers. In the event you can't pay back the loan due to an accident, Friday Finance also offers personal loan protection and insurance.

Since Friday Finance takes into consideration the current and future earning capacity of each applicant, we recommend it for people who have trouble getting a loan due to a lower credit score, particularly those who make good income now but had an incident that affected their credit scores in the past. Due to this type of credit checking, it's also a great option if you don't have a fixed income stream (i.e. you are a freelancer, or entrepreneur).

Best Personal Loan for Foreigners in Singapore

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 4x monthly salary for income S$30,000 to S$120,000; 8x monthly salary for income > S$120,000; S$200,000 Maximum Loan Size (2x monthly salary for foreigners)

- Min. Loan Amount

- S$10,000

- Processing Fee

- S$0

- Approval Time

- 1 minute approval, receive cash in one business day

Promotion:

|

|---|

According to our analysis HSBC offers the best personal loan for foreigners/expats living in Singapore. Foreigners can also take advantage of 1 minute approval with disbursement within a day. Furthermore, HSBC has the lowest interest rates (6% EIR) and income requirements for foreigners (S$40,000). Finally, HSBC offers the longest personal loan tenures (7 years), which can reduce the cost of monthly instalments.

To learn more about the best personal loans available to foreigners living in Singapore, refer to our full guide.

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 3.2% | 1% | 6% | S$860.00 | S$420 |

| 2 years | 3.2% | 1% | 6% | S$443.33 | S$740 |

| 3 years | 3.2% | 1% | 6% | S$304.44 | S$1,060 |

| 4 years | 3.2% | 1% | 6% | S$235.00 | S$1,380 |

| 5 years | 3.2% | 1% | 6% | S$193.33 | S$1,700 |

| 6 years | 3.2% | 1% | 6% | S$165.56 | S$2,020 |

| 7 years | 3.2% | 1% | 6% | S$145.71 | S$2,340 |

- Eligibility

- S$30,000 of annual income

- Max. Loan Amount

- 4x monthly salary for income S$30,000 to S$120,000; 8x monthly salary for income > S$120,000; S$200,000 Maximum Loan Size (2x monthly salary for foreigners)

- Min. Loan Amount

- S$10,000

- Processing Fee

- S$0

- Approval Time

- 1 minute approval, receive cash in one business day

Promotion:

|

|---|

According to our analysis HSBC offers the best personal loan for foreigners/expats living in Singapore. Foreigners can also take advantage of 1 minute approval with disbursement within a day. Furthermore, HSBC has the lowest interest rates (6% EIR) and income requirements for foreigners (S$40,000). Finally, HSBC offers the longest personal loan tenures (7 years), which can reduce the cost of monthly instalments.

To learn more about the best personal loans available to foreigners living in Singapore, refer to our full guide.

| Loan Duration | Flat Rate | Processing Fee | EIR | Monthly Instalment | Total Cost |

|---|---|---|---|---|---|

| 1 year | 3.2% | 1% | 6% | S$860.00 | S$420 |

| 2 years | 3.2% | 1% | 6% | S$443.33 | S$740 |

| 3 years | 3.2% | 1% | 6% | S$304.44 | S$1,060 |

| 4 years | 3.2% | 1% | 6% | S$235.00 | S$1,380 |

| 5 years | 3.2% | 1% | 6% | S$193.33 | S$1,700 |

| 6 years | 3.2% | 1% | 6% | S$165.56 | S$2,020 |

| 7 years | 3.2% | 1% | 6% | S$145.71 | S$2,340 |

How to Choose the Best Personal Loan in Singapore

Before you apply for a personal loan, you should always consider all of your options. Although personal loans are cheaper than credit card debt, they still come at a relatively high price. Interest rates and other terms can also vary greatly based on your annual income and other factors. Therefore, here is some parting advice for those who want to take out a personal loan.

- Total Cost: this is the dollar amount you end up paying in interest and fees. You can minimize it by choosing low effective interest rate and short duration.

- Monthly Payment: you need to be able to comfortably afford the monthly repayment during the loan’s tenure. Otherwise, you will end up paying significant amounts in penalty fees and interest. To figure out your monthly payment, first multiply your annual flat rate by the principal amount. Then, multiply this amount by the duration of your loan in years. Then add this amount to the principal you borrowed. Dividing this by the duration of your loan in months will result in the monthly payment (also called monthly installment or monthly repayment) that you need to make to the bank.

- Balance: you need to balance the above two numbers as much as possible. Try to minimize the total cost of your personal loan, while making sure that your finances can comfortably handle the monthly installment required to pay off the loan.

Personal Instalment Loan Comparison Table

Please refer to our summary table below for the best personal loan offerings in Singapore.

| Personal Loans | Best For... | Min. Annual Income | |

|---|---|---|---|

| HSBC Personal Loan | Best Personal Loan | S$30,000 | |

| Standard Chartered CashOne | Best Promotions | S$20,000 | |

| POSB/DBS Personal Loan | Fast Cash Disbursement | S$20,000 | |

| Citibank Quick Cash | Small, Short Term Loans | S$30,000 | |

| Citibank Quick Cash 0% Interest | Small, 1-Year Loans | S$30,000 | |

| OCBC Cash-On-Instalment | Short-Term Alternative | S$30,000 | |

| Standard Chartered CashOne | Annual Income Below S$30,000 | S$20,000 | |

| HSBC Personal Loan | Foreigners in Singapore | S$40,000 | |

| Lendela Personal Loan | Low-income Borrowers | S$19,200 | |

| Friday Finance Personal Loan | Near-prime Credit Borrowers | Less than S$20,000 | |

| TCC Personal Loan | Low-income Borrowers | S$14,400 |

| Personal Loans | Best For... | Min. Annual Income | |

|---|---|---|---|

| HSBC Personal Loan | Best Personal Loan | S$30,000 | |

| Standard Chartered CashOne | Best Promotions | S$20,000 | |

| POSB/DBS Personal Loan | Fast Cash Disbursement | S$20,000 | |

| Citibank Quick Cash | Small, Short Term Loans | S$30,000 | |

| Citibank Quick Cash 0% Interest | Small, 1-Year Loans | S$30,000 | |

| OCBC Cash-On-Instalment | Short-Term Alternative | S$20,000 | |

| Standard Chartered CashOne | Annual Income Below S$30,000 | S$20,000 | |

| HSBC Personal Loan | Foreigners in Singapore | S$40,000 | |

| Lendela Personal Loan | Low-income Borrowers | S$19,200 | |

| Friday Finance | Near-prime Credit Borrowers | Less than S$20,000 | |

| TCC Personal Loan | Low-income Borrowers | S$14,400 |

Effective Interest Rate (EIR) vs Flat Interest Rate

When evaluating a personal loan in Singapore, it’s very important to consider both its flat rate and its effective interest rate (EIR). To explain the difference, flat rate is the number you use to calculate how much interest you owe on the loan. For example, if you borrow S$10,000 at 5% flat rate over 5 years, you have to pay S$500 in interest per year for the next 5 years.

In contrast, EIR represents the true economic cost of the loan, and includes the impact of processing fees and your loan repayment schedule. The reason this is important is that you don’t get to use the full amount you borrow (principal) for the entire duration of your loan. This is because you have to pay the processing fee and your principal payment back to the bank. In other words, you are paying some money back every month that has no impact on reducing your interest payment.

Therefore, you have to carefully examine both numbers when shopping for a personal loan. The flat interest rate will determine how much you have to pay back to the bank on a monthly basis. On the other hand, EIR will tell you what the loan really costs (including fees). Don't be tricked into thinking that a personal loan is only going to cost you 4-8% by looking at its flat rate. In reality, it really costs 12%-20%, if not more, which is represented by EIR.

What You Need to Apply for A Personal Loan

In Singapore, you must be between 21 and 65 years old to qualify for a personal loan. Also, most banks will require a minimum annual income of S$30,000, though some banks lend to people with as little as S$20,000 of annual income. For foreigners, this limit increases to $40,000-S$60,000 depending on the lender.

In terms of documents, you will likely need to provide the following to the lender to be approved:

- Proof of Identity: Singapore Identification Card (IC) or Employment Pass (EP) + Passport

- Proof of Address: Documents including your residential address (i.e. utility bills with your name and address)

- Proof of Income: Your Latest 12 months’ Central Provident Fund (CPF) contribution history statement or Latest Income Tax Notice of Assessment or Latest Computerised Payslip or Salary Crediting into the lender’s bank account

To learn more about how personal loans work in Singapore, you can read more about personal loans basics and how much they cost in our guides.

There are a few different types of personal loans available to borrowers in Singapore. First, there are personal instalment loans. These are the most common type of personal loans. Personal instalment loans provide borrowers funds upfront, which borrowers are expected to repay on a monthly basis over the tenor of the loan. These loans are helpful for borrowers that need financing for a large, one-time expense. Another common type of personal financing is known as a credit line or personal line of credit. These loans allow borrowers to "draw" funds as needed up to a limit determined by the lender. Borrowers are only charged interest based on the amount of money and amount of time that they have borrowed, which can make this type of financing cheaper depending on your borrowing needs. These type of loans are useful for individuals that plan to borrow smaller amounts on an ongoing basis.

Borrowers that already have a significant amount of personal debt may consider balance transfer or debt consolidation loans. Balance transfer loans allow borrowers to transfer outstanding loans to a one new loan balance. Many lenders offer a grace period of 3 to 12 months, during which borrowers are not charged interest, making these loans a great option for consolidating and paying down your personal debt. Debt consolidation loans are similar in that they allow borrowers to pay down various personal debts; however, debt consolidation loans are instalment loans that provide a lump sum of cash in order to pay down various debts. Debt consolidation loans are typically useful for borrowers that require a longer-term option for consolidating their personal debt.

If you are considering applying for a personal loan, it is essential to make sure that you are applying for the cheapest loan possible. Aside from comparing rates and fees, it is important to make sure that you are considering the most applicable loan type. For instance, it is often much more inexpensive to apply for a specific-use loan if it fits your borrowing purposes. For example, home, car and education loans tend to charge much lower interest rates than those of personal loans, making these loans less expensive for borrowers that require financing for these specific purposes. Therefore, while personal loans can be great financing tools for many large or unexpected expenses, prospective borrowers should also be aware of other borrowing options.

What if You Don’t Qualify for a Personal Loan?

Banks generally offer lower minimum requirements for Singaporeans and permanent residents. That being said, foreigners will find it a bit more difficult to get a personal loan from a bank if your income falls below S$30,000 annually, many impose higher minimum income requirements.

Your first option should be to find a personal loan from a bank. In the event you are unsuccessful, there are licensed moneylenders in Singapore that offer short-term loans. Getting a loan from a moneylender should be a last resort, and be sure to choose from the published list of licensed moneylenders from the Ministry of Law.

Take your time carefully reading through the terms and conditions. Singaporean law requires moneylenders to properly explain terms and conditions to you, so if you have any questions laid out in the terms, don't be afraid to ask. Additionally, rates vary widely across different moneylenders and can be quite high. So, you should shop around and compare rates while only borrowing what you need with the shortest loan tenure possible.

Frequently Asked Questions

Want to learn more about personal loans? Here are some answers to commonly asked questions.

Personal loans do not count towards income, so they are not taxed. Therefore, you will not need to report the amount you borrow on your income tax return. This is due from the fact that personal loans are meant to be paid back fully, so it cannot be considered part of your annual income.

Yes. Foreigners can apply for personal loans in Singapore. All you need to do to apply is to submit a copy of proof of identification, an employment pass which will be valid (at least) for the next 12 months, and three months worth of bank statements. Currently, the lowest annual income requirement for foreigners to obtain a personal loan is S$40,000 from HSBC.

Yes. You can take out a home loan even if you already have a personal loan. As long as you meet the requirements and can prove that you can repay the original loan, you will be able to acquire both loans.

If you decide to get a home loan in addition to another loan, you may wish to calculate your monthly debt obligations, or your TDSR (total debt servicing ratio for property loans). This is useful to know when budgeting for multiple monthly expenses. The following is the formula:

TDSR= (Borrower's total monthly debt obligation/Borrower's gross monthly income)*100%

Having poor credit does not mean that you cannot get a personal loan. While in most cases you'll have to meet a minimum credit score requirement to get a loan at a bank, there may be some banks that have more lenient requirements It is worth comparing some bank's eligibility requirements, but be wary that they might charge higher interest rates. Alternatively, you might be able to get a cash advance on your next paycheck or look to obtain a a licensed moneylender.

There is no limit on how many loans you can get. However, the total amount of loans you have cannot exceed 12 times your monthly income. If you decide to apply for a secondary personal loan, you will have to undergo a credit check. This will tell your prospective borrower if you have any loans currently outstanding, which could hinder your ability to get another loan.

Moreover, policies vary from lender to lender regarding eligibility for subsequent loans. For example, some providers will require you to pay on time for six consecutive months prior to giving you another loan.

Depending on which loan you choose, you will be able to take out 4-8 times your monthly income per personal loan. For example, if you have a high monthly income, HSBC will allow you to borrow 8x your monthly income.

If you want to get a loan for a specific purpose, such as buying a home or car, it is recommended that you get a loan directed for that purpose.

Yes. While you do not need to disclose the purpose of your personal loan and can therefore use a personal loan for this purpose, the higher interest rates and short tenors might deter you. Instead, it might be better for you to choose a home loan to put a down payment on your house. This is due to the lower fees and longer-term loan duration.

While it is possible to use a personal loan for nearly all purchases, if you are interested in financing in order to purchase a vehicle, renovate your home, attend university or even buy a home, you are better off considering a specific-use loan. Most banks offer a range of these loans (e.g. car loans) with interest rates that are much lower than those of personal loans.

It depends. If you are able to repay your credit card balance within your monthly billing cycle, a credit card can be a great option, as they often offer great rewards that can offset the total cost of your wedding. On the other hand, if you are unable to repay your balance in-full, you're better off choosing a personal loan, as personal loans tend to charge much lower interest rates than credit cards.

Methodology

To arrive at our best personal loan list for Singapore, we collected data from the terms and conditions of personal loans from over 10 major loan providers in Singapore, listed in our table below.

| Personal Lenders in ValueChampion's Study | |||

|---|---|---|---|

| POSB/DBS | OCBC | UOB | HSBC |

| Citibank | Standard Chartered | Maybank | CIMB |

| Hong Leong | ANZ | RHB | QianNow |

| TCC | |||

We then created an algorithm to calculate the cost of each loan. This cost includes everything that a borrower ends up paying the bank outside of the loan amount itself, which includes processing fees, administrative fees, interest rates. We also take into account benefits of promotions like fee waivers or cashback, which decrease the total cost of a loan. We assume that each monthly installment is paid on time, therefore avoiding other penalties like late payments or early payments.

Because loans come with different costs depending on their size, duration and required minimum income, cost is calculated for each duration range (1-5 years) and for each principal amount. By mapping out each loan's total costs at different size, maturity and income level, we were able to arrive at the above list that costs the least to the borrower.

Consumers who wants to find out more about other personal loans before making a decision can read our other guides to find the best personal loan in Singapore in 2022 that fits your needs.

Read Also:

Stephen Lee is a Senior Research Analyst at ValueChampion, specializing in insurance. He holds a Bachelor of Arts degree in International Studies from the University of Washington, and his prior work experience include risk management and underwriting for professional liability and specialty insurance at Victor Insurance. Additionally, Stephen is a former US Peace Corps Volunteer in Myanmar (serving between 2018-2020), where he continues to provide business development consulting services to HR companies in Asia Pacific.