Personal Installment Loans vs Personal Line of Credit: How Should You Choose?

In Singapore, there are 4 main types of personal loans: personal instalment loans, personal line of credit, balance transfers and debt consolidation plans. Among these, personal installment loans and personal lines of credit work in quite similar ways: they can both be used for almost any purpose, while the other two can only be used to pay off an existing debt. However, personal instalment loans and personal lines of credit have important distinctions that make them useful for different kinds of people and usages. Read our guide to learn the most appropriate usage of an installment loan or a line of credit so that you can use them properly.

Table of Contents

- How Personal Instalment Loans and Personal Lines of Credit Work

- Personal Instalment Loan vs Personal Line of Credit

How Personal Instalment Loans and Personal Lines of Credit Work

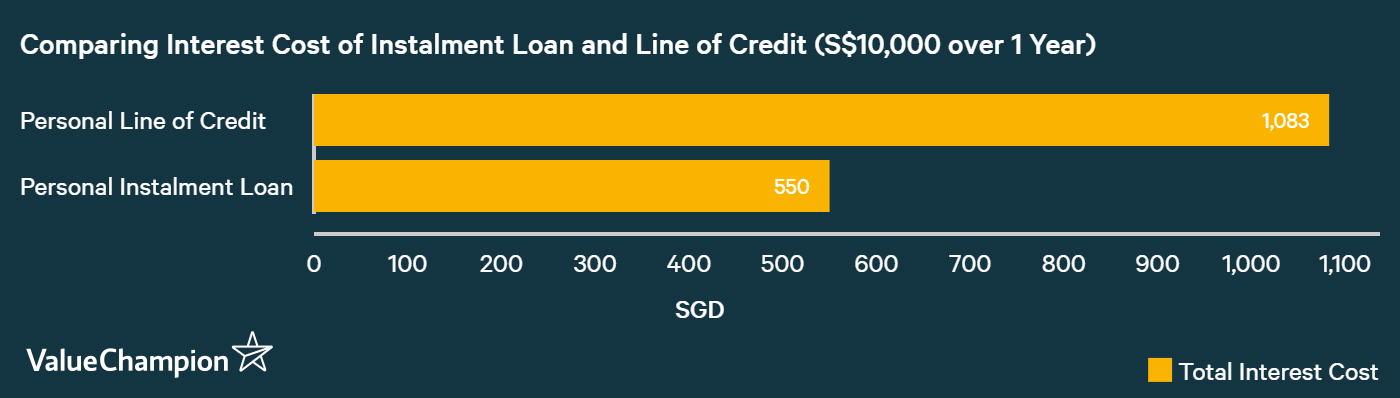

A personal instalment loan is a lump sum that you can borrow for a year or longer at a fixed interest rate. During the tenure of the loan, you have to pay a fixed amount that consists of principal and interest, the dollar value of which remain stable. For instance, let's say you take out an instalment loan of S$10,000 over 1 year at a flat rate of 5.5%. Given that it's a flat rate, the total amount of interest that you end up paying is S$550 (5.5% x S$10,000).

| Month | Remaining Principal | Monthly Payment | Principal Payment | Interest Payment |

|---|---|---|---|---|

| 0 | 10,000 | - | - | - |

| 1 | 9,167 | 879 | 833 | 45.83 |

| 2 | 8,333 | 879 | 833 | 45.83 |

| 3 | 7,500 | 879 | 833 | 45.83 |

| 4 | 6,667 | 879 | 833 | 45.83 |

| 5 | 5,833 | 879 | 833 | 45.83 |

| 6 | 5,000 | 879 | 833 | 45.83 |

| 7 | 4,167 | 879 | 833 | 45.83 |

| 8 | 3,333 | 879 | 833 | 45.83 |

| 9 | 2,500 | 879 | 833 | 45.83 |

| 10 | 1,667 | 879 | 833 | 45.83 |

| 11 | 833 | 879 | 833 | 45.83 |

| 12 | - | 879 | 833 | 45.83 |

| Total | 10,550 | 10,000 | 550 |

In contrast, a personal line of credit is the total amount of dollars that you can borrow from your bank at any time. You typically pay an annual fee for having access to this fund, and pay interest only on the amount that you have drawn from your line of credit at any given point in time. For example, let's assume that you have S$10,000 worth of personal line of credit open. If end up not borrowing a dollar from this account, you won't owe a single dollar of interest to your bank. If you take out S$5,000 from your line of credit for 1 month, you would be charged around S$83 in interest (S$5,000 x 20% / 12 months)

Personal Instalment Loan vs Personal Line of Credit

If you are trying to decide between getting a personal instalment loan and getting a personal line of credit, the rule of thumb you should adhere to is the following: use instalment loan for sudden and/or unavoidable expenditures that are large (and hence need to be repaid over a long period of time), and use line of credit to supplement your unpredictable and/or inconsistent source of income for amount of money that can be paid back relatively quickly.

| Type of Personal Loan | Best For... |

|---|---|

| Personal Instalment Loan | Large expenditures that are sudden and unavoidable |

| Personal Line of Credit | People with unpredictable or inconsistent source of income |

| Balance Transfers | Repaying a small amount of credit card or personal loan over a few months |

| Debt Consolidation Plans | Repaying a small amount of credit card or personal loan over a few years |

Instalment loans are great for funding large expenditures that need to be paid over time because its repayment schedule is spread out over a few years at a relatively low interest rate, as we've shown above. On the other hand, if you try to use a line of credit in the same manner, it can cost you dearly. For example, let's assume you take a line of credit of S$10,000, and repay it as if it were an instalment loan over a 12-month period. Because personal lines of credit typically charge an interest rate of 20%, you could end up paying S$1,083 in interest, nearly 2x what an instalment loan would've cost you.

| Month | Remaining Principal | Monthly Payment | Principal Payment | Interest Payment |

|---|---|---|---|---|

| 0 | 10,000 | - | - | - |

| 1 | 9,167 | 1,000 | 833 | 167 |

| 2 | 8,333 | 986 | 833 | 153 |

| 3 | 7,500 | 972 | 833 | 139 |

| 4 | 6,667 | 958 | 833 | 125 |

| 5 | 5,833 | 944 | 833 | 111 |

| 6 | 5,000 | 931 | 833 | 97 |

| 7 | 4,167 | 917 | 833 | 83 |

| 8 | 3,333 | 903 | 833 | 69 |

| 9 | 2,500 | 889 | 833 | 56 |

| 10 | 1,667 | 875 | 833 | 42 |

| 11 | 833 | 861 | 833 | 28 |

| 12 | - | 847 | 833 | 14 |

| Total | 11,083 | 10,000 | 1,083 |

Similarly, if you only needed to borrow S$1,000 for 1 month every other month, you would be much better off getting a line of credit. Each time you borrow S$1,000 for 1 month, you would owe an interest of S$16.67 only, which would add up to S$100 if you do it 6 times within 1 year. On the other hand, getting a S$6,000 personal loan for 1 year would unnecessarily cost you S$330 (S$6,000 x 5.5%) in interest. Instalment loans are simply not flexible enough for usages that are sporadic and temporary.

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.