Balance Transfer vs Debt Consolidation Plan: Which Is Better?

With the rapid rise in personal debt in the recent years, there has been a massive growth in demand for financial facilities that help people payoff their loans. In Singapore, there are 2 main types of personal loans that do just this: balance transfers and debt consolidation plans. While these two loan facilities have similar functions, they have important distinctions that make them useful for different kinds of people and usages. Read our guide to see which is more appropriate for your needs.

Table of Contents

How Balance Transfers and Debt Consolidation Plans Work

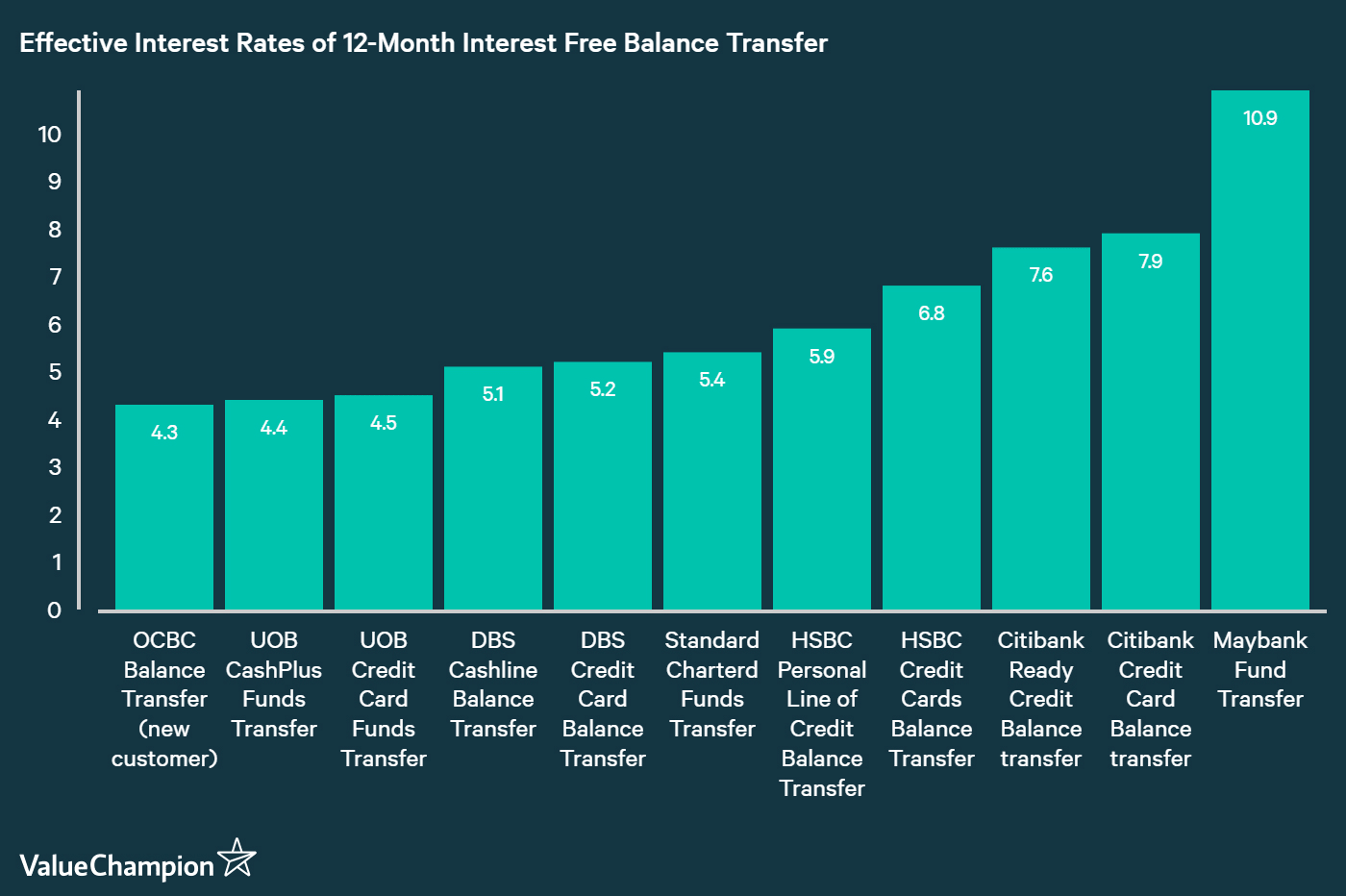

A balance transfer is a facility that provides you with a predetermined length of "interest free period," which you can use to pay down your various personal loans (i.e. personal instalment loans or credit card debt) quickly without incurring high interests. Typically, you pay a one-time processing fee ranging from 1.5% to 5.5%, and get either 3, 6 or 12 months to pay down your debt without incurring any interests. If you still have balance remaining after your interest free "grace period," however, you will again incur interest on the remaining portion that could range from 26 to 30%. Assuming you pay off your balance in full within your grace period, the processing fee can translate into an effective interest rate as displayed in our chart below.

In contrast, a debt consolidation plan is an instalment loan that is specifically used for paying off your personal debt. Hence, you get a lump sum at the beginning, which you have to repay in equal amount of monthly repayments over 1 year to 10 years, depending on the tenure of your loan. For example, let's say you take out a debt consolidation loan to pay off S$10,000 of credit card bills and personal loans, and the tenure of the loan is 1 year. Given its flat interest rate of 4.7%, the total amount of interest that you end up paying is S$470 (4.7% x S$10,000).

| Month | Remaining Principal | Monthly Payment | Principal Payment | Interest Payment |

|---|---|---|---|---|

| 0 | 10,000 | - | - | - |

| 1 | 9,167 | 872 | 833 | 39.17 |

| 2 | 8,333 | 872 | 833 | 39.17 |

| 3 | 7,500 | 872 | 833 | 39.17 |

| 4 | 6,667 | 872 | 833 | 39.17 |

| 5 | 5,833 | 872 | 833 | 39.17 |

| 6 | 5,000 | 872 | 833 | 39.17 |

| 7 | 4,167 | 872 | 833 | 39.17 |

| 8 | 3,333 | 872 | 833 | 39.17 |

| 9 | 2,500 | 872 | 833 | 39.17 |

| 10 | 1,667 | 872 | 833 | 39.17 |

| 11 | 833 | 872 | 833 | 39.17 |

| 12 | - | 872 | 833 | 39.17 |

| Total | 10,550 | 10,000 | 470 |

Balance Transfer vs Debt Consolidation Plan

If you are trying to decide between getting a balance transfer loan and getting a debt consolidation plan, almost the only thing that you should consider is how much time you need to repay your loan. If you make enough money to repay your balance within 12 months, you should go for a balance transfer. If you need more than 1 year to payoff your loan in full, you should go for a debt consolidation plan.

| Type of Personal Loan | Best For... |

|---|---|

| Personal Instalment Loan | Large expenditures that are sudden and unavoidable |

| Personal Line of Credit | People with unpredictable or inconsistent source of income |

| Balance Transfers | Repaying a small amount of credit card or personal loan over a few months |

| Debt Consolidation Plans | Repaying a small amount of credit card or personal loan over a few years |

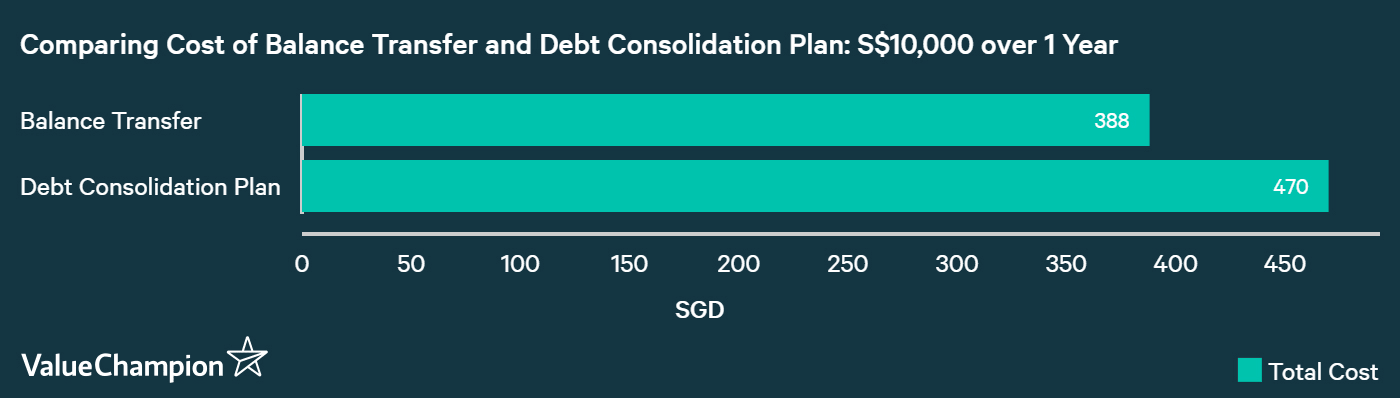

Consider an example of a balance that you need to pay off of S$10,000. You make enough money to pay off the balance over a 12 months period by using either balance transfer or a debt consolidation plan. Given that the best balance transfer loans charge a one time processing fee of 3.88% for a 12-month interest free period, you would only incur the cost of S$388 as long as you payoff your loan in full before your grace period is over. On the other hand, the best debt consolidation plans charge a flat rate of 4.7%, which translates to roughly S$470 of cost in interest over 1 year.

However, you can pay debt consolidation plan allows you to spread out your loan repayment for longer than 1 year (2-10 years) while paying a low level of interest, lightening the burden of debt repayment on your daily lifestyle. In contrast, balance transfers charge you an astronomical rate of 26% or higher after your grace period is over. Therefore, if you can only pay off 50% of your balance in 12 months (and pay off fully in your 2nd year), you would incur almost S$1,100 of interest and fees for 2 years, compared to S$940 of interest you would've paid on your debt consolidation loan.

| Month | Remaining Principal | Monthly Payment | Principal Payment | Interest Payment |

|---|---|---|---|---|

| 0 | 10,000 | 388 | - | 388 |

| 1-12 | 9,583 | 417 | 417 | - |

| 13 | 4,583 | 525 | 417 | 108 |

| 14 | 4,167 | 516 | 417 | 99 |

| 15 | 3,750 | 507 | 417 | 90 |

| 16 | 3,333 | 498 | 417 | 81 |

| 17 | 2,917 | 489 | 417 | 72 |

| 18 | 2,500 | 480 | 417 | 63 |

| 19 | 2,083 | 471 | 417 | 54 |

| 20 | 1,667 | 462 | 417 | 45 |

| 21 | 1,250 | 453 | 417 | 36 |

| 22 | 833 | 444 | 417 | 27 |

| 23 | 417 | 435 | 417 | 18 |

| 24 | - | 426 | 417 | 9 |

| Total | 11,092 | 10,000 | 1,092 |

Duckju (DJ) is the founder and CEO of ValueChampion. He covers the financial services industry, consumer finance products, budgeting and investing. He previously worked at hedge funds such as Tiger Asia and Cadian Capital. He graduated from Yale University with a Bachelor of Arts degree in Economics with honors, Magna Cum Laude. His work has been featured on major international media such as CNBC, Bloomberg, CNN, the Straits Times, Today and more.