Best No Annual Fee Credit Cards in Singapore 2024

Credit cards with no annual fee, or an easy annual fee waiver, provide a low-maintenance option that allows consumers to enjoy rewards without worrying if the rewards offset the annual fee. Not all no-fee cards are created equal, however. Our credit card experts have reviewed every no annual fee credit card in Singapore to identify those with the most competitive rates, ensuring you will maximise rewards as well as save money.

- DBS Altitude: Earn 5 miles per S$1 spend on online flight & hotel transactions (capped at S$5,000 per month) and overseas spend (at point-of-sale), earn S$1 = 2 miles on overseas spend (online transactions), earn S$1 = 1.2 miles on local spend. All miles earned through this card is via DBS Points and thus will never expire.

- Maybank Horizon Visa: Market-leading 3.2 miles per S$1 select local spend

- UOB PRVI Miles Amex: Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- OCBC Frank: Up to 6% rebate for FX, online and mobile purchases, low S$600 min. spend requirement

- Maybank Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- CIMB Visa Infinite: Unlimited 2% cashback on travel, overseas and online spend in foreign currencies

- DBS Woman's World: Get up to 10X DBS Points (or 20 miles) for online purchases, 3X DBS Point (or 6 miles) for overseas purchases and 1X DBS Point (or 2 miles) for other purchases

- OCBC Titanium: 4 miles per S$1 on fashion & select retail

- HSBC Revolution: 4 miles per S$1 spent online and on contactless payments

- Maybank World: Free green fees at 100 fairways across 19 countries

- CIMB World MC: Unlimited 2% cashback on wine and dine, food delivery, entertainment, taxi & automobile, luxury goods and 50% off green fees

- HSBC Visa Platinum: 5% rebate on groceries, dining & petrol, miles for general

- CIMB Platinum MC: 10% rebate on wine and dine, transport, petrol, health and travel, capped at S$100/month

- CIMB Visa Signature: 10% cashback on online shopping, groceries, beauty and wellness, pet shops and cruises

When choosing your perfect credit card, it's important to consider several factors like how well its rewards fit your spending lifestyle and whether you can meet its minimum spend requirements. One of the most significant factors is the annual fee, because they can sometimes outweigh your annual earnings in terms of rewards. The no-fee credit cards reviewed below either never charge an annual fee or offer achievable waivers (such as waiving a fee for S$10k annual spend). These cards therefore require far less maintenance, and will allow you to earn easily on your daily spend.

When choosing your perfect credit card, it's important to consider several factors like how well its rewards fit your spending lifestyle and whether you can meet its minimum spend requirements. One of the most significant factors is the annual fee, because they can sometimes outweigh your annual earnings in terms of rewards. The no-fee credit cards reviewed below either never charge an annual fee or offer achievable waivers (such as waiving a fee for S$10k annual spend). These cards therefore require far less maintenance, and will allow you to earn easily on your daily spend.

- DBS Altitude: Earn 5 miles per S$1 spend on online flight & hotel transactions (capped at S$5,000 per month) and overseas spend (at point-of-sale), earn S$1 = 2 miles on overseas spend (online transactions), earn S$1 = 1.2 miles on local spend. All miles earned through this card is via DBS Points and thus will never expire.

- Maybank Horizon Visa: Market-leading 3.2 miles per S$1 select local spend

- UOB PRVI Miles Amex: Fee-Waiver + 20k bonus miles, 2.4 miles per $1 overseas

- OCBC 365: 6% rebate on dining, 3% rebate on groceries, utilities and travel, Visa Concierge Services

- OCBC Frank: Up to 6% rebate for FX, online and mobile purchases, low S$600 min. spend requirement

- Maybank Platinum Visa: Up to 3.33% rebate on local and foreign currency spend

- CIMB Visa Infinite: Unlimited 2% cashback on travel, overseas and online spend in foreign currencies

- DBS Woman's World: Get up to 10X DBS Points (or 20 miles) for online purchases, 3X DBS Point (or 6 miles) for overseas purchases and 1X DBS Point (or 2 miles) for other purchases

- OCBC Titanium: 4 miles per S$1 on fashion & select retail

- HSBC Revolution: 4 miles per S$1 spent online and on contactless payments

- Maybank World: Free green fees at 100 fairways across 19 countries

- CIMB World MC: Unlimited 2% cashback on wine and dine, food delivery, entertainment, taxi & automobile, luxury goods and 50% off green fees

- HSBC Visa Platinum: 5% rebate on groceries, dining & petrol, miles for general

- CIMB Platinum MC: 10% rebate on wine and dine, transport, petrol, health and travel, capped at S$100/month

- CIMB Visa Signature: 10% cashback on online shopping, groceries, beauty and wellness, pet shops and cruises

Best No Fee Credit Cards for Air Miles

While many travel credit cards are expensive, the following credit cards in Singapore offer great rewards rates for air miles yet have no annual fee.

DBS Altitude Visa: Best Miles Credit Card with Affordable Perks

| |

DBS Altitude Visa Card stands out by offering more travel perks than any other miles credit card with a fee-waiver. Cardholders earn respectable rewards rates at 1.2 miles per S$1 local spend, 2 miles overseas, 3 miles on online travel bookings, and miles earned never expire. However, unlike other comparable cards, DBS Altitude Card offers free travel insurance, 2 lounge visits/year, golfing privileges throughout SE Asia, dining privileges with Visa Foodie Trail & more. In fact, these perks are more extensive than some travel credit cards with S$250+ fees.

| |

|

|

DBS Altitude Visa Card stands out by offering more travel perks than any other miles credit card with a fee-waiver. Cardholders earn respectable rewards rates at 1.2 miles per S$1 local spend, 2 miles overseas, 3 miles on online travel bookings, and miles earned never expire. However, unlike other comparable cards, DBS Altitude Card offers free travel insurance, 2 lounge visits/year, golfing privileges throughout SE Asia, dining privileges with Visa Foodie Trail & more. In fact, these perks are more extensive than some travel credit cards with S$250+ fees.

|

Maybank Horizon Visa Signature: Best Miles Card for Local Budgets

| |

Maybank Horizon Visa Signature Card is an excellent way for primarily local spenders to earn miles at home at top rates, but then also earn on vacation bookings and spend abroad. Cardholders earn 3.2 miles per S$1 spend on local dining, petrol, taxis & Grab, and hotel bookings with Agoda–this rate is higher than that offered by even the priciest travel credit cards. In addition, cardholders earn 2 miles per S$1 spend on air tickets, travel packages and foreign currency transactions, which aligns with the overseas rates of other travel cards. While earnings are limited by category, local food & transportation account for nearly have of the average budget, so most consumers can easily earn with this credit card.

| |

|

|

Maybank Horizon Visa Signature Card is an excellent way for primarily local spenders to earn miles at home at top rates, but then also earn on vacation bookings and spend abroad. Cardholders earn 3.2 miles per S$1 spend on local dining, petrol, taxis & Grab, and hotel bookings with Agoda–this rate is higher than that offered by even the priciest travel credit cards. In addition, cardholders earn 2 miles per S$1 spend on air tickets, travel packages and foreign currency transactions, which aligns with the overseas rates of other travel credit cards. While earnings are limited by category, local food & transportation account for nearly have of the average budget, so most consumers can easily earn with this credit card.

|

UOB PRVI Miles American Express Card: Best for Rapid Miles

| |

UOB PRVI Miles American Express Card is the only luxury travel credit card with a fee waiver, allowing above-average spenders to take advantage of high rates, great perks, and even bonus miles without added cost. Cardholders earn 1.4 miles per S$1 locally, 2.4 miles overseas, and 6 miles with major airlines & hotels–rates equal to (or higher than) most pricey travel credit cards’. In addition, cardholders receive free travel insurance, free airport transfers and more.

| |

|

|

UOB PRVI Miles American Express Card is the only luxury travel credit card with a fee waiver, allowing above-average spenders to take advantage of high rates, great perks, and even bonus miles without added cost. Cardholders earn 1.4 miles per S$1 locally, 2.4 miles overseas, and 6 miles with major airlines & hotels–rates equal to (or higher than) most pricey travel credit cards’. In addition, cardholders receive free travel insurance, free airport transfers and more.

|

Best No Fee Credit Cards for Cashback

If you want to earn rebates on daily essentials without worrying about paying extra for your credit card, consider these credit cards with no annual fee in Singapore.

OCBC 365 Card: Best No Fee Cashback Overall

| |

If you want a no-fee everyday credit card that rewards your essential spend, OCBC 365 Card is absolutely the best option on the market. Not only is there a fee waiver with just S$10,000 annual spend, there also aren’t any merchant restrictions–two benefits you won’t find with OCBC 365 Card’s key competitor. Cardholders earn 6% on dining & online food delivery and 3% on groceries, land transport (including Grab), online travel bookings, and even recurring electricity & telco bills–compared to the competitor’s 1% rebate on bills, capped at S$1/month.

| |

|

|

If you want a no-fee everyday credit card that rewards your essential spend, OCBC 365 Card is absolutely the best option on the market. Not only is there a fee waiver with just S$10,000 annual spend, there also aren’t any merchant restrictions–two benefits you won’t find with OCBC 365 Card’s key competitor. Cardholders earn 6% on dining & online food delivery and 3% on groceries, land transport (including Grab), online travel bookings, and even recurring electricity & telco bills–compared to the competitor’s 1% rebate on bills, capped at S$1/month.

|

Best No Fee Credit Cards for Lower Spenders

Suitable for those with a smaller budget, these cards offer low minimum spend requirements, respectable rates, and easy annual fee-waivers.

OCBC Frank Card: Best for Young Online Shoppers

|

|

Young adults with lower monthly spend are most likely to maximise their cashback with OCBC Frank Card. Unlike its competitor credit cards (some of which have an S$800+ minimum requirement), OCBC Frank allows cardholders to access its higher rates after just S$600 spend. Consumers earn 6% rebate on FX, online, and mobile contactless spend. Additionally, this card offers 0.3% on all other purchases. Earnings are a respectable S$75/month (S$25/FX & mobile contactless, S$25/online, and S$25/general).

OCBC Frank Card also stands apart from its closest competitor by offering a fee-waiver. With just S$10,000 annual spend, cardholders are exempt from the S$80 fee, which itself is fairly low. If you’re looking for a card that rewards online shopping and mobile contactless purchases without a lofty spend requirement, OCBC Frank Card is the best and most affordable option. | |

|

|

|---|

|

|

Young adults with lower monthly spend are most likely to maximise their cashback with OCBC Frank Card. Unlike its competitor credit cards (some of which have an S$800+ minimum requirement), OCBC Frank allows cardholders to access its higher rates after just S$600 spend. Consumers earn 6% rebate on FX, online, and mobile contactless spend. Additionally, this card offers 0.3% on all other purchases. Earnings are a respectable S$75/month (S$25/FX & mobile contactless, S$25/online, and S$25/general).

OCBC Frank Card also stands apart from its closest competitor by offering a fee-waiver. With just S$10,000 annual spend, cardholders are exempt from the S$80 fee, which itself is fairly low. If you’re looking for a card that rewards online shopping and mobile contactless purchases without a lofty spend requirement, OCBC Frank Card is the best and most affordable option. |

Maybank Platinum Visa: Best for Small Budgets

| |

If you’re looking for cashback after just S$300 local spend–maybe for a lower budget, or as a complement to a travel card–Maybank Platinum Visa Card is the only rebate credit card that can truly maximise your earnings while also waiving its fee. Almost all cashback credit cards require minimums of S$400+ (at the very least) to earn rewards beyond the base rate (usually 0.3%). With Maybank Platinum Visa Card, you can earn S$30/quarter after just S$300 local monthly spend, equal to S$1,200/year. Compare this to S$3.6/year, earned for the same spend but at the base rate.

| |

|

|

If you’re looking for cashback after just S$300 local spend–maybe for a lower budget, or as a complement to a travel card–Maybank Platinum Visa Card is the only rebate credit card that can truly maximise your earnings while also waiving its fee. Almost all cashback credit cards require minimums of S$400+ (at the very least) to earn rewards beyond the base rate (usually 0.3%). With Maybank Platinum Visa Card, you can earn S$30/quarter after just S$300 local monthly spend, equal to S$1,200/year. Compare this to S$3.6/year, earned for the same spend but at the base rate.

|

Best No Fee Credit Cards for High Spenders

High spenders shouldn’t have to pay high annual fees. The following credit cards in Singapore with no annual fee, offer unlimited and maintenance-free earning potential, without the hassle of added cost.

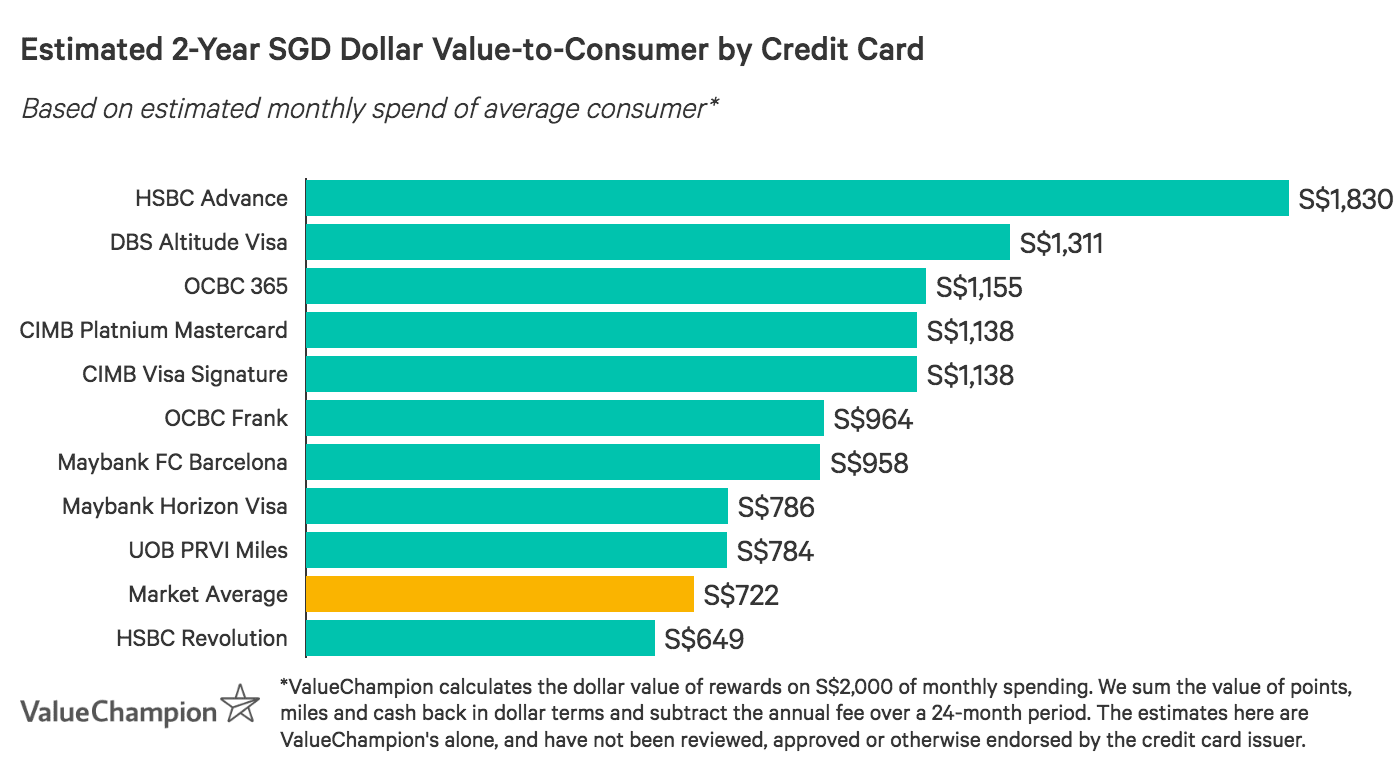

CIMB Visa Infinite Card: Unlimited Cashback for Travellers

| |

If you’re an affluent traveller interested in earning cashback (rather than miles), CIMB Visa Infinite Card is an excellent, no-fee way to earn on all spend. Cardholders earn 1% unlimited cashback on all spend, bumped to 2% for travel expenses (hotels, airlines, travel agencies & more) after a S$2,000 minimum threshold. Competitor credit cards offer 1.5% flat cashback, so frequent travellers are far more likely to benefit from CIMB Visa Infinite Card. Most competitors also charge S$170+ fees, while CIMB Visa Infinite Card is free forever.

| |

|

|

If you’re an affluent traveller interested in earning cashback (rather than miles), CIMB Visa Infinite Card is an excellent, no-fee way to earn on all spend. Cardholders earn 1% unlimited cashback on all spend, bumped to 2% for travel expenses (hotels, airlines, travel agencies & more) after a S$2,000 minimum threshold. Competitor credit cards offer 1.5% flat cashback, so frequent travellers are far more likely to benefit from CIMB Visa Infinite Card. Most competitors also charge S$170+ fees, while CIMB Visa Infinite Card is free forever.

|

Best No Fee Credit Cards for Retail Shoppers

Whether you mostly shop for retail or pay for bills and essentials online, we have found a few credit cards that can maximise rewards without charging an annual fee.

DBS Woman's World: Shopper Card with 0% Interest Instal Plan

| |

DBS Woman’s World Card is a great option for average spenders seeking rewards for online shopping. Cardholders earn 4 miles per S$1 spend in this category, up to 8,000 miles/month (about S$80 value-to-consumer). In addition, cardholders can split payments for their larger purchases into instalments across up to 12 months, with 0% interest and no processing fee. While general spend earns just 0.4 miles per S$1 locally, 1.2 miles overseas, frequent online shoppers who spend at least S$25,000 annually are exempt from the S$192.6 fee. For these shoppers, DBS Woman’s World Card offers easy and accessible rewards without added maintenance or cost.

| |

|

|

DBS Woman’s World Card is a great option for average spenders seeking rewards for online shopping. Cardholders earn 4 miles per S$1 spend in this category, up to 8,000 miles/month (about S$80 value-to-consumer). In addition, cardholders can split payments for their larger purchases into instalments across up to 12 months, with 0% interest and no processing fee. While general spend earns just 0.4 miles per S$1 locally, 1.2 miles overseas, frequent online shoppers who spend at least S$25,000 annually are exempt from the S$192.6 fee. For these shoppers, DBS Woman’s World Card offers easy and accessible rewards without added maintenance or cost.

|

OCBC Titanium Card: Miles for Retail Shoppers

| |

If you’re a frequent retail shopper, look no further than OCBC Titanium Rewards Card–the most flexible and comprehensive shopper card on the market, with the added benefits of high rates and an easily waived fee. Cardholders earn 10 points (4 miles) per S$1 spend on retail, department stores, and electronics–plus on a variety of retail merchants, from Amazon to Qoo10 & more. Consumers can earn rewards locally, overseas, online and offline, with no minimum spend requirement. This flexibility makes it easy for average spenders to quickly achieve the 4,000 miles/month earnings cap.

| |

|

|

If you’re a frequent retail shopper, look no further than OCBC Titanium Rewards Card–the most flexible and comprehensive shopper card on the market, with the added benefits of high rates and an easily waived fee. Cardholders earn 10 points (4 miles) per S$1 spend on retail, department stores, and electronics–plus on a variety of retail merchants, from Amazon to Qoo10 & more. Consumers can earn rewards locally, overseas, online and offline, with no minimum spend requirement. This flexibility makes it easy for average spenders to quickly achieve the 4,000 miles/month earnings cap.

|

HSBC Revolution: Miles for Online & Social Spenders

| |

HSBC Revolution Card is one of the best miles-earning cards for social spenders who tend to make many purchases online. Cardholders earn 2 miles per S$1 spend on local dining & entertainment, and have access to a myriad of regional deals and discounts. More uniquely, cardholders also earn this rewards rate for online spend, including on travel bookings, transit payments, and recurring bills. These expenses are almost always excluded from earning rewards by other cards. There are no minimum spend requirements and earnings are unlimited, making HSBC Revolution Card a great match for many budgets. And, if that wasn’t enough, the S$160.5 fee is waived with S$12,500 annual spend. HSBC Revolution Card is both extremely accessible and a great way for social and online spenders to maximise rewards from their monthly budget.

| |

|

|

HSBC Revolution Card is one of the best miles-earning cards for social spenders who tend to make many purchases online. Cardholders earn 2 miles per S$1 spend on local dining & entertainment, and have access to a myriad of regional deals and discounts. More uniquely, cardholders also earn this rewards rate for online spend, including on travel bookings, transit payments, and recurring bills. These expenses are almost always excluded from earning rewards by other cards. There are no minimum spend requirements and earnings are unlimited, making HSBC Revolution Card a great match for many budgets. And, if that wasn’t enough, the S$160.5 fee is waived with S$12,500 annual spend. HSBC Revolution Card is both extremely accessible and a great way for social and online spenders to maximise rewards from their monthly budget.

|

Best No Fee Credit Cards for Golf & Leisure

The following no annual fee credit cards offer great entertainment and leisure perks in Singapore.The following credit cards offer great leisure perks, despite waiving an annual fee.

Maybank World MasterCard: Best Miles Card for Golfers

| |

With Maybank World MasterCard, golfers can enjoy the most comprehensive golfing privileges on the market and possibly avoid paying an annual fee. Cardholders receive complimentary green fees all year round at 100 participating golf clubs in 23 countries – nearly triple the amount offered by the top competitor credit card. Consumers can also earn 10 points (4 miles) per S$1 spend on select dining & retail merchants, such as Paradise Group, Imperial Treasure, Resorts World Sentosa, The Shilla Duty Free Changi Airport and many more. Additional perks include free travel insurance and Plaza Premium airport lounge access. Ultimately, cardholders can even avoid the S$240 fee by spending S$24,000/year. While this may seem substantial, spend on supplementary cards adds towards total spend, making it easier to reach this threshold. Maybank World MasterCard is an excellent option for people who prioritise golfing privileges and enjoy luxury shopping.

| |

|

|

With Maybank World MasterCard, golfers can enjoy the most comprehensive golfing privileges on the market and possibly avoid paying an annual fee. Cardholders receive 2 complimentary green fees per month at 120 fairways across 25 countries–triple the amount offered by the top competitor credit card. Consumers can also earn 10 points (4 miles) per S$1 spend on select dining & retail merchants. Additional perks include free travel insurance and lounge access. Ultimately, cardholders can even avoid the S$240 fee by spending S$24,000/year. While this may seem substantial, spend on supplementary cards adds towards total spend, making it easier to reach this threshold. Maybank World MasterCard is an excellent option for people who prioritise golfing privileges and enjoy luxury shopping.

|

CIMB World Mastercard: Cashback for Affluent Socialites

| |

CIMB World MasterCard is the absolute best credit card on the market for affluent social spenders looking to balance great privileges with unlimited cashback rewards. While competitor credit cards narrow earning potential with merchant restrictions, CIMB World MasterCard offers unlimited 2% cashback with all vendors across a variety of categories: wine & dine (including food deliveries), movies & digital entertainment, taxi & automobile and luxury goods with a minimum monthly spending of S$1,000. This 2% rate is higher than the flat 1.5% offered by other unlimited cashback credit cards, and unlike these cards, CIMB World MasterCard is free forever. In addition, all other spend earns unlimited 1% cashback. Consumers also enjoy perks like 50% off green fees, and access to MasterCard Airport Experiences. Overall, CIMB World Card is a great way to maximise rewards on leisure spend without any extra hassle or fees.

| |

|

|

CIMB World MasterCard is the absolute best credit card on the market for affluent social spenders looking to balance great privileges with unlimited cashback rewards. While competitor credit cards narrow earning potential with merchant restrictions, CIMB World MasterCard offers unlimited 2% cashback with all vendors across a variety of categories: wine & dine (including food deliveries), movies & digital entertainment, taxi & automobile and luxury goods. This 2% rate is higher than the flat 1.5% offered by other unlimited cashback credit cards, and unlike these cards, CIMB World MasterCard is free forever. In addition, all other spend earns unlimited 1% cashback. Consumers also enjoy perks like 50% off green fees, and access to MasterCard Airport Experiences. Overall, CIMB World Card is a great way to maximise rewards on leisure spend without any extra hassle or fees.

|

HSBC Visa Platinum: No Fee Card for Cashback + Miles

| |

HSBC Visa Platinum Card is the best credit card on the market for earning both cashback and miles, especially if you’re looking to avoid an annual fee. Cardholders earn 5% cashback on local dining, groceries and petrol after just S$600 minimum spend. All other spend earns 0.4 miles per S$1, with no minimum spend requirement. While this is on the lower side, it’s worth pointing out that the rebate covers the top spend categories in the average consumer’s budget. In addition, cardholders can earn up to S$83/month (S$250/quarter) which is fairly high.

| |

|

|

HSBC Visa Platinum Card is the best credit card on the market for earning both cashback and miles, especially if you’re looking to avoid an annual fee. Cardholders earn 5% cashback on local dining, groceries and petrol after just S$600 minimum spend. All other spend earns 0.4 miles per S$1, with no minimum spend requirement. While this is on the lower side, it’s worth pointing out that the rebate covers the top spend categories in the average consumer’s budget. In addition, cardholders can earn up to S$83/month (S$250/quarter) which is fairly high.

|

CIMB Platinum MasterCard: No Fee Card for Health, Transport & Dining

|

|

CIMB Platinum MasterCard is an especially unique credit card, combining exceptional rewards for medical expenses, transport, dining & more. Each of these categories–as well as travel spend in foreign currency and electronics/furnishings purchases– earns 10% cashback, up to a cumulative S$100/month. Very few credit cards reward health or home improvement spend, especially at such high rates–making CIMB Platinum MC truly stand-out. Even more, while there's an S$800 minimum spend requirement, there's no annual fee, making CIMB Platinum MC an excellent option for those seeking a low-risk, no-maintenance credit card.

| |

|

|

|---|

|

|

CIMB Platinum MasterCard is an especially unique credit card, combining exceptional rewards for medical expenses, transport, dining & more. Each of these categories–as well as travel spend in foreign currency and electronics/furnishings purchases– earns 10% cashback, up to a cumulative S$100/month. Very few credit cards reward health or home improvement spend, especially at such high rates–making CIMB Platinum MC truly stand-out. Even more, while there's an S$800 minimum spend requirement, there's no annual fee, making CIMB Platinum MC an excellent option for those seeking a low-risk, no-maintenance credit card.

|

CIMB Visa Signature: Cashback for Online & Beauty Spend

| |

CIMB Visa Signature Card is a great option for grocery-shoppers seeking cashback for discretionary spend. Groceries, online shopping, beauty, petcare, and transactions with cruise lines all earn 10% rebate, up to S$20/category. This adds up to a potential S$100/month–quite respectable given market standards–though accessing these rates requires an S$800 minimum spend. In addition, you can earn an unlimited 0.2% on all other spend. It's also worth mentioning that CIMB Visa Signature is exceptionally low-risk and low-maintenance, as there's no annual fee. This means consumers who only periodically shop these categories can still benefit from the high rebate rates.

| |

|

|

CIMB Visa Signature Card is a great option for grocery-shoppers seeking cashback for discretionary spend. Groceries, online shopping, beauty, petcare, and transactions with cruise lines all earn 10% rebate, up to S$20/category. This adds up to a potential S$100/month–quite respectable given market standards–though accessing these rates requires an S$800 minimum spend. In addition, you can earn an unlimited 0.2% on all other spend. It's also worth mentioning that CIMB Visa Signature is exceptionally low-risk and low-maintenance, as there's no annual fee. This means consumers who only periodically shop these categories can still benefit from the high rebate rates.

|

Learn More About How to Find the Best Credit Card for You

Zoryana is a Senior Research Analyst at ValueChampion, who focuses on evaluating credit cards, savings and fixed deposits in Singapore. She holds a BA in Political Science and an MPA in International Finance and Economic Policy, both from Columbia University. Prior to joining ValueChampion, Zoryana worked in treasury management consulting.